A Look At JetBlue Airways (JBLU) Valuation As New Boston Milan Route And United Partnership Expand Its Network

JetBlue Airways Corporation JBLU | 0.00 |

JetBlue Airways (JBLU) has been in focus after launching its first Boston to Milan route and rolling out reciprocal loyalty perks with United Airlines. These moves reshape its transatlantic and frequent flier footprint.

These new routes and loyalty perks come as JetBlue’s 7 day share price return of 10.26% contrasts with a weaker 90 day share price return of 15.48% and a 5 year total shareholder return that is down 74.88%, highlighting stronger short term movement alongside a more challenging longer term record.

If this kind of corporate reshaping has your attention, it can be a good moment to broaden your radar and check out 20 top founder-led companies

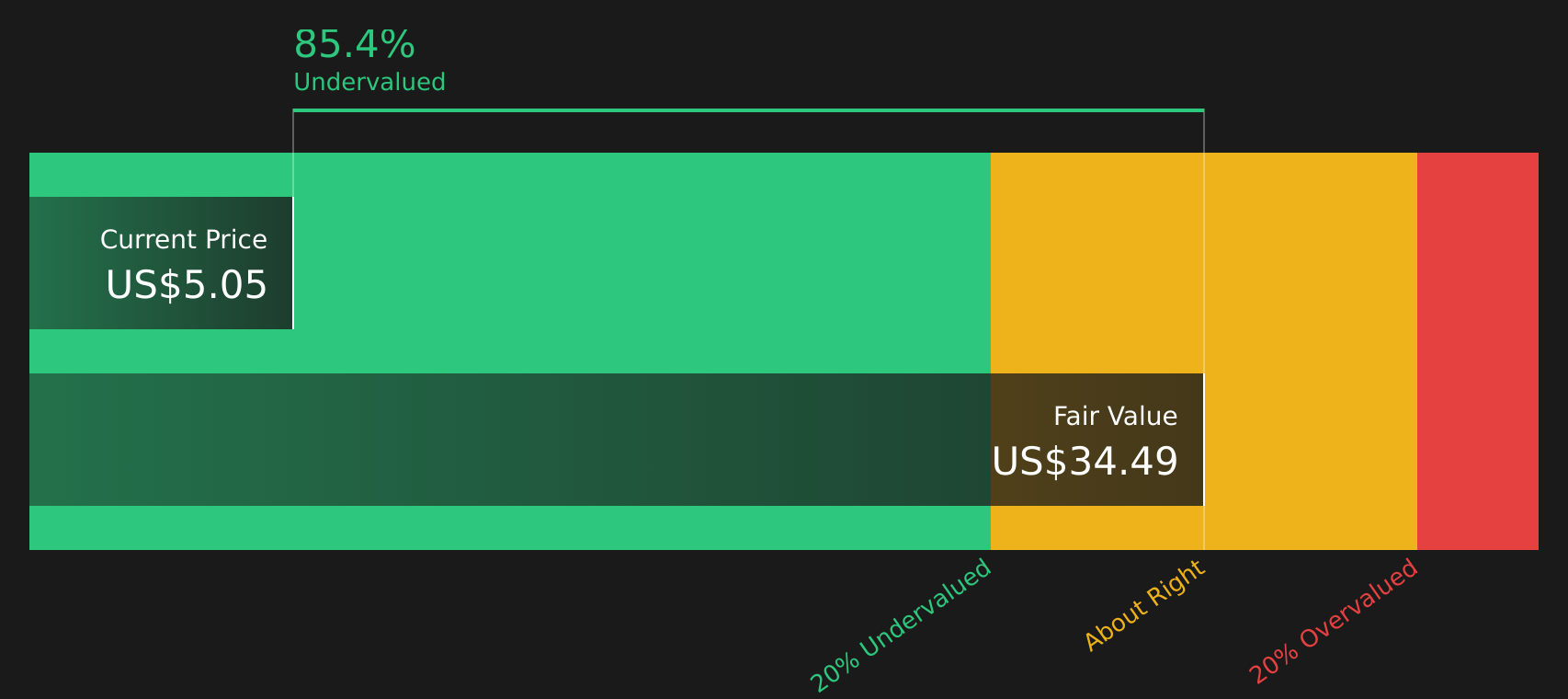

With JetBlue shares up 10.26% over 7 days but still showing a 74.88% decline over 5 years and trading at an estimated 85% discount to intrinsic value, is this a mispriced turnaround story, or is the market already factoring in future growth?

Most Popular Narrative: 7.2% Overvalued

JetBlue closed at $5.05 compared with a narrative fair value of $4.71, so the widely followed view sees the stock trading a bit ahead of its fundamentals.

The rebound in leisure travel and resilient demand, especially among Millennials and Gen Z prioritizing experiences, continues to drive close-in bookings and support premium cabin and loyalty revenue growth, which is likely to result in higher ticket revenues and topline expansion.

Want to see what justifies paying more than the fair value estimate for an unprofitable airline? The narrative leans heavily on steady revenue growth, gradual margin repair and a richer earnings multiple than the sector usually grants. Curious which combinations of growth, profitability and discount rate make that pricing work on paper?

Result: Fair Value of $4.71 (OVERVALUED)

However, this depends on demand remaining strong and fuel costs not eroding margins further, while higher labor expenses could still limit any meaningful earnings recovery.

Another Angle on Value: Sales Multiple vs DCF

There is a sharp split between methods here. On one hand, JetBlue screens as good value on a P/S of 0.2x versus 0.5x for both the global airlines industry and peers, and a fair ratio of 0.8x, which points to a wide valuation gap. Yet the SWS DCF model suggests the stock trades about 85% below its future cash flow value, which is a very large disconnect for you to weigh.

Next Steps

Mixed signals on value and sentiment so far? Take a closer look at the details, weigh the trade off between risk and reward, and check out 2 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop with one airline when a wider set of opportunities is just a few clicks away. Broadening your watchlist now could help you spot ideas others overlook.

- Spot potential value candidates early by scanning 49 high quality undervalued stocks, which combine lower prices with solid fundamentals.

- Strengthen your focus on balance sheet resilience by reviewing the solid balance sheet and fundamentals stocks screener (46 results), which may better handle financial stress.

- Hunt for off-the-radar potential by checking the screener containing 21 high quality undiscovered gems, which most investors are not watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.