A Look At Uniti Group (UNIT) Valuation As New Fiber Backed Debt Deal Reshapes Its Balance Sheet

Uniti Group Inc. UNIT | 0.00 |

Why Uniti Group’s new fiber-backed debt deal matters for shareholders

Uniti Group (UNIT) has priced about $1.14b of secured fiber network revenue term notes through subsidiary Kinetic ABS Issuer LLC, backed by residential fiber assets and customer agreements across multiple U.S. states.

The company plans to use the proceeds for general corporate purposes, including capital expenditures and repayment of outstanding debt. This directly affects its capital structure, interest costs, and financial flexibility for shareholders.

At a share price of $11.68, Uniti Group has given investors a 71.01% year to date share price return and a 61.88% total shareholder return over the past year. The recent fiber backed securitization and earlier ESOP related shelf registration have contributed to strong 90 day momentum of 41.75%, while the 5 year total shareholder return is still down 12.12%.

If this kind of move has you looking beyond a single stock, it could be a good moment to broaden your watchlist with 33 power grid technology and infrastructure stocks

With UNIT up 71.01% year to date and trading above the average analyst price target of US$10.25, you need to ask whether markets are already looking ahead or if this fiber backed financing still leaves room for a buying opportunity.

Most Popular Narrative: 14% Overvalued

With Uniti Group closing at $11.68 against a narrative fair value of $10.25, the current price sits above what this widely followed model suggests, which puts more focus on the assumptions behind that gap.

Improved capital structure through debt silo unification and proactive refinancing (blended debt yield down 550 bps in 2.5 years) is reducing interest expense and improving financial flexibility, setting the stage for greater net earnings and capacity to reinvest in growth initiatives.

Want to see why this narrative still lands on a higher required return, even with cheaper debt and fiber growth baked in? The entire framework hinges on measured revenue expansion, a margin reset from unusually high current levels, and a future earnings multiple that stays below many telecom peers. The full picture shows how those ingredients combine to produce a fair value below today’s price.

Result: Fair Value of $10.25 (OVERVALUED)

However, the story could shift quickly if higher fiber build costs squeeze cash flow or if heavy leverage and refinancing needs begin to weigh more heavily on sentiment.

Another way to look at Uniti Group’s value

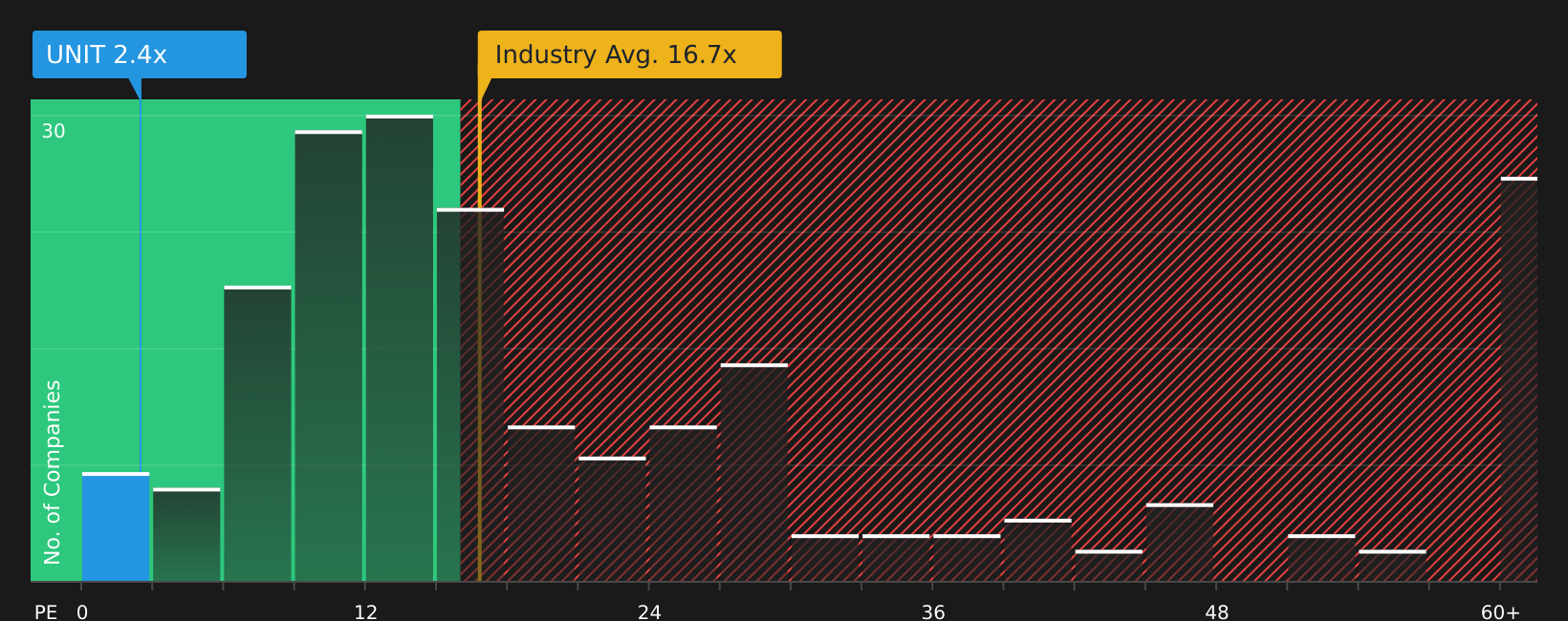

The analyst narrative flags Uniti Group as 14% overvalued versus a fair value of $10.25, yet the current P/E of 2.5x looks low compared with a fair ratio of 8.7x, a peer average of 9.2x and a global telecom average of 16.8x. So is the market rightly cautious, or leaving something on the table?

Next Steps

If this mixed picture of momentum and valuation leaves you undecided, quickly review the key data yourself. Then weigh up the 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If UNIT has your attention, do not stop here. Broadening your watchlist now could help you spot opportunities that others only notice much later.

- Target stability first by checking out 61 resilient stocks with low risk scores that aim to keep drawdowns in check while still offering room for long term compounding.

- Hunt for quality at a discount through screener containing 21 high quality undiscovered gems that combine solid fundamentals with relatively low market attention.

- Focus on financial resilience by scanning solid balance sheet and fundamentals stocks screener (46 results) so you can shortlist companies that are not weighed down by fragile balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.