Boot Barn Holdings (BOOT) Is Up 7.5% After Raising FY 2027 Guidance And Completing Buyback – What's Changed

Boot Barn Holdings, Inc. BOOT | 0.00 |

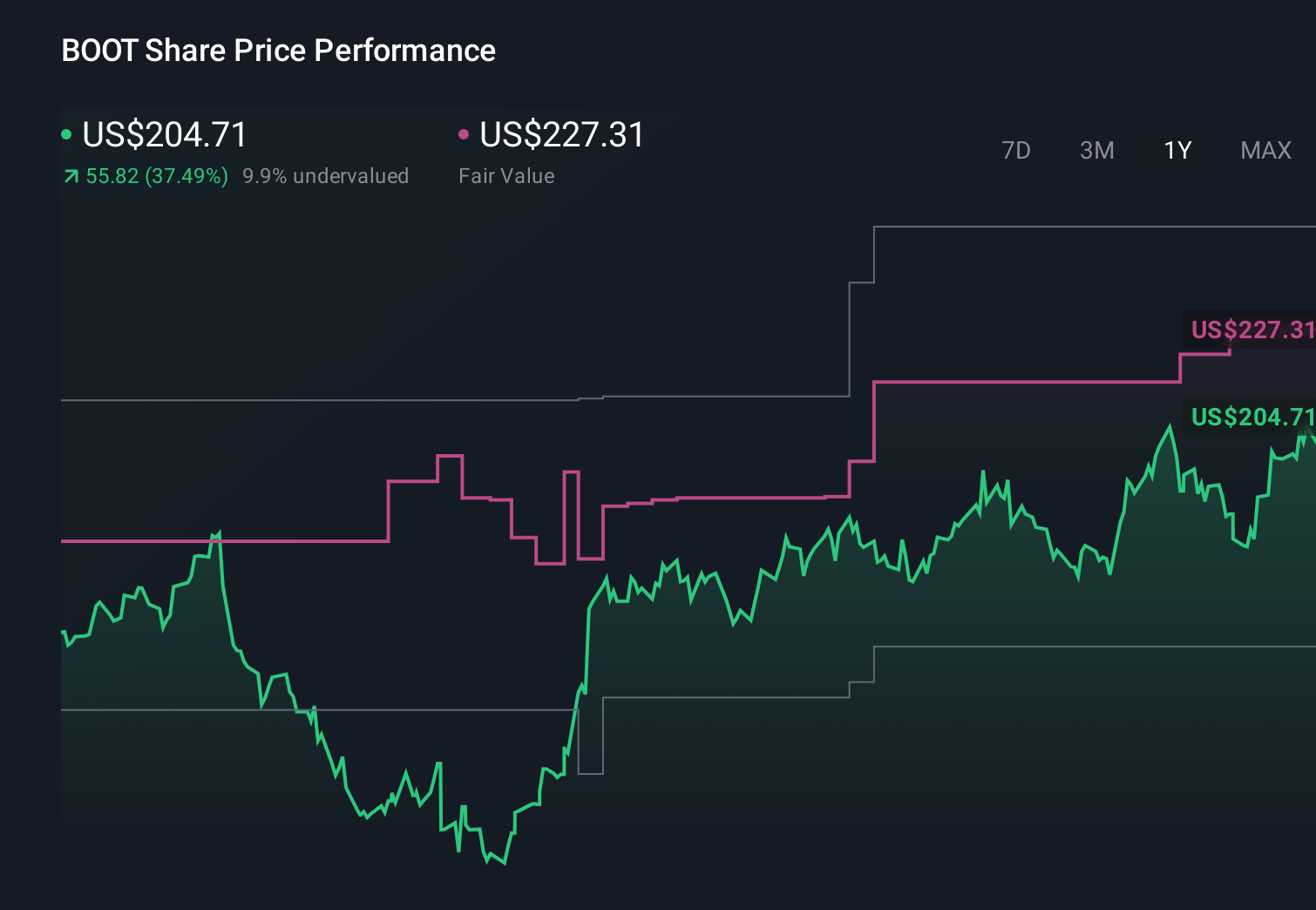

- In May 2026, Boot Barn Holdings reported full-year sales of US$2.25 billion and net income of US$225.88 million, alongside new guidance calling for higher sales, net income and same-store growth in fiscal 2027.

- Management also confirmed completion of a US$49.94 million share repurchase program while highlighting accelerating new store openings, expanding exclusive brands and strong e-commerce momentum as key earnings drivers.

- Building on this, we’ll now examine how the stronger earnings guidance and expanding exclusive brands reshape Boot Barn’s broader investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn, you need to believe that aggressive store expansion, growing exclusive brands and a still-relevant Western/workwear niche can keep supporting earnings, while avoiding overexpansion or fashion fatigue. The latest full-year results and higher fiscal 2027 guidance reinforce the near term catalyst around same-store and e-commerce growth, but they do not remove the key risk that rapid store openings could eventually pressure returns if newer markets underperform.

The most relevant update here is Boot Barn’s new fiscal 2027 guidance, calling for US$2.578 billion to US$2.623 billion in sales and net income of US$251.1 million to US$264.5 million. This directly ties to the earnings catalyst behind store growth and exclusive brands, while giving investors clearer signposts on how consolidation of physical locations and faster e-commerce same-store sales might offset risks from higher costs or changing customer behavior.

Yet against this stronger outlook, investors should still be aware that rapid store expansion could eventually...

Boot Barn Holdings' narrative projects $3.3 billion revenue and $350.9 million earnings by 2029. This requires 13.9% yearly revenue growth and a roughly $125 million earnings increase from $225.9 million today.

Uncover how Boot Barn Holdings' forecasts yield a $225.14 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$3.3 billion with earnings of roughly US$370 million, which leans heavily on continued margin gains from exclusive brands and efficient expansion. Compared with the baseline narrative, this is a much more optimistic view that amplifies both the upside from private brand execution and the risk that heavy store investment might clash with rising e-commerce expectations after the latest guidance.

Explore 3 other fair value estimates on Boot Barn Holdings - why the stock might be worth 46% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.