يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Does Delta’s Entry Into Riyadh With Nonstop Flights Shift the Long-Term Story for DAL?

Delta Air Lines, Inc. DAL | 67.10 | -0.21% |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

If you are considering investing in Delta Air Lines, the long-term thesis centers on the company’s ability to protect margins and free cash flow by aligning supply with demand, while leaning into premium, loyalty, and international travel to drive revenue. The recent announcement of new nonstop service to Riyadh expands Delta’s international presence, but is not expected to materially impact the main short-term catalyst: the resilience of demand in premium and international segments. The greatest near-term risk remains potential softening in core domestic travel and main cabin demand, which could pressure Delta’s margins if economic uncertainty persists.

Among Delta’s recent announcements, the expansion of the maintenance, repair, and overhaul (MRO) partnership with UPS stands out as most relevant to the airline’s effort to diversify revenue streams and manage costs, supporting the margin protection that underpins its investment thesis. While international route additions like Atlanta to Riyadh capture headlines, long-term agreements like the UPS deal strengthen Delta’s position beyond passenger travel, especially if passenger demand slows.

By contrast, investors should also be mindful of the risk posed by...

Delta Air Lines' narrative projects $68.4 billion revenue and $4.6 billion earnings by 2028. This requires 3.4% yearly revenue growth and a $0.1 billion earnings increase from $4.5 billion.

Uncover how Delta Air Lines' forecasts yield a $71.75 fair value, a 22% upside to its current price.

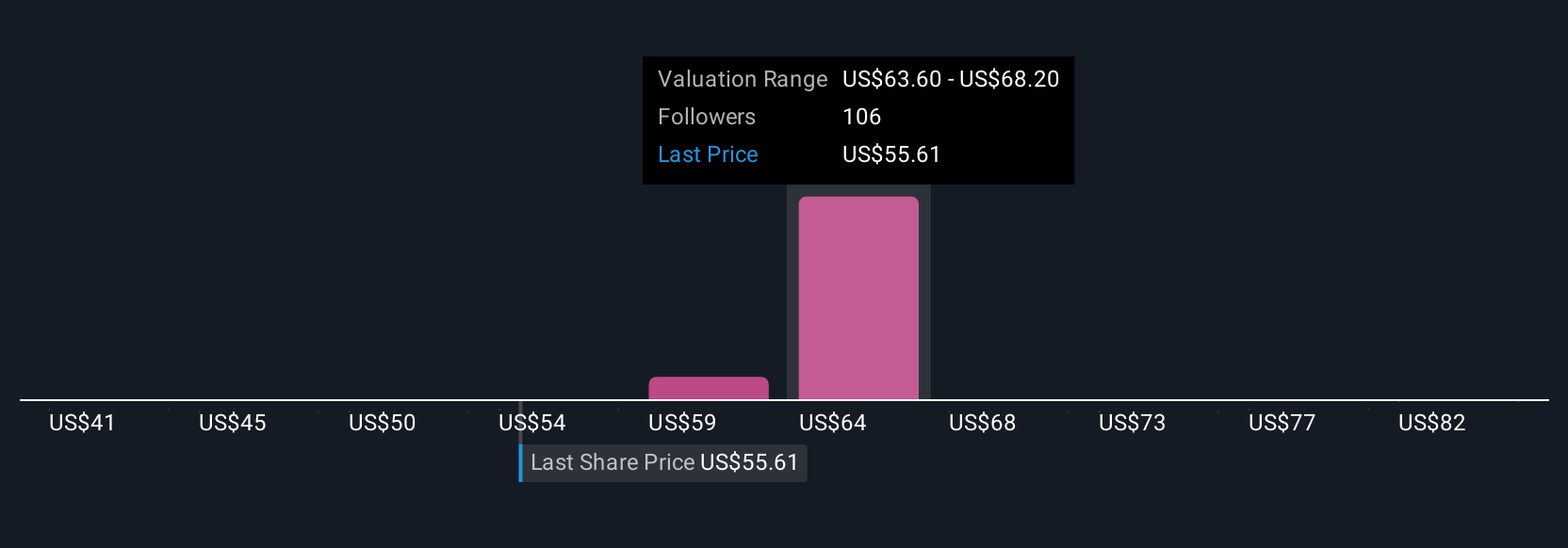

Eight individual fair value estimates from the Simply Wall St Community range from US$41 to US$100 per share. While some see substantial upside, the underlying risk of softer main cabin demand could shape future results in ways that are top of mind for many market participants.

Explore 8 other fair value estimates on Delta Air Lines - why the stock might be worth 31% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Opportunities like this don't last. These are today's most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.