Evaluating Lakeland Financial (LKFN) Valuation As Recent Share Performance Sends Mixed Signals

Lakeland Financial Corporation LKFN | 0.00 |

Stock moves and recent performance context

Lakeland Financial (LKFN) has drawn fresh attention after its share price closed at US$59.99, with recent returns mixed, up over the past 3 months but down over the past month and modestly positive over the past year.

Short term, the stock has seen mixed share price momentum, with a 1-day share price return of 1.17% and a 90-day share price return of 5.77%. The 1-year total shareholder return of 1.72% points to relatively muted longer term gains.

If Lakeland Financial’s move has you thinking about where else value might be hiding in financials, this could be a good moment to widen your search using the 20 top founder-led companies

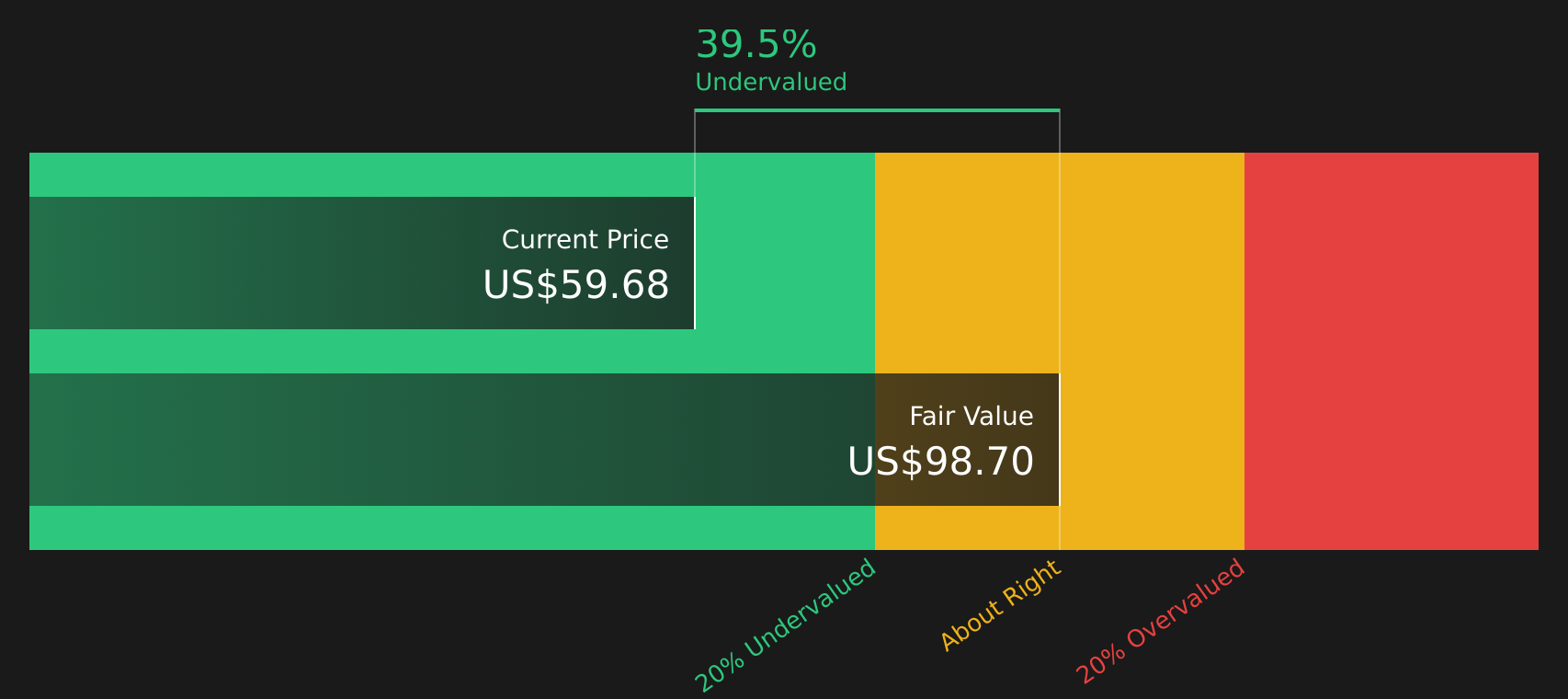

With Lakeland Financial trading at US$59.99, an indicated intrinsic discount of about 39% and a modest 1 year total return, the real question for you is whether this is a genuine value opening or if the market is already factoring in its growth potential.

Preferred Price-to-Earnings of 13.6x: Is it justified?

On a P/E of 13.6x, Lakeland Financial trades at a higher earnings multiple than the US Banks industry average of 11.6x, yet below the peer average of 14.7x and below an estimated fair P/E of 10.4x.

The P/E ratio compares the share price with earnings per share, so it gives you a quick sense of how much investors are paying for each dollar of current earnings. For a bank like Lakeland Financial, where profits and balance sheet strength are central, this is a widely watched benchmark.

Here, the market is valuing the stock more highly than the broader US Banks industry, which suggests investors are paying a premium for its earnings. However, the P/E also sits above the modelled fair ratio of 10.4x, a level the market could move towards if sentiment cools or earnings do not keep pace. At the same time, the P/E is below the 14.7x peer average, which presents Lakeland Financial as cheaper than similar companies that trade at higher earnings multiples.

Result: Price-to-Earnings of 13.6x (OVERVALUED)

However, the higher P/E and only modest 1-year total return mean that any setback in earnings or sector sentiment could quickly challenge the current valuation case.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Point to Undervaluation

While the P/E of 13.6x presents Lakeland Financial as expensive compared with both the US Banks industry and its own fair ratio of 10.4x, the SWS DCF model indicates a different perspective, with an estimated future cash flow value of about $98.70 per share versus the current $59.99 price.

This gap presents the stock as trading well below that cash flow estimate. It raises a key question for you: is the market too cautious on Lakeland Financial, or is the model too optimistic about its long term earnings power?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lakeland Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value, risk, and cash flow, the real edge is in seeing the details yourself and acting before sentiment shifts. To weigh up both the potential upsides and the concerns flagged by the market, start by checking the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Lakeland Financial is on your radar, do not stop there. Broaden your opportunity set so you are not relying on just one stock for potential returns.

- Target resilience by screening for companies with steady finances and staying power through the 63 resilient stocks with low risk scores.

- Hunt for potential bargains by focusing on quality stocks that trade below their assessed worth using the 48 high quality undervalued stocks.

- Zero in on underfollowed opportunities by scanning a screener containing 21 high quality undiscovered gems that might not yet be crowded with attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.