Has Flowers Foods (FLO) Fallen Too Far After Sharp One-Year Share Price Slide?

Flowers Foods, Inc. FLO | 0.00 |

- If you are wondering whether Flowers Foods at around US$7.94 is a bargain or a value trap, the answer starts with understanding how its current price stacks up against a few simple valuation checks.

- The stock has been volatile, with a rise of 10.6% over the past week but declines of 9.3% over the past month, 26.4% year to date, and 47.7% over the last year, which can change how investors think about both risk and opportunity.

- Recent coverage has focused on how this long slide in the share price and the current level around US$7.94 compare with the underlying business. Some commentators are asking whether the market reaction has gone too far or not far enough, which makes valuation the key question for anyone considering the stock today.

- On Simply Wall St's framework, Flowers Foods scores 3 out of 6 on the valuation checks, which you can see in detail via its valuation score. The rest of this article will walk through those methods, then finish with a broader way to think about what the valuation really means for you as an investor.

Approach 1: Flowers Foods Discounted Cash Flow (DCF) Analysis

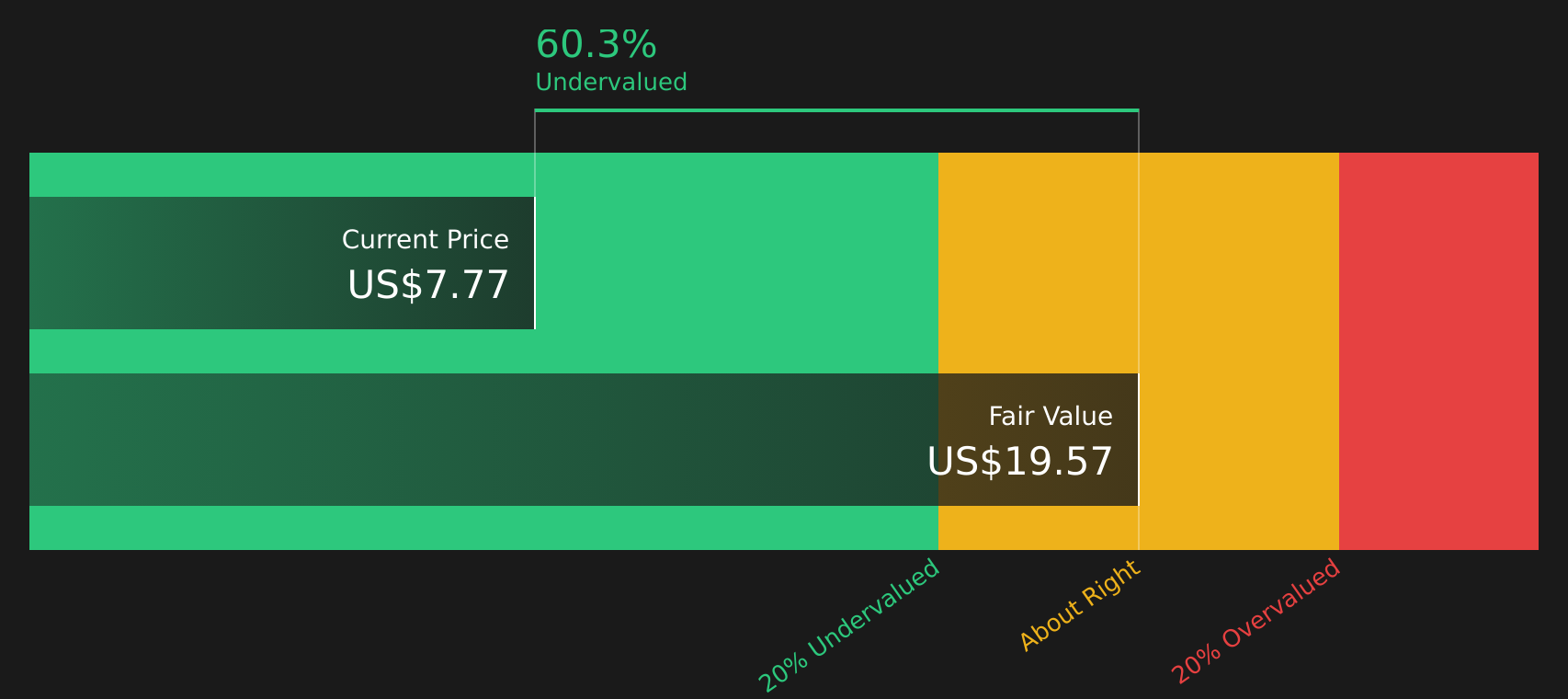

A Discounted Cash Flow, or DCF, model takes the cash that a company is expected to generate in the future and discounts those amounts back to today, aiming to estimate what the entire business might be worth right now.

For Flowers Foods, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model based on cash flow projections. The latest twelve month Free Cash Flow is around $305.63 million. Analysts provide estimates out to 2028, with projected Free Cash Flow of $174 million in that year, and Simply Wall St extrapolates out to 2035 using its own assumptions. All of these future cash flows are then discounted back into today's dollars.

On this basis, the DCF model produces an estimated intrinsic value of $15.02 per share. Compared with the current share price around $7.94, this implies the stock is trading at about a 47.1% discount to that DCF estimate, indicating that the market price is well below this model's view of underlying value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Flowers Foods is undervalued by 47.1%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: Flowers Foods Price vs Earnings

For a profitable company, the P/E ratio is a useful way to see how much investors are paying for each dollar of current earnings. It links directly to what you receive as an owner, because earnings can be paid out as dividends or reinvested to support the business.

What counts as a normal or fair P/E depends on how the market views a stock's growth prospects and risks. Higher expected growth or lower perceived risk often supports a higher P/E, while lower growth expectations or higher risk usually align with a lower P/E.

Flowers Foods currently trades on a P/E of 20.07x. That sits slightly above the Food industry average P/E of about 18.64x and well below a peer group average of 45.85x. Simply Wall St's Fair Ratio model, which incorporates factors such as earnings growth, industry, profit margin, market cap and risk profile, suggests a Fair P/E of 19.68x for Flowers Foods. This company specific Fair Ratio is more tailored than a simple comparison with industry or peers because it adjusts for the characteristics that make Flowers Foods different from other stocks.

With a current P/E of 20.07x versus a Fair Ratio of 19.68x, the stock screens as slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Flowers Foods Narrative

Earlier the article mentioned that there is an even better way to understand valuation, and Simply Wall St calls it a Narrative. This is basically your story about Flowers Foods linked directly to a forecast and a fair value. For example, one investor on the Community page sees M&A, Simple Mills and new products supporting a fair value of US$16.12 per share. Another, more cautious investor focuses on slower revenue, modest margin uplift and regulatory and competition risks and lands closer to US$7.00. A third sits around the analyst consensus near US$10.67. Each Narrative uses different assumptions for future revenue, earnings, margins and P/E to produce a fair value that you can compare with the current price. The platform then updates those Narratives automatically when new earnings, guidance, news or price targets are added. This makes it a simple, visual way for you to decide whether the stock looks cheap or expensive without getting stuck on a single DCF or P/E number.

For Flowers Foods however we will make it really easy for you with previews of two leading Flowers Foods Narratives:

Fair value in this bull case: US$16.12 per share

Implied discount to this fair value based on the recent US$7.94 share price: about 50.7% below the narrative fair value

Revenue outlook used in this Narrative: 1.15% growth per year

- M&A, including the US$800m Simple Mills deal funded with senior debt, is central to the thesis that Flowers Foods can expand into health focused brands and improve margins over time.

- New Wonder branded snack products and a management refresh are treated as potential supports for both brand strength and operational efficiency while the company works through recent earnings pressure.

- The author highlights a higher dividend yield and recent dividend uplift as important for investors who care about income while weighing the added balance sheet risk from the extra debt.

Fair value in this bear case: US$7.00 per share

Implied premium to this fair value based on the recent US$7.94 share price: about 13.4% above the narrative fair value

Revenue outlook used in this Narrative: revenue is assumed to decline about 0.55% per year

- The bear author starts from the view that long running changes in diet, health concerns around processed foods and demographic trends could leave the core packaged bread market structurally smaller.

- Higher regulation risk, strong private label and local competitors and a slower shift away from legacy brands are treated as ongoing headwinds for margins, pricing power and volume.

- The fair value of US$7.00 assumes only modest profit margin improvement, a lower future P/E multiple than the sector and relatively flat revenue, which together keep the long term earnings outlook restrained.

Putting these side by side gives you a ready made range, with one Narrative tying the recent share price slide to a case for recovery and another that leans into a tougher long term backdrop for traditional bakery products. The key step now is to decide which set of assumptions feels closer to how you see the business and its risks.

Do you think there's more to the story for Flowers Foods? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.