يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

How Warrior Met Coal’s Expanded Credit Facility Could Shape Growth Prospects for HCC Investors

Warrior Met Coal, Inc. HCC | 81.61 | -1.21% |

The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

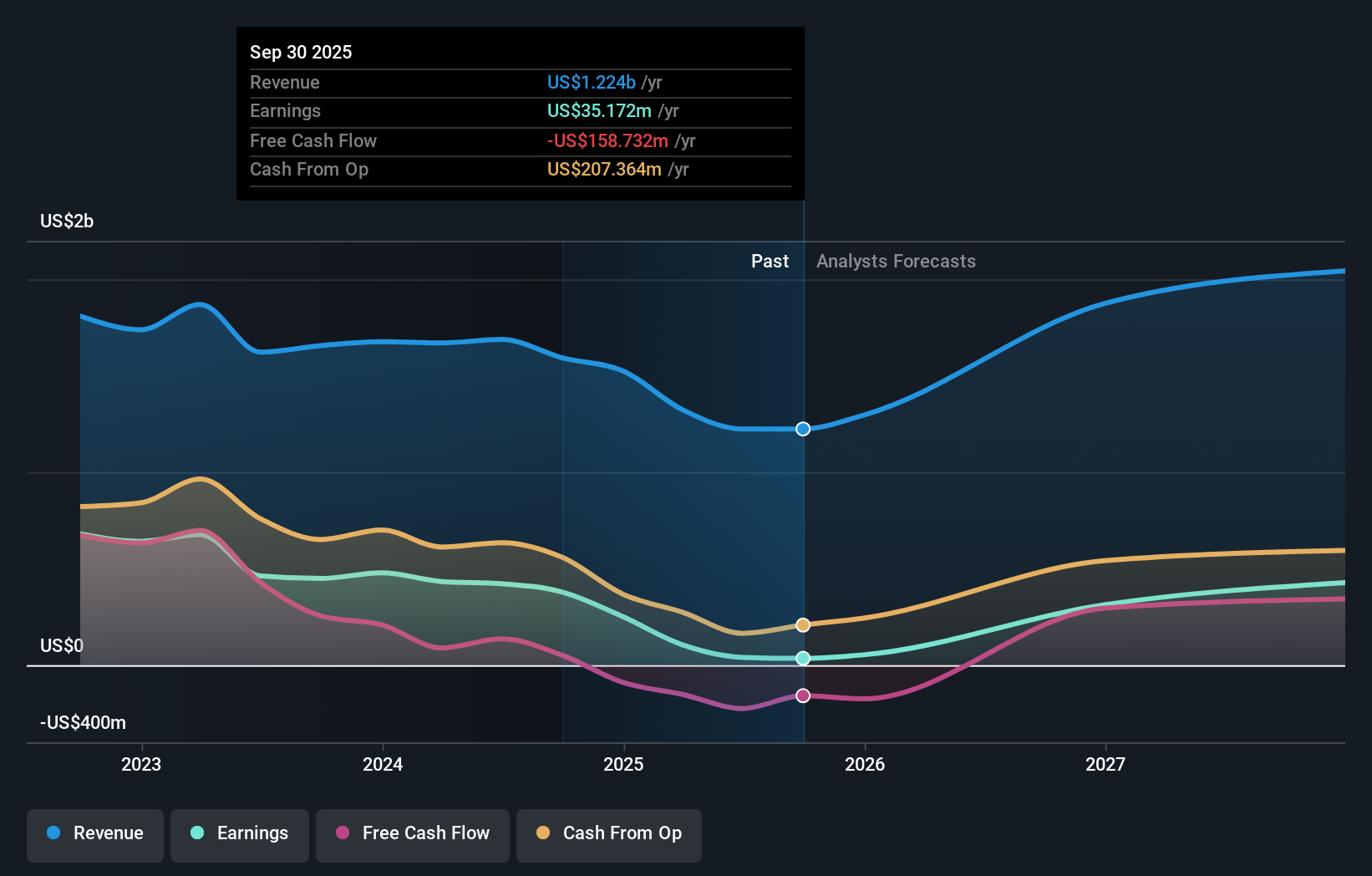

To own Warrior Met Coal, you need to believe in a meaningful rebound in steelmaking coal demand, especially as Blue Creek’s ramp-up drives higher sales volumes and improved cost efficiency. The expanded credit facility offers extra liquidity, which could help fund operations as Blue Creek moves toward first tonnage, but persistent coal price pressures remain the biggest risk in the near term, this facility alone does not materially offset commodity-driven risks.

Of Warrior's recent updates, the August 2025 production guidance stands out: expectations for 8.3 million to 9.1 million short tons of output underscore management’s confidence despite weak revenue and earnings this year. The rising borrowing base supports this ambition, but it will only matter if higher volumes translate into stronger sales as Blue Creek comes online.

By contrast, investors should keep in mind that new credit lines are helpful, but they do not erase the risk of mounting capital intensity and uncertain placement of Blue Creek volumes if...

Warrior Met Coal's outlook anticipates $2.0 billion in revenue and $636.5 million in earnings by 2028. This projection is based on an expected 18.8% annual revenue growth rate and a $596 million increase in earnings from the current $40.3 million.

Uncover how Warrior Met Coal's forecasts yield a $65.67 fair value, a 13% upside to its current price.

Five members of the Simply Wall St Community value Warrior Met Coal between US$65.67 and US$209.47 a share. While many expect profit growth to accelerate as Blue Creek delivers, the wide range of estimates shows just how much your outlook on demand and execution can shape expectations for this stock.

Explore 5 other fair value estimates on Warrior Met Coal - why the stock might be worth just $65.67!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.