Western Midstream Partners (WES) Valuation Check After Earnings Beat Dividend Growth And 52-Week High

Western Midstream Partners, LP WES | 0.00 |

Western Midstream Partners (WES) is back in focus after first quarter 2026 results topped analyst expectations, helping the stock reach a fresh 52 week high and extending a four year streak of dividend increases.

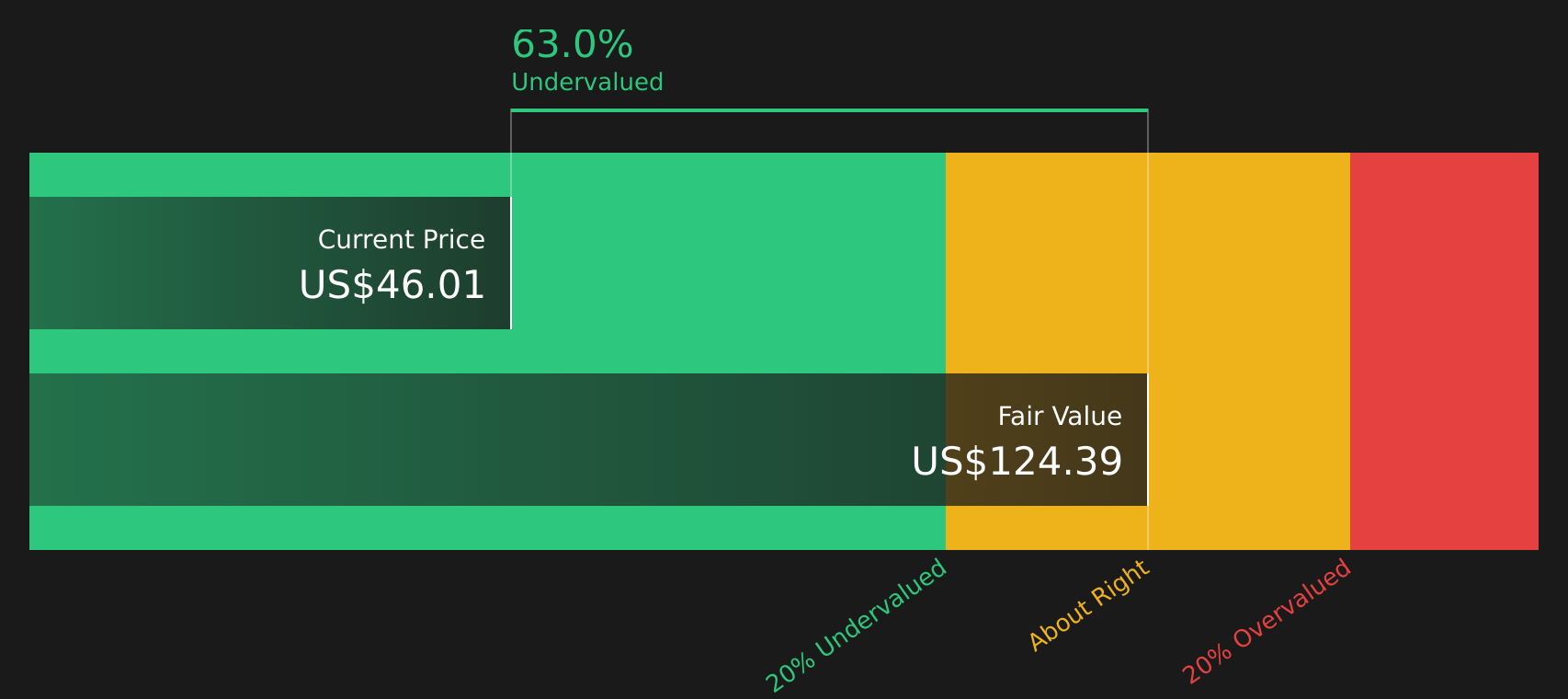

At a share price of $46.01, Western Midstream Partners has logged a 12.44% 1 month share price return and a 15.84% year to date share price return. The 1 year total shareholder return of 29.33% and 5 year total shareholder return of 249.79% suggest momentum has been building alongside recent earnings and dividend news.

If strong recent performance has you reassessing your watchlist, it could be a good moment to widen your search with 35 power grid technology and infrastructure stocks

With the stock near a 52 week high, a value score of 4, and an intrinsic value estimate implying roughly a 63% discount, investors have to ask: is this a genuine mispricing, or is the market already looking ahead and pricing in future growth?

Most Popular Narrative: 10% Overvalued

Western Midstream Partners last closed at $46.01, while the most followed narrative anchors fair value closer to $41.83, highlighting a gap investors will want to understand.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.5 billion, earnings will come to $1.6 billion, and it would be trading on a PE ratio of 15.8x, assuming you use a discount rate of 7.2%.

Curious what underpins that valuation gap? The narrative leans on steady revenue growth, higher margins, and a richer future earnings multiple. The mix may surprise you.

Result: Fair Value of $41.83 (OVERVALUED)

However, even this popular narrative could be shaken if large capital projects face delays or cost overruns, or if producer activity and volumes weaken more than expected.

Another Take: Cash Flows Point a Very Different Way

Analysts see Western Midstream Partners trading about 10% above their $41.83 fair value, yet the SWS DCF model presents a very different picture, with an estimated future cash flow value of $124.14 per unit that implies the units are deeply undervalued. When earnings based and cash flow based signals disagree this sharply, which one do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Western Midstream Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals around value and future expectations, it makes sense to move quickly and check the underlying numbers yourself before opinions harden. To see both sides of the story in one place, start with 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Western Midstream Partners has sharpened your thinking, do not stop here. Broaden your watchlist with a few targeted stock ideas that fit different priorities.

- Target higher income potential by scanning for companies that resemble yield focused fortresses using the 10 dividend fortresses.

- Hunt for quality at a reasonable price by running a search for companies that look like 49 high quality undervalued stocks.

- Prioritise resilience by filtering for businesses that match the profile of the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.