Why Southwest Airlines (LUV) Is Up 6.1% After Expanding Its Aircraft-Backed Term Loan Facility

Southwest Airlines Co. LUV | 0.00 |

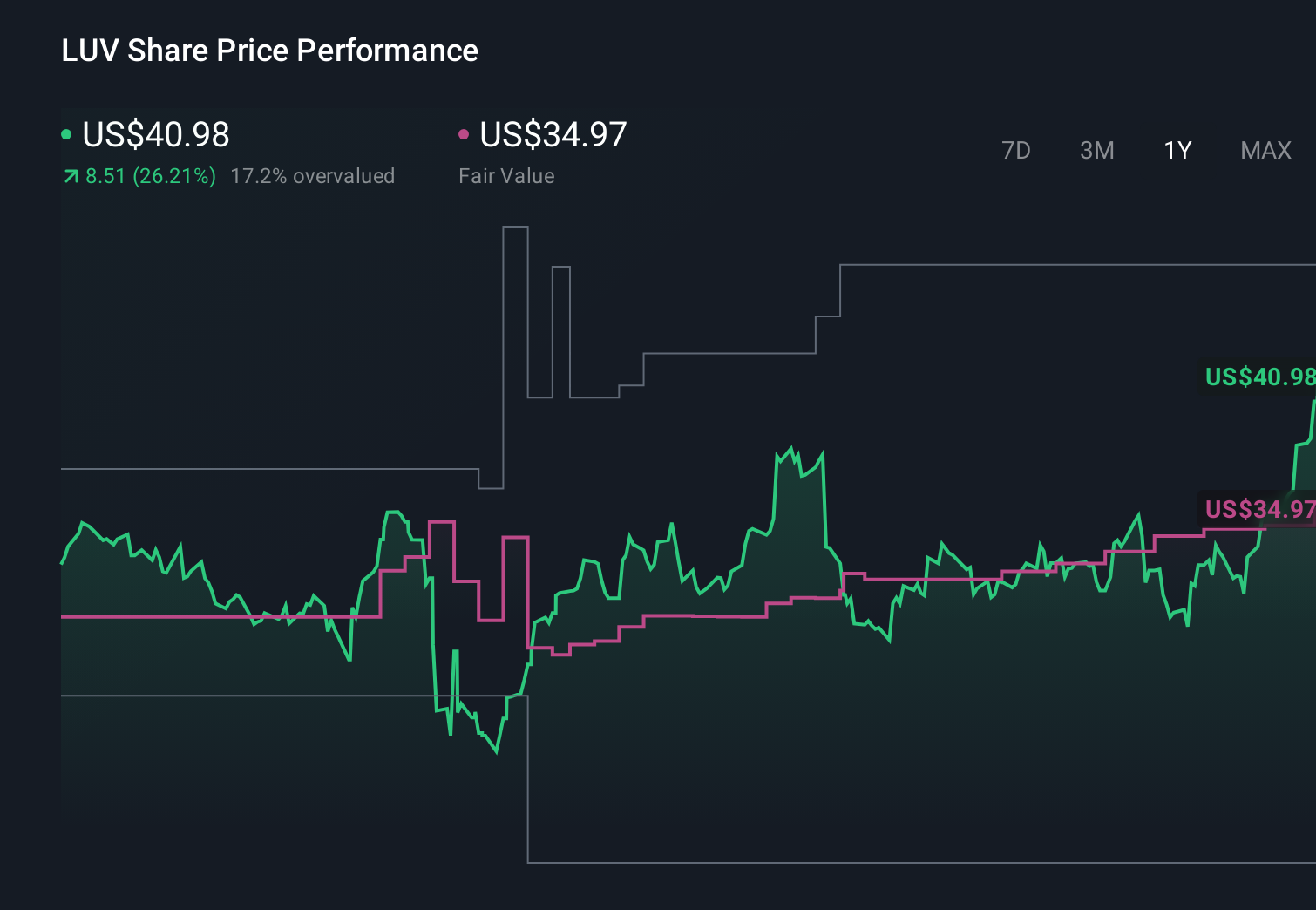

- Southwest Airlines recently expanded its senior secured term loan facility by US$1.0 billion to US$1.5 billion in total, with aircraft and related assets pledged as collateral and the loans maturing on March 11, 2029, while remaining prepayable without penalty.

- This financing move, coupled with flexibility to adjust the collateral pool and add up to another US$1.0 billion in future term loans, materially increases Southwest’s liquidity options and balance sheet resilience at a time of ongoing industry uncertainty.

- We’ll now examine how this expanded, aircraft-backed term loan facility reshapes Southwest Airlines’ investment narrative, particularly around liquidity and earnings flexibility.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Southwest Airlines Investment Narrative Recap

To own Southwest, you generally need to believe its low cost model, product changes, and loyalty ecosystem can translate into resilient earnings, even as leisure demand and booking trends remain choppy. The expanded US$1.5 billion aircraft backed term loan mainly reinforces liquidity and cushions near term turbulence around demand and fuel costs, but it does not directly change the key short term catalyst of monetizing new fare products, or the major risks around macro uncertainty and Boeing delivery timing.

In that context, the recent Q1 2026 update is highly relevant: Southwest generated US$7.249 billion of quarterly revenue and returned to profitability with US$227 million of net income. Those results sit alongside guidance for Q2 2026 revenue per available seat mile growth, which many shareholders are watching closely as a proof point that fare changes, distribution via Expedia, and loyalty program tweaks can offset cost pressures and softer booking visibility.

Yet, investors should also be aware that if domestic demand softens at the same time as labor and fuel costs stay elevated, the cushion from this new term loan could...

Southwest Airlines' narrative projects $34.5 billion revenue and $2.3 billion earnings by 2029. This requires 6.1% yearly revenue growth and about a $1.5 billion earnings increase from $817.0 million today.

Uncover how Southwest Airlines' forecasts yield a $45.25 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$36.6 billion of revenue and US$2.7 billion of earnings by 2029, which is a far more bullish story than consensus. When you compare that optimism with concerns around an aging, single type Boeing 737 fleet and rising maintenance and labor costs, the new US$1.5 billion term loan could either support that upside case or prompt those forecasts to be revisited.

Explore 4 other fair value estimates on Southwest Airlines - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southwest Airlines research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 28 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.