Please use a PC Browser to access Register-Tadawul

Get It

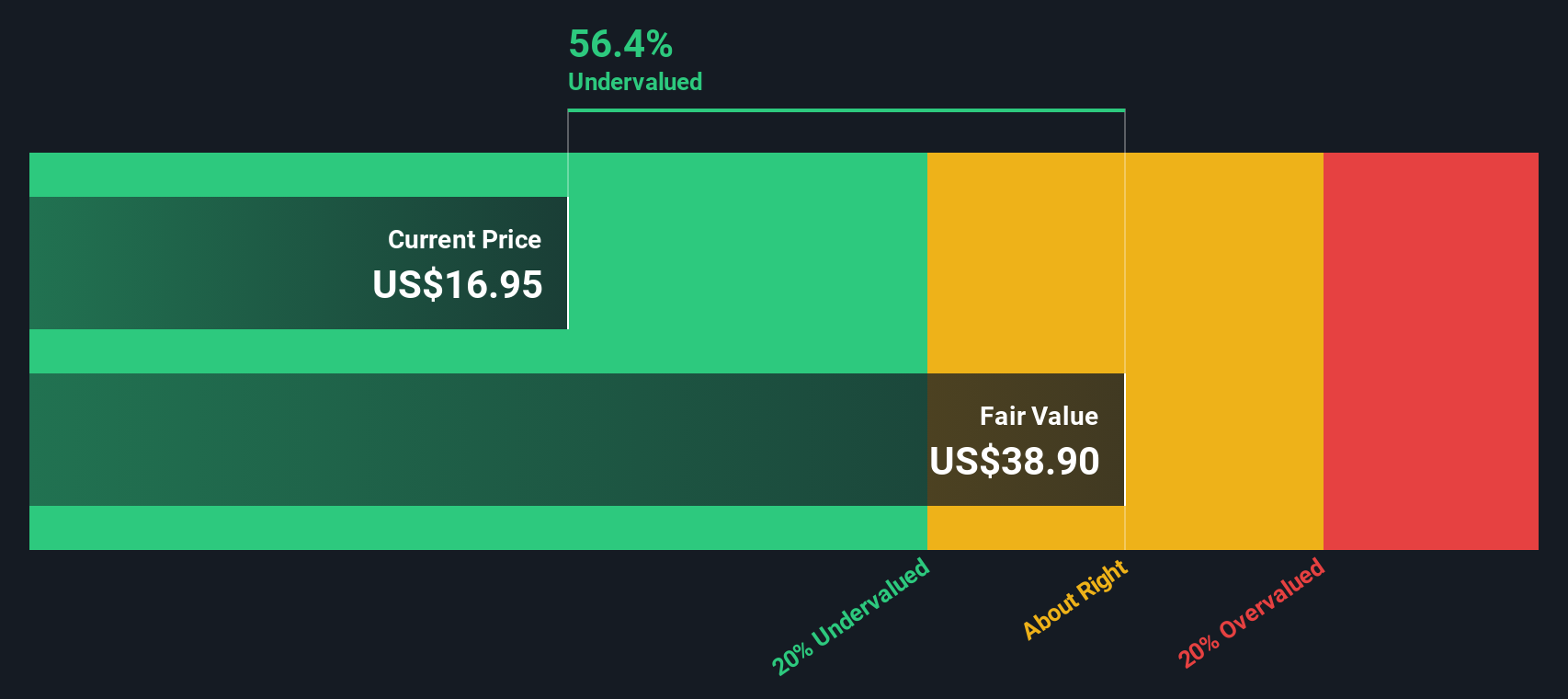

A Fresh Look at Albertsons (ACI) Valuation Following $4 Billion Credit Facility Expansion

Albertsons Companies, Inc. ACI | 17.22 | -2.49% |

According to the most widely followed narrative, Albertsons Companies is considered meaningfully undervalued, with the current market price at a steep discount to projected fair value.

Modernization through technology investments, such as automation, AI-driven inventory and pricing, and centralized buying, are streamlining operations, reducing labor and supply chain costs, and positioning the company for long-term margin expansion and improved net earnings.

Want to know what’s fueling this big price gap? Analysts are betting on game-changing growth levers, a profit surge, and a future valuation multiple that challenges the industry norm. Curious how ambitious these assumptions get, or which trends they think will move the needle most? Discover the bold projections at the heart of this fair value estimate.

Result: Fair Value of $24.19 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, slower e-commerce scaling and rising labor costs could undermine margin gains. This may potentially slow down Albertsons Companies’ momentum despite its digital and pharmacy growth.

Find out about the key risks to this Albertsons Companies narrative.Taking a step back from analyst targets, our DCF model looks at Albertsons Companies from a different perspective and also signals the stock is undervalued. However, does this approach paint the full picture?

Look into how the SWS DCF model arrives at its fair value.

If you see the story differently, or want to dig deeper into the numbers yourself, you can craft your own perspective in just a few minutes. Do it your way

A great starting point for your Albertsons Companies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

If you want to uncover fresh opportunities and stay a step ahead, don’t miss out on new trends and standout stocks using the Simply Wall St screener tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.