Assessing DuPont (DD) Valuation As XPRIZE Water Scarcity And Osmotic Energy Exposure Draw Interest

E. I. du Pont de Nemours and Company DD | 0.00 |

DuPont de Nemours (DD) is back on investor radars after its desalination technology, through the DESAL4ALL consortium, advanced to the XPRIZE Water Scarcity semifinals, alongside growing attention on its role in osmotic energy.

The recent XPRIZE Water Scarcity progress and the attention on osmotic energy come against a backdrop where DuPont de Nemours has a 1-month share price return of 4.65% and a year-to-date share price return of 17.74%. Its 1-year total shareholder return of 74.25% points to strong longer-term momentum despite a 3-month share price return that is down 4.54%.

If this kind of water and energy theme interests you, it can be worth casting a wider net and checking out 35 power grid technology and infrastructure stocks

With DuPont trading at US$48.12 alongside an intrinsic value estimate and analyst targets that sit higher, the key question for you is simple: is there still mispricing here, or has the market already baked in future growth?

Most Popular Narrative: 14.3% Undervalued

The most followed narrative puts DuPont de Nemours' fair value at $56.13 per share compared with the last close of $48.12. It frames the latest water news inside a bigger valuation story built on long term cash flow assumptions.

Persistent strength and investment in Healthcare & Water, driven by surging global demand for clean water solutions and healthcare products, leverages favorable demographic, sustainability, and infrastructure trends to drive above peer organic revenue growth and margin stability.

Curious what sits behind that valuation gap. The narrative leans on a specific earnings path, tighter margins, and a future profit multiple that assumes investors keep paying up for this mix of water technology and specialty materials.

Result: Fair Value of $56.13 (UNDERVALUED)

However, you also need to keep an eye on PFAS litigation and the impact of portfolio moves such as Qnity and possible divestitures, which could reshape future earnings.

Another View: Rich On Earnings Multiples

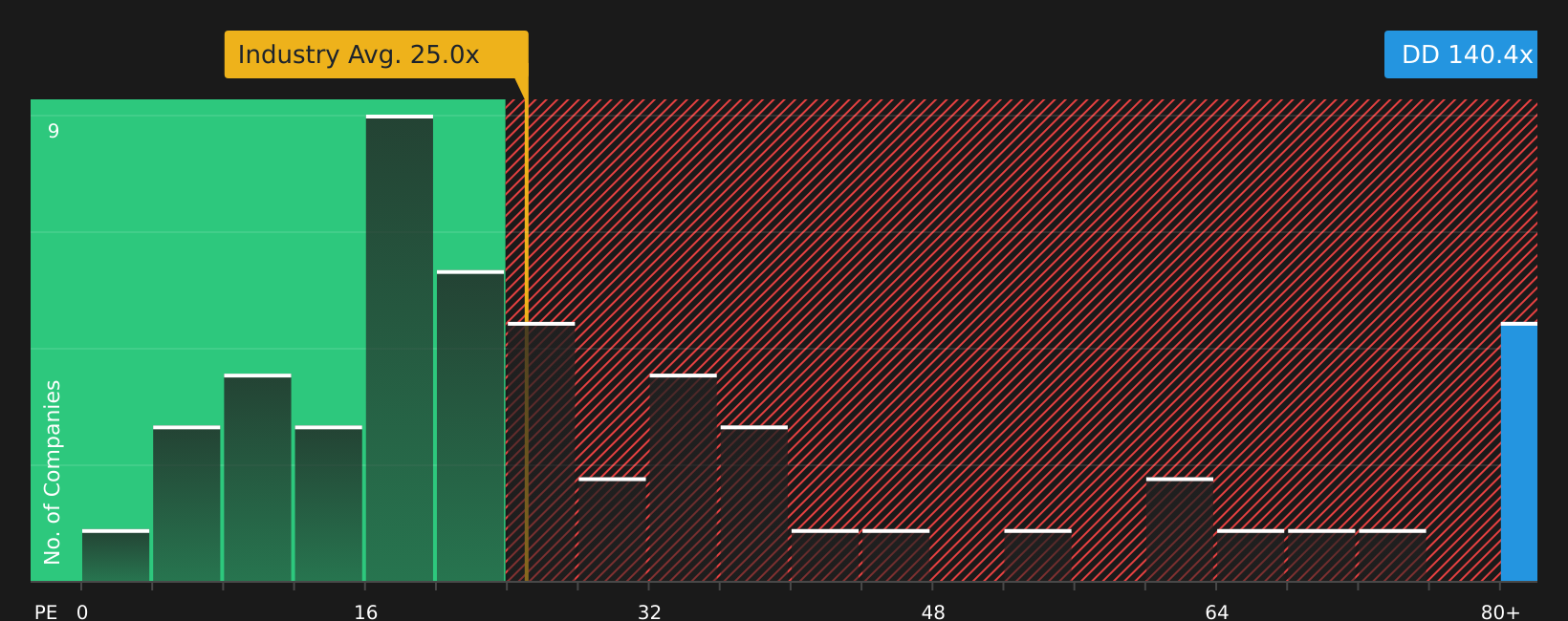

That $56.13 fair value hinges on long term cash flows, but the current P/E of 149.4x tells a different story. It sits well above the US Chemicals industry at 27x, the peer average at 36.6x, and even the 32.5x fair ratio the market could move toward. This raises the risk that any earnings wobble could hit the share price hard.

To see how this earnings based view compares with the cash flow case, it is worth checking the full valuation breakdown, including how the market is currently pricing similar companies, in See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment split between enthusiasm over growth themes and concern about litigation and valuation, it makes sense to move quickly and weigh the full picture yourself. You can start with the company's 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you could miss out on opportunities that better fit your goals, risk comfort, and income needs across the market.

- Target potential mispricing by scanning for quality companies trading below their estimated worth through the 49 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies in the 10 dividend fortresses that offer higher yields with a focus on durability.

- Prioritize resilience by checking stocks in the 66 resilient stocks with low risk scores that score well on financial stability and lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.