Assessing Ecolab (ECL) Valuation After Recent Pullback And Mixed Long Term Returns

Ecolab ECL | 0.00 |

Ecolab stock performance snapshot and business context

Ecolab (ECL) has been relatively steady in the short term, with the stock up about 1.4% over the past month and about 3% over the past week, while returns over the past 3 months declined roughly 8.3%.

At a recent close of US$257.97, the company carries a market value of about US$72.6b. Its business is anchored by a portfolio that spans water treatment, hygiene, infection prevention, pest elimination and life sciences solutions across global industrial and institutional customers.

Looking beyond the recent pullback, Ecolab’s share price return over the past year is slightly down. However, the 3 year total shareholder return of 48.70% and 5 year total shareholder return of 27.54% point to a stronger longer term record.

If you are comparing Ecolab’s profile with other opportunities, this is a good moment to scan for AI infrastructure suppliers and related enablers using the 48 AI infrastructure stocks

With steady revenue and net income growth alongside a recent pullback, the key question is whether Ecolab’s current valuation already reflects its prospects, or if the recent weakness hints at a potential opportunity that markets have not fully priced in.

Most Popular Narrative: 18.5% Undervalued

The most followed Ecolab narrative places fair value at about $316, above the recent $257.97 close, framing the stock as undervalued on that model.

Ecolab is focusing on expanding its One Ecolab growth initiative, aiming to capitalize on market share gains and increased value pricing. This initiative is expected to drive revenue growth and improve net margins by delivering exceptional value to customers.

Want to see what sits behind that pricing power story? The narrative leans on steady top line expansion, rising margins and a premium earnings multiple. Curious how those pieces fit together into a single fair value number?

Result: Fair Value of $316 (UNDERVALUED)

However, this pricing power story can be knocked off course if industrial demand stays soft or if tariffs and higher local supplier costs squeeze margins more than expected.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View on Ecolab’s Valuation

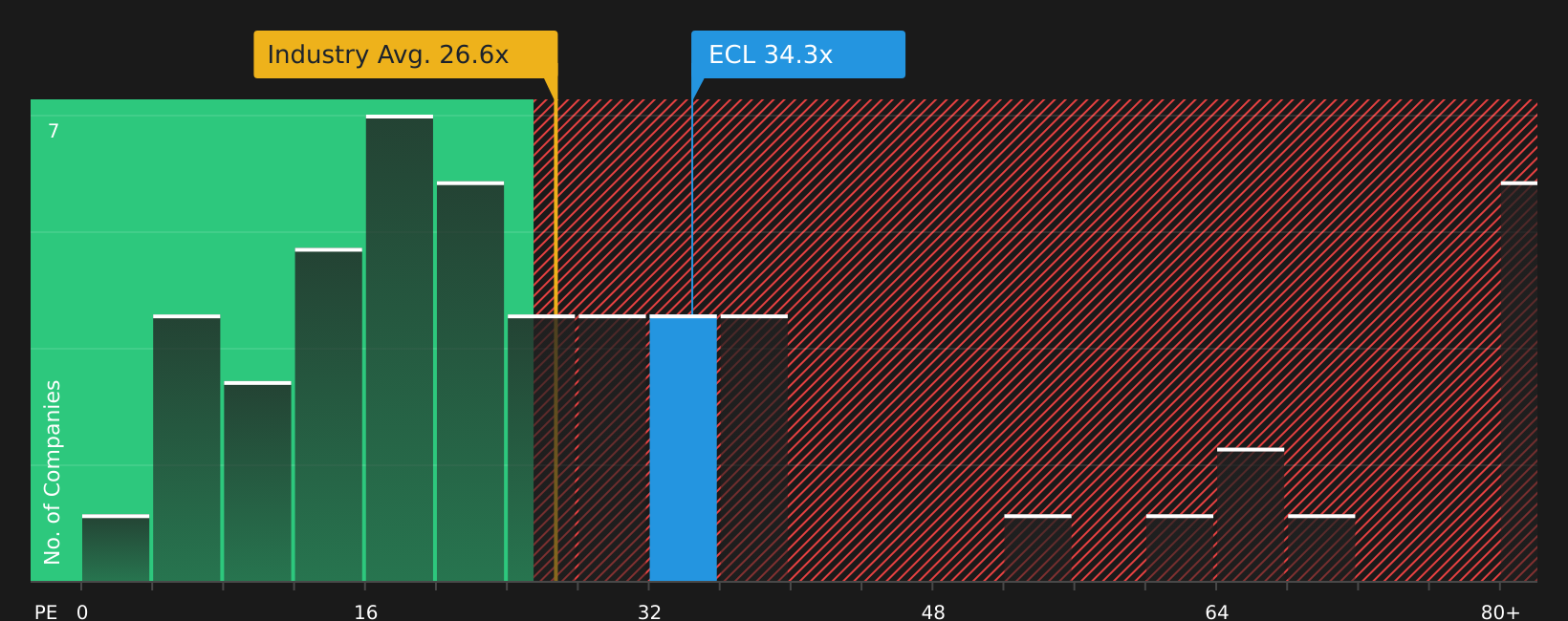

The popular fair value narrative leans on future earnings and a premium P/E, but the current numbers tell a tougher story. Ecolab trades on a P/E of 34.5x versus a fair ratio of 24.5x, and above both the peer average of 21.9x and the US Chemicals industry at 27.1x.

That kind of gap usually signals valuation risk rather than an obvious bargain. The key question is whether you think earnings quality and returns on equity justify paying this much ahead of the sector.

Next Steps

Curious whether the optimism in this story really balances the concerns it raises? Act now by reviewing the underlying data and weighing the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you could miss out on other opportunities that match your goals, risk comfort and income needs across the market.

- Spot potential bargain opportunities by comparing fundamentals and valuations across 48 high quality undervalued stocks that might fit your return expectations and risk profile.

- Lock in potential income ideas by scanning 10 dividend fortresses that combine yield with business strength and balance sheet support.

- Prioritize resilience by reviewing 63 resilient stocks with low risk scores that score well on financial health and business stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.