Assessing Iridium Communications (IRDM) Valuation After A Powerful Short Term Share Price Rally

Iridium Communications Inc. IRDM | 0.00 |

Stock performance snapshot

Iridium Communications (IRDM) has caught investor attention after a very large past 3 months return, while the stock is up 21% over the past month and 7% over the past week.

The recent 6.87% 1-day share price return at a last close of US$48.84 comes on top of strong short term momentum, with a 30-day share price return of 20.89% and a 1-year total shareholder return of 99.03%, even though the 3-year total shareholder return declined 14.11%. This suggests sentiment around Iridium Communications has shifted more positively in the near term.

If this kind of move has your attention, it could be a good moment to look at other satellite and communications plays by checking out 46 AI infrastructure stocks

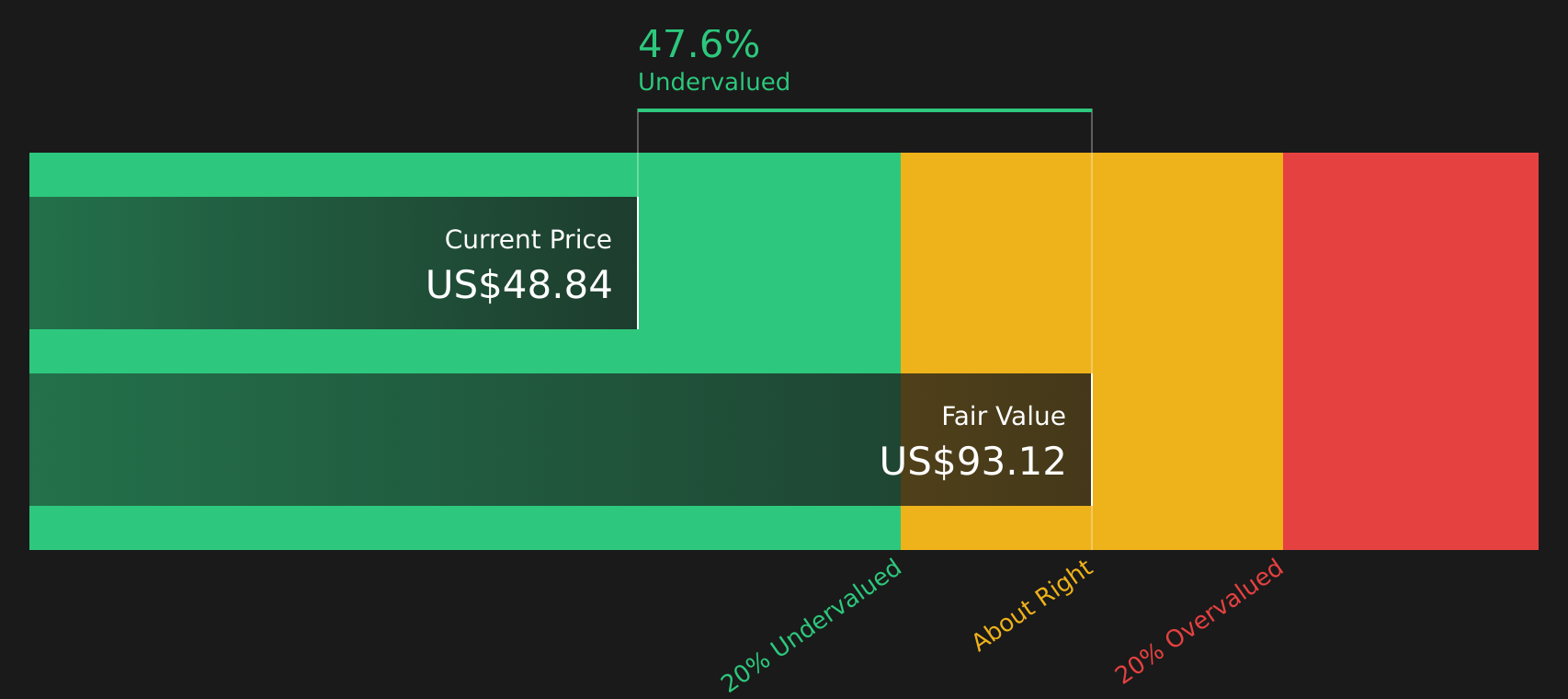

With Iridium trading at US$48.84 against an analyst price target of US$36.38 and an estimated intrinsic value suggesting a 48% discount, investors may question whether the stock is still undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 26.5% Overvalued

According to the most followed narrative, Iridium Communications has a fair value estimate of $38.60, which sits below the last close of $48.84 and frames the recent rally in a different light.

Iridium Communications (IRDM) represents a compelling long-term investment opportunity driven by its strategic positioning in the satellite communications industry and its recent acquisition of Satelles. This acquisition enables Iridium to leverage its existing infrastructure to capitalize on the growing demand for secure positioning, navigation, and timing systems (PNTS) as alternatives to aging GPS technology.

Want to see what kind of revenue mix and margin profile could support that valuation gap according to latentbiologist? The narrative leans heavily on PNTS growth, capital efficiency and how management might allocate cash through to 2030. The fair value hinges on those moving parts lining up just right.

Result: Fair Value of $38.60 (OVERVALUED)

However, this hinges on Satelles integration and PNTS adoption going smoothly. Any slowdown in government or defense demand could quickly challenge that optimistic setup.

Another view on value

While the most followed narrative points to Iridium Communications being 26.5% overvalued at $48.84 versus a $38.60 fair value, the SWS DCF model points the other way, with a fair value estimate of $94.32 suggesting the stock trades at a 48.2% discount. When two methods disagree this much, which one should carry more weight for you as an investor?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Iridium Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and sentiment so far? If you want to move quickly and build your own view, start by weighing both the upside and downside using 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Iridium has sharpened your interest, do not stop here. The next step is lining up fresh stock ideas that fit your style before the crowd catches on.

- Target potential mispricings by checking companies that screen well on quality and value using the 49 high quality undervalued stocks.

- Prioritize income and resilience by reviewing stocks with meaningful yields and robust fundamentals through the 10 dividend fortresses.

- Focus on financial strength first by scanning companies with clean balance sheets and solid metrics via the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.