Assessing Nucor (NUE) Valuation After Analyst Upgrades And Leadership Transition

Nucor NUE | 0.00 |

Analyst optimism and leadership transition put Nucor (NUE) in focus

Recent analyst upgrades tied to Nucor’s (NUE) earnings outlook, along with active capital projects and a planned leadership transition, have drawn fresh attention to the stock and its long term profitability efforts.

Nucor’s share price has pulled back 3% over the past day to US$254.39, but that comes after a strong run, with a 49.26% 3 month share price return and a 110.76% 1 year total shareholder return. This suggests momentum has been building as investors reassess its earnings potential and risk profile.

If you are looking for other ways to put recent industrial and infrastructure themes to work in your portfolio, consider scanning for 34 power grid technology and infrastructure stocks as a starting point.

With Nucor trading just above its average analyst price target but carrying a sizable intrinsic discount estimate, the key question is whether the pullback sets up a mispriced value opportunity or if the market already reflects future growth.

Most Popular Narrative: 4.2% Overvalued

The most followed narrative pegs Nucor’s fair value at $244.14 using an 8.85% discount rate, which sits slightly below the last close at $254.39.

Nucor's significant capital reinvestment of $860 million, with two-thirds directed towards projects commencing operations within two years, is expected to diversify and strengthen future earnings. This impacts revenue and net margins through enhanced production capacity and efficiencies.

Curious what kind of earnings power those new mills need to deliver to back this fair value? The narrative leans on measured revenue growth, firmer margins, and a lower future earnings multiple than many investors might expect.

Result: Fair Value of $244.14 (OVERVALUED)

However, this depends on steel demand remaining strong, as well as large projects like the West Virginia sheet mill and new micro mills proceeding without delays or cost overruns.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Paint A Different Picture

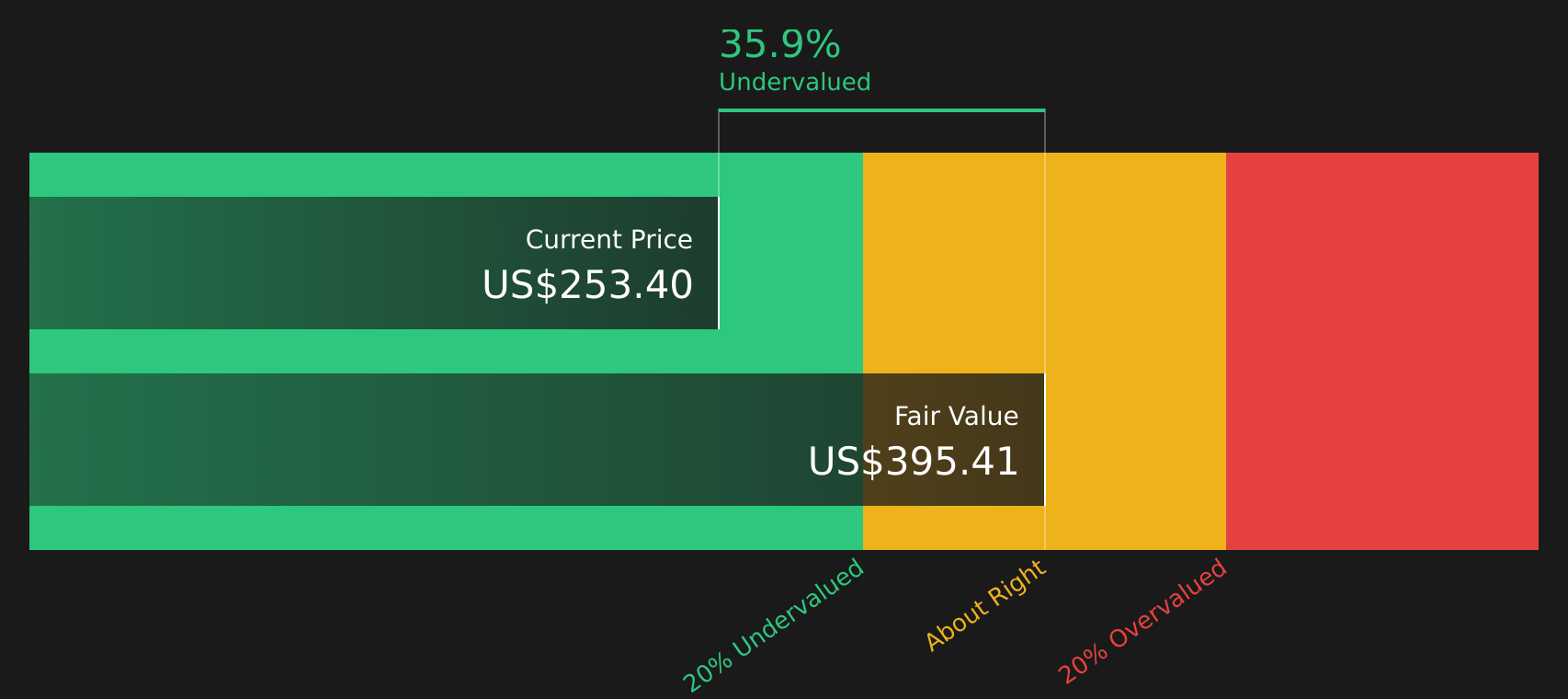

The narrative fair value of $244.14 suggests Nucor is about 4.2% overvalued, yet the SWS DCF model points in the opposite direction, with an estimated future cash flow value of $395.10 implying the stock trades at a 35.6% discount. Which signal do you trust more, the earnings multiple or the cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nucor for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and future earnings can be hard to weigh, so move quickly, review the underlying data, and test the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you could miss out on other opportunities that fit your style, so take a few minutes to scan these ideas.

- Spot potential value opportunities early by running your filters through 48 high quality undervalued stocks, which already combine quality with pricing signals.

- Build a steadier income stream by reviewing 10 dividend fortresses, which focus on higher yielding companies with resilient payout profiles.

- Sleep easier at night by screening for 63 resilient stocks with low risk scores, which keep overall risk scores in check while still leaving room for upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.