Assessing Robert Half (RHI) Valuation After Sector Rally And Protiviti AI Patent News

Robert Half RHI | 0.00 |

Robert Half (RHI) has drawn fresh attention after its stock climbed alongside a wider rally in staffing and employment services peers, while subsidiary Protiviti secured a second U.S. patent for AI driven automation technology.

That sector-wide rally and Protiviti’s new AI patent come after a sharp 34.68% 90 day share price return to US$31.26, yet the 1 year total shareholder return is still down 23.54%, so recent momentum contrasts with a weaker longer term record.

If you are looking beyond staffing and consulting, this could be a good moment to widen your watchlist with a curated set of 20 top founder-led companies

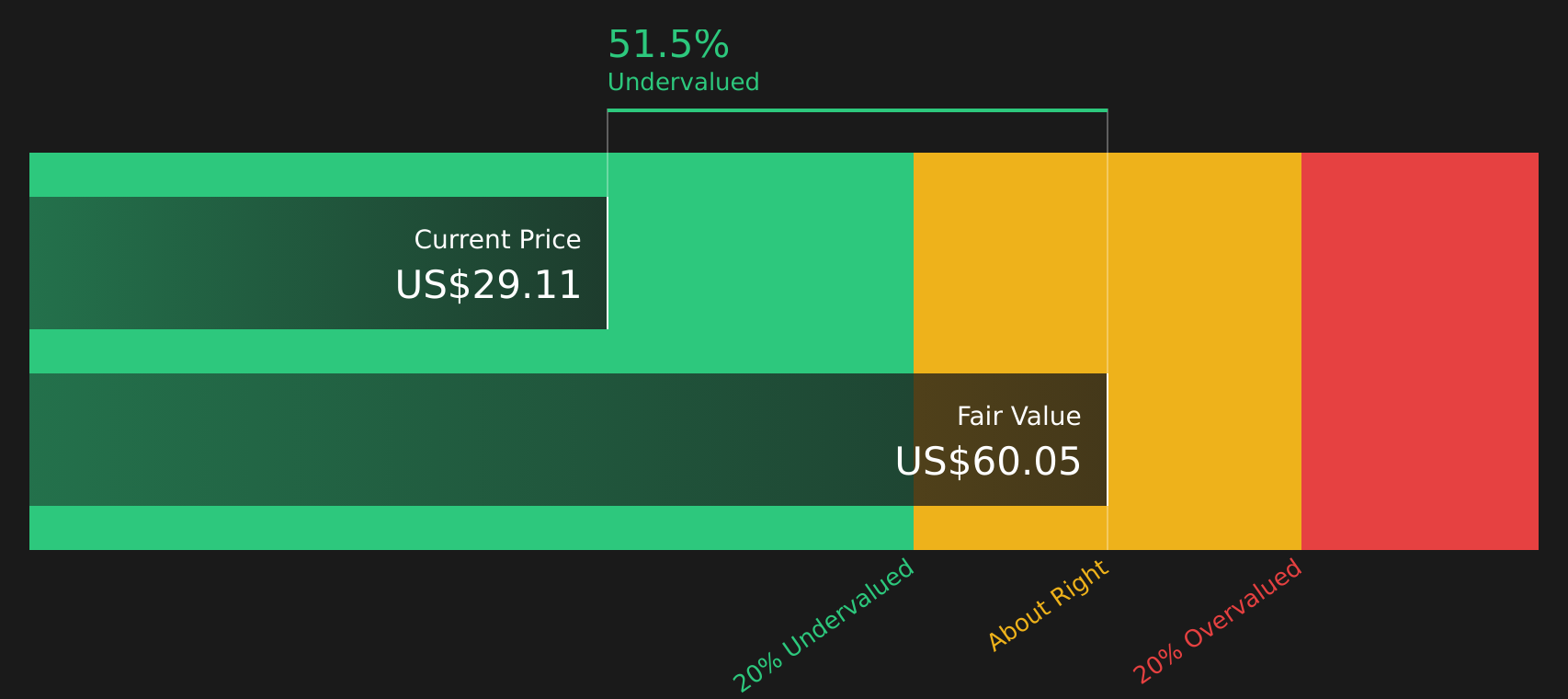

So with Robert Half trading at US$31.26 against an internal intrinsic value estimate that implies a wide discount, yet sitting slightly above the analyst price target, are you looking at a genuine mispricing or a market that has already priced in expectations of future growth?

Most Popular Narrative: 4% Undervalued

Robert Half's most followed valuation narrative pegs fair value at $32.39, only slightly above the current $31.26 share price. This leaves a relatively narrow implied upside and puts more weight on the earnings and margin assumptions behind that figure.

Recent research on Robert Half shows a split view, with some analysts lifting targets and others pulling back after the company disclosed a US$17 million cost action charge in its latest 10-K. Here is how the debate is shaping up for you as an investor watching execution and valuation risk.

Want to see what sits underneath that fair value gap? The core narrative leans on modest revenue acceleration, firmer margins and a tempered future earnings multiple. Curious which assumptions really carry the model?

Result: Fair Value of $32.39 (UNDERVALUED)

However, the narrative still hinges on reversing recent revenue declines and easing cost pressure. If those trends persist, profit and valuation assumptions could quickly look stretched.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Market Multiple Sends A Different Signal

While the SWS DCF model points to Robert Half at US$31.26 as trading well below an estimated fair value of US$60.09, the P/E picture is less forgiving. The current 24.3x P/E sits above the US Professional Services industry at 19.7x and above peers at 16.2x, even though it is below the 27.2x fair ratio the model suggests the market could move toward.

In practice, that means anyone leaning on the DCF is effectively betting that earnings delivery justifies both the discount to cash flow and a richer P/E than the sector. So which signal feels more credible to you right now?

Next Steps

With mixed signals on value, momentum and the business outlook, this is a moment to move quickly on your own homework and weigh both sides carefully. Start by reviewing the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Robert Half is on your radar, do not stop there. Spread your research across other angles so you are not relying on a single stock story.

The Simply Wall St screener makes it easy to move from one compelling idea to another in minutes, giving you a broader field of potential opportunities.

- Target higher quality at better prices by scanning a curated mix of 48 high quality undervalued stocks that pair stronger fundamentals with attractive entry points.

- Prioritise resilience by reviewing 63 resilient stocks with low risk scores that score well on stability, financial strength and lower historical volatility.

- Hunt for future leaders early with a focused list built from the screener containing 21 high quality undiscovered gems, before the wider market starts paying closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.