Please use a PC Browser to access Register-Tadawul

Get It

Does Analyst Optimism on Brookfield Renewable (BEPC) Reveal Deeper Strengths in Its Growth Strategy?

BROOKFIELD RENEWABLE CORP BEPC | 39.71 | -0.87% |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To believe in Brookfield Renewable as a shareholder means trusting in accelerating global demand for clean energy and the company’s capacity to grow through new projects, partnerships, and operational expansion. The recent reiteration of analyst confidence, despite a profit miss, supports the view that management’s focus on Funds From Operations growth could be a stronger near-term catalyst than earnings volatility. Risks around regulatory uncertainty in U.S. policy remain but are not materially changed by this quarter's news.

Among recent announcements, Brookfield Renewable’s long-term agreement with Microsoft, aimed at delivering 10.5 gigawatts of new capacity, stands out as especially relevant given rising analyst emphasis on project pipeline growth. This agreement provides visibility on future revenue streams and aligns with broader industry trends toward large corporate clean energy procurement, reinforcing the company’s role in meeting high-value demand.

Yet, in contrast, regulatory changes affecting renewable project permitting could stall growth plans, something investors should understand before...

Brookfield Renewable is projected to reach $7.0 billion in revenue and $761.5 million in earnings by 2028. This outlook is based on an assumed annual revenue growth rate of 21.8% and a $2.1 billion increase in earnings from the current level of -$1.3 billion.

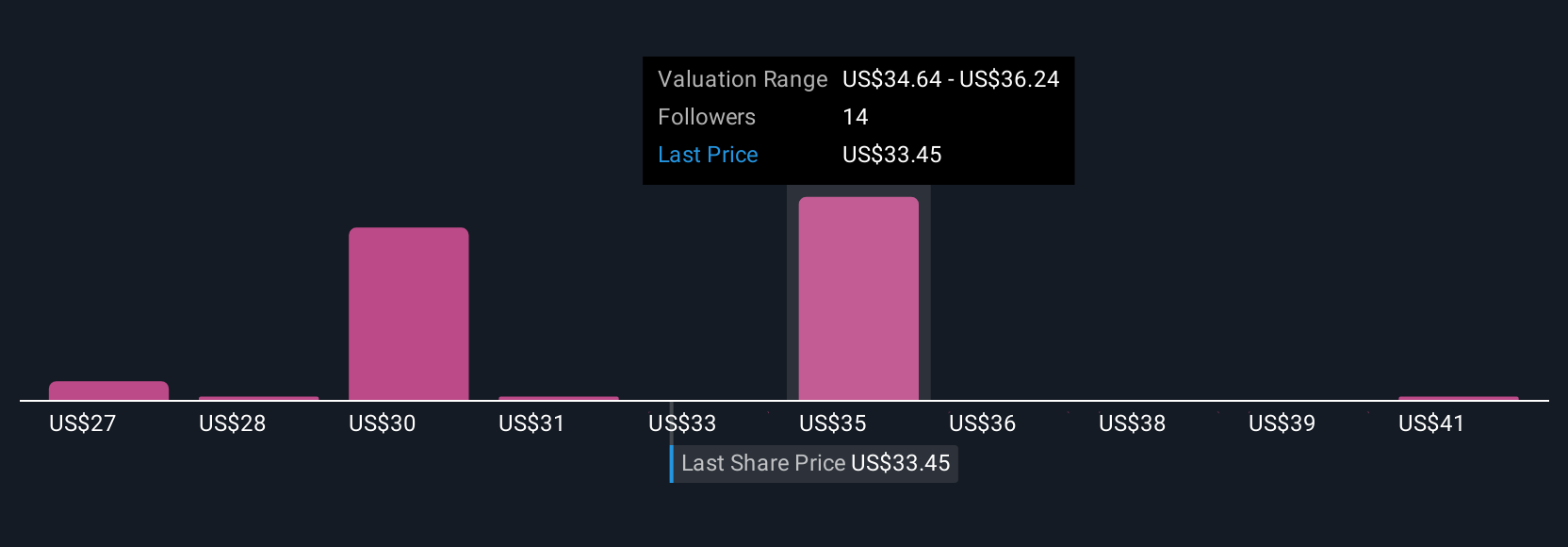

Uncover how Brookfield Renewable's forecasts yield a $36.20 fair value, a 5% downside to its current price.

Eight fair value estimates from the Simply Wall St Community range from US$26.64 to US$42.64 per share, highlighting wide differences in outlooks. With the company’s growth plans relying on large-scale projects and partnerships, consider how regulatory uncertainty could sway both sentiment and results, explore further viewpoints here.

Explore 8 other fair value estimates on Brookfield Renewable - why the stock might be worth as much as 12% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Opportunities like this don't last. These are today's most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.