Has The Market Gone Too Far On Viasat (VSAT) After Its 320% One-Year Surge?

ViaSat, Inc. VSAT | 0.00 |

- Wondering whether Viasat at around US$43.72 is still offering value or if most of the opportunity is already priced in? This article breaks down what the current share price might be implying.

- The stock has returned 16.2% year to date and 319.6% over the past year, even though the last 7 days and 30 days show declines of 11.1% and 4.5% respectively.

- Recent headlines have focused on Viasat's position in satellite communications and its role in providing connectivity services, which has kept attention on the stock. This backdrop helps explain why the market has been reassessing both its growth potential and its risks over the past year.

- Viasat currently has a valuation score of 5 out of 6. Next you will see how different valuation methods stack up for the company, and later on you will see an approach that can help you put all of those signals into a clearer story.

Approach 1: Viasat Discounted Cash Flow (DCF) Analysis

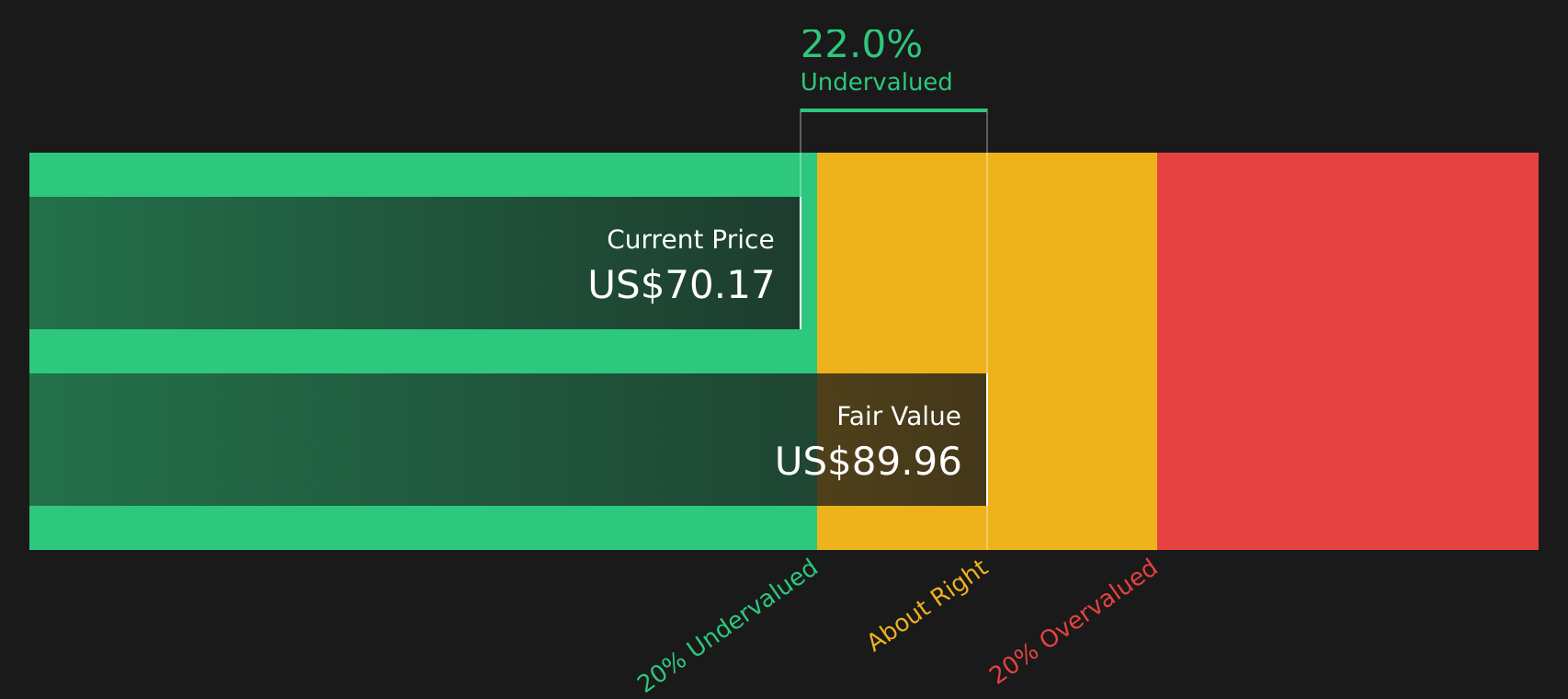

The DCF model estimates what a business could be worth by projecting its future cash flows and then discounting those back to today, so you can compare that value with the current share price.

For Viasat, the model uses a 2 Stage Free Cash Flow to Equity approach based on projected free cash flow in $. The latest twelve month free cash flow is about $289.7 million, and analyst and extrapolated estimates point to free cash flow of $555.2 million in 2028. Simply Wall St then extends those projections out to 2035, discounting each year’s cash flow back to today and adding them together.

On this basis, the estimated intrinsic value for Viasat comes out at about $71.30 per share. Compared with the current share price of about $43.72, the DCF suggests the stock is roughly 38.7% undervalued according to these cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Viasat is undervalued by 38.7%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: Viasat Price vs Sales

For companies where earnings can be volatile or influenced by heavy investment, the P/S ratio is often a useful way to compare what the market is paying for each dollar of revenue. It avoids the noise that can come from short term swings in profit, while still tying valuation back to the core business.

Growth expectations and risk still matter here. Higher growth and lower perceived risk can support a higher P/S multiple, while slower growth or higher uncertainty usually calls for a lower, more conservative multiple.

Viasat currently trades on a P/S ratio of about 1.29x. That sits below the Communications industry average of 2.38x and the peer group average of 7.07x. Simply Wall St’s Fair Ratio for Viasat is 2.02x, which is its proprietary estimate of what the P/S multiple could be given factors such as revenue growth, profit margins, industry, market cap and key risks.

This Fair Ratio is more tailored than a simple comparison with peers or the broad industry, because it adjusts for Viasat’s own profile rather than assuming all companies deserve the same multiple. With the current 1.29x P/S ratio sitting below the 2.02x Fair Ratio, this approach suggests that the shares may be undervalued on a sales basis.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Viasat Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you turn your view of Viasat into a clear story that joins the business setup, a financial forecast and a Fair Value, then compares that Fair Value to today’s price to help you decide whether the stock looks expensive or cheap for your plan.

On the Community page, you can pick or create a Narrative by choosing assumptions for future revenue, earnings and margins. The platform turns these into cash flow and valuation estimates that update automatically when new earnings, news or guidance is added.

For Viasat, one investor might lean toward a higher Fair Value near US$58.00 if they agree with the more optimistic view that assumes stronger earnings and a higher P/E of about 20.6x in 2029. Another might align with a lower Fair Value around US$26.66 if they think a more cautious path with a future P/E of about 10.48x is more realistic. Seeing those Narratives side by side can make it easier to decide which story best matches personal expectations and risk tolerance.

For Viasat however, we will make it really easy for you with previews of two leading Viasat Narratives:

Fair Value in this bullish narrative: US$58.00 per share

Implied discount to this Fair Value at US$43.72: about 24.6% undervalued

Assumed revenue growth: 6.93% a year

- Backers of this view are leaning on higher capacity from ViaSat 3, shared infrastructure and open networks to support a larger addressable market and stronger free cash flow over time.

- The story assumes Viasat gradually lifts profit margins closer to the wider US Communications industry, which in the model would support higher earnings and a P/E of about 20.6x by 2029.

- It also acknowledges meaningful risks, including heavy capital needs, competition from low Earth orbit players, integration work after the Inmarsat deal and the chance that a defense spinout or other portfolio moves may not play out as expected.

Fair Value in this more cautious narrative: US$41.13 per share

Implied premium to this Fair Value at US$43.72: about 6.3% overvalued

Assumed revenue growth: 4.14% a year

- This view accepts that secure connectivity and the ViaSat 3 rollout can support growth, but places more weight on execution challenges, capital intensity and competition from larger satellite operators.

- Analysts behind this framework are using a lower Fair Value and higher discount rate, with revenue growing more slowly and profit margins settling below the bullish case, even though a higher future P/E multiple of about 19.7x is applied.

- Key concerns include high ongoing CapEx, pressure on US fixed broadband subscribers, legal and regulatory costs and the risk that any defense spinout or portfolio reshaping does not deliver the uplift some investors expect.

Do you think there's more to the story for Viasat? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.