How a Potential 500-Megawatt Customer Load Could Reshape Avista’s (AVA) Long-Term Investment Story

Avista AVA | 0.00 |

- In June 2026, Avista Corporation reported that it had entered into a non-binding memorandum of understanding with a developer in its Washington service territory to explore supplying an initial 125-megawatt electric load from 2029, potentially rising to 500 megawatts by 2032, subject to regulatory approvals and definitive agreements.

- This prospective large-load customer could reshape Avista’s long-term planning by driving new generation procurement, grid upgrades, and a structure aimed at delivering net benefits to existing customers while supporting regional economic development.

- We’ll now look at how this potential 500-megawatt large-load agreement could influence Avista’s investment narrative and long-term growth drivers.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Avista Investment Narrative Recap

To own Avista, you generally need to believe in the appeal of a regulated utility focused on steady earnings, a reliable dividend and constructive regulatory relationships. The new 125 to 500 megawatt large-load MOU could strengthen the long term growth story if it progresses, but in the near term the main catalyst remains regulatory outcomes on cost recovery, while the biggest risk is rising capital needs outpacing what regulators allow into rates.

This prospective customer links directly to Avista’s January 2026 resource update, where the company identified new gas peaking capacity, a 100 megawatt battery project and a roughly 200 megawatt wind PPA as preferred options. Together, those plans and the MOU highlight how emerging large-load requests could feed into future rate base growth, but they also underline the execution and regulatory risks around expanding the grid and adding generation to meet potential demand.

Yet behind the appeal of a growing regulated rate base, investors should also be aware of the risk that rising capital expenditure for grid upgrades, new generation and wildfire mitigation could...

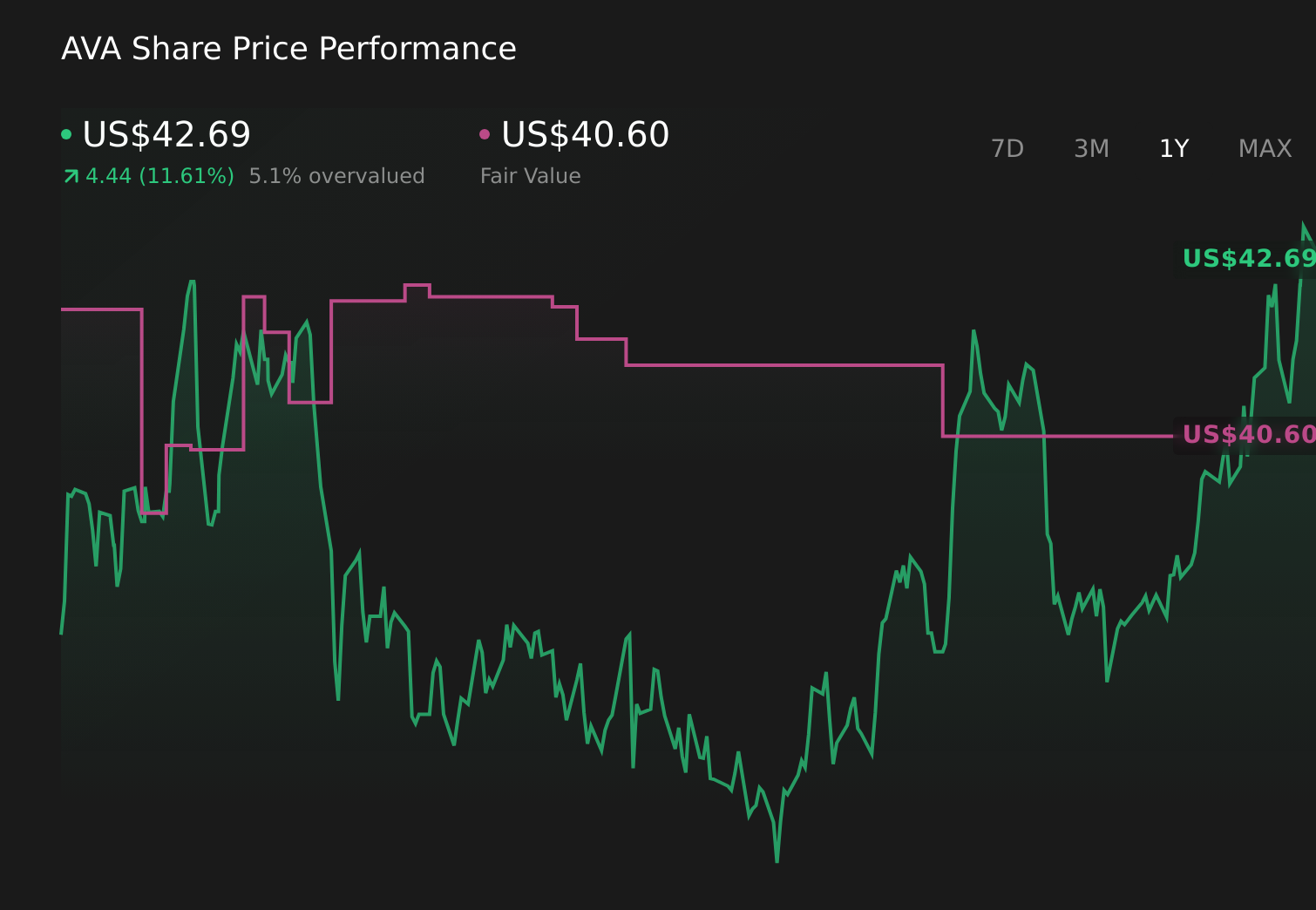

Avista’s narrative projects $2.2 billion revenue and $253.4 million earnings by 2029. This requires 3.3% yearly revenue growth and about a $60 million earnings increase from $193.0 million today.

Uncover how Avista's forecasts yield a $42.80 fair value, in line with its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$35.94 to US$42.80 per share, showing how differently individual investors see Avista’s prospects. When you weigh those views against the potential 500 megawatt large-load opportunity and the capital recovery risk it brings, it becomes even more important to examine several perspectives before forming an opinion.

Explore 2 other fair value estimates on Avista - why the stock might be worth 15% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Avista research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Avista research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avista's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.