Please use a PC Browser to access Register-Tadawul

Get It

How Slower EPS Growth Guidance at MongoDB (MDB) Has Changed Its Investment Story

MONGODB MDB | 409.62 | +3.25% |

Find companies with promising cash flow potential yet trading below their fair value.

To own MongoDB stock, an investor needs to believe that its AI and cloud initiatives will translate into sustained, high-quality growth, particularly through continued adoption of Atlas and product innovation. The latest Q2 results reinforce this narrative in the short term, but the company's updated guidance for slower EPS growth casts some doubt on the immediate benefit of AI gains. Right now, the most important catalyst remains enterprise adoption of Atlas, while the biggest risk centers on intensifying competition from cloud-native database providers; neither appears materially changed by the recent guidance, though margin pressure remains a concern. Among several recent company developments, the announcement of MongoDB AMP, an AI-powered Application Modernization Platform, stands out as especially relevant. This move directly highlights MongoDB’s commitment to helping enterprises leverage AI for legacy transformation, linking clearly with both current customer demand and AI-driven revenue momentum. These product rollouts align closely with the growth catalysts investors are watching. Yet, despite AI momentum and breakthroughs, investors should also be aware that competitive risks are ...

MongoDB's outlook suggests $3.5 billion in revenue and $5.0 million in earnings by 2028. This is based on a projected 16.8% annual revenue growth rate and reflects an increase in earnings of $83.6 million from the current level of -$78.6 million.

Uncover how MongoDB's forecasts yield a $350.80 fair value, a 12% upside to its current price.

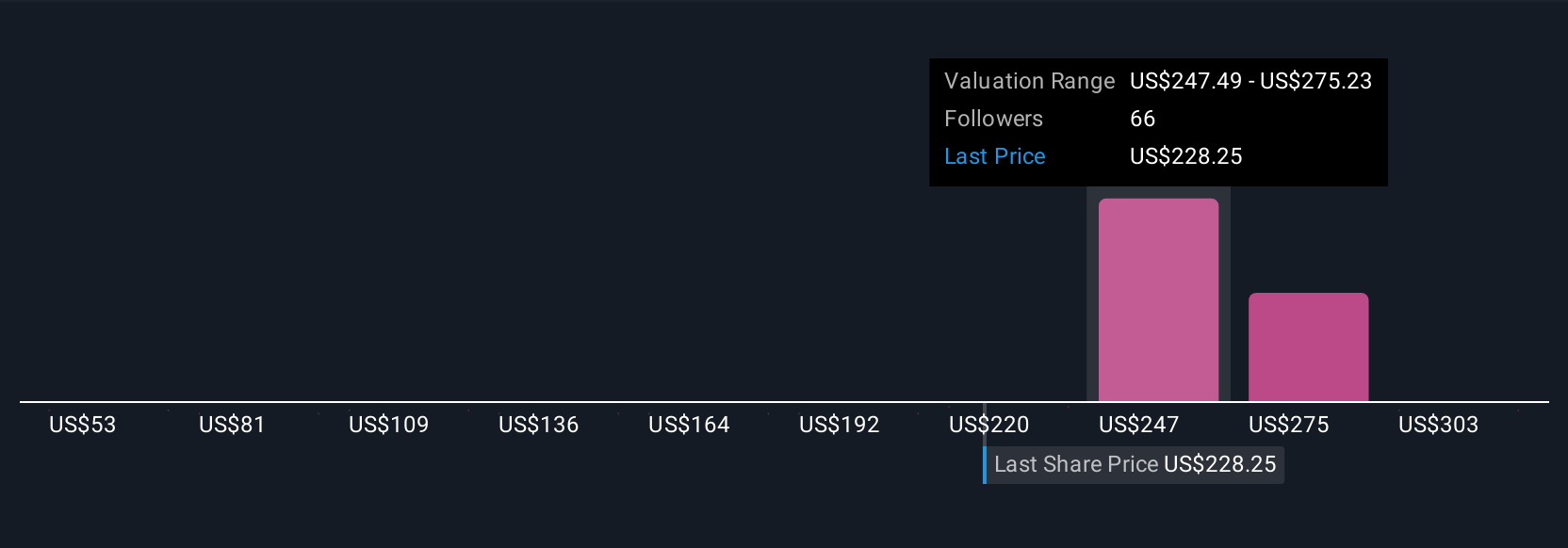

Eleven members of the Simply Wall St Community estimate fair value for MongoDB between US$130.20 and US$394.78 per share. While these views span both bullish and cautious expectations, many are watching carefully as competition from cloud-native database providers could impact MongoDB’s margins and scale.

Explore 11 other fair value estimates on MongoDB - why the stock might be worth as much as 26% more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.