Ingersoll Rand (IR) Valuation Check After Garrett Motion Partnership On Oil Free Air Technologies

Ingersoll Rand Inc. IR | 0.00 |

Ingersoll Rand (IR) has entered a multiyear partnership with Garrett Motion to develop next generation oil-free air technologies aimed at greater energy efficiency, reliability, and air purity across critical industrial markets.

Despite the new partnership announcement, Ingersoll Rand’s recent trading has been weak, with the share price down 25.8% over the past 90 days and the 1 year total shareholder return declining 11.7%. Recent momentum has clearly cooled compared with its longer term 3 year total shareholder return of 20.8%.

If this kind of industrial technology story interests you, it may also be worth scanning for other opportunities in power and automation through our 35 power grid technology and infrastructure stocks

With the stock down sharply in recent months, yet trading below one approach to intrinsic value and some analyst targets, you have to ask yourself: is Ingersoll Rand now on sale, or is the market already pricing in its future growth?

Most Popular Narrative: 24.6% Undervalued

The most followed narrative currently places Ingersoll Rand’s fair value at $94, above the last close of $70.91, which frames the recent share price slide in a very different light.

The company continues building recurring, high-margin revenue streams through expansion of aftermarket services and value-added lifecycle solutions (aftermarket revenue grew to 37% of total), which increases the stability of net margins and supports long-term earnings resilience even if new equipment demand remains variable.

Want to understand why this narrative supports a higher valuation despite recent share price weakness? The core assumptions tie together recurring revenue, rising margins, and a richer future earnings multiple. Curious which combination of growth, profitability, and discount rate gets to that $94 figure? The full narrative presents the numbers behind that conclusion.

Result: Fair Value of $94 (UNDERVALUED)

However, you also need to weigh the risk that acquisition missteps or weaker compressor and power tools demand could pressure margins and challenge those higher earnings assumptions.

Another Angle on Valuation

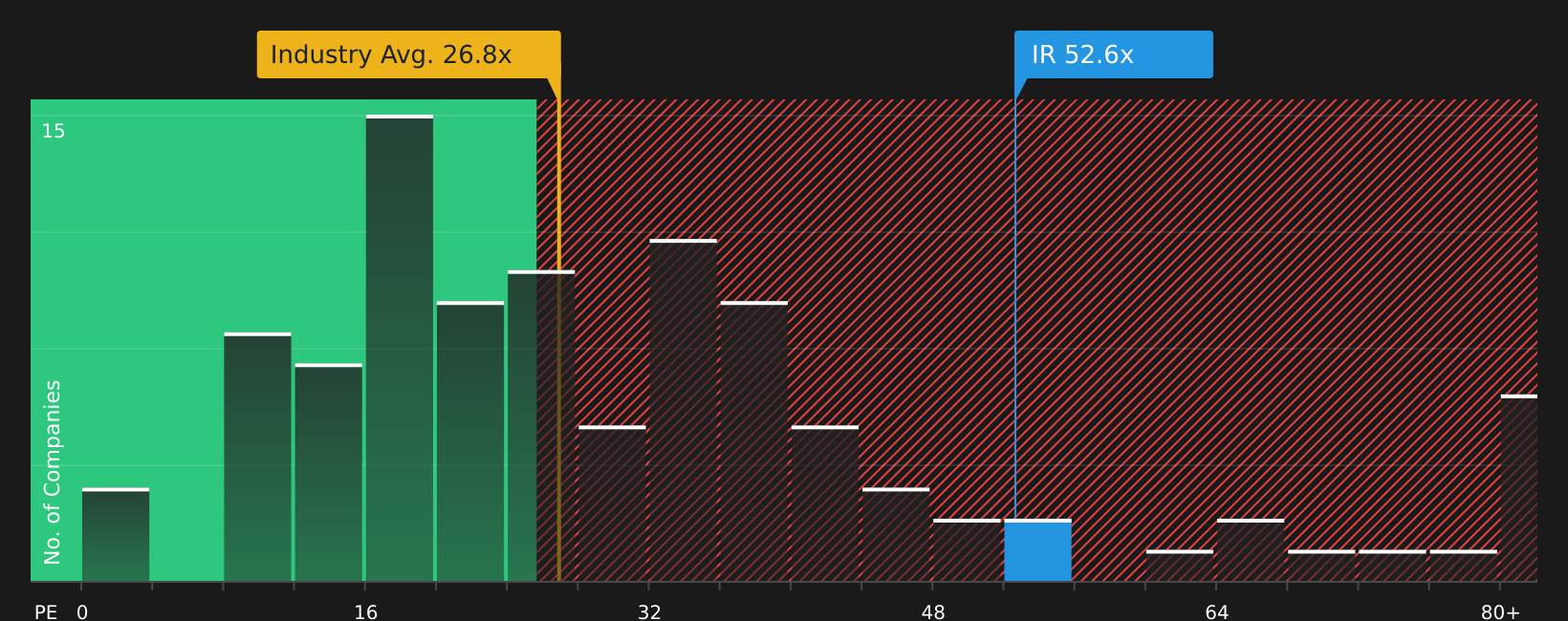

That 24.6% “undervalued” view is built on future earnings assumptions, but the current P/E of 47.3x tells a different story. It sits well above the Machinery industry at 26.4x, peers at 33.2x, and even the 37.5x fair ratio, which points to real valuation risk if sentiment cools.

To see how this high P/E compares with what the numbers suggest the ratio could move toward, and what that gap might mean for your risk tolerance, take a closer look at our valuation breakdown, starting with the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of concern and optimism running through this story, it makes sense to look at the full picture yourself and decide where you stand. You can start with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might fit your style even better, so give yourself options and compare.

- Target potential bargains by scanning companies that screen well on valuation and quality through the 49 high quality undervalued stocks.

- Prioritise resilience by checking out stocks that pass strict balance sheet and fundamentals checks via the solid balance sheet and fundamentals stocks screener (46 results).

- Spot early-stage standouts by reviewing a screener containing 21 high quality undiscovered gems before more attention arrives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.