Is It Time To Reassess Nvidia (NVDA) After The Recent AI Rally And Pullback

NVIDIA Corporation NVDA | 0.00 |

- If you are wondering whether NVIDIA's current share price offers good value or is already pricing in a lot of optimism, this article walks through what that might mean for you as an investor.

- After a very strong multi year run, the stock is still up 8.6% year to date and 44.0% over the last year, even though it has fallen 8.6% over the past week and 4.7% over the past month from a last close of US$205.10.

- Recent headlines around NVIDIA have focused on its central role in powering artificial intelligence workloads and data center build outs, alongside ongoing attention on regulation, competition and chip supply. These themes help explain why the stock can move sharply in short periods as expectations and risk appetite shift.

- NVIDIA currently has a valuation score of 3/6, which means it screens as undervalued on half of the checks used in this framework. The rest of this article will compare several valuation approaches before finishing with a broader way to think about what the stock might be worth.

Approach 1: NVIDIA Discounted Cash Flow (DCF) Analysis

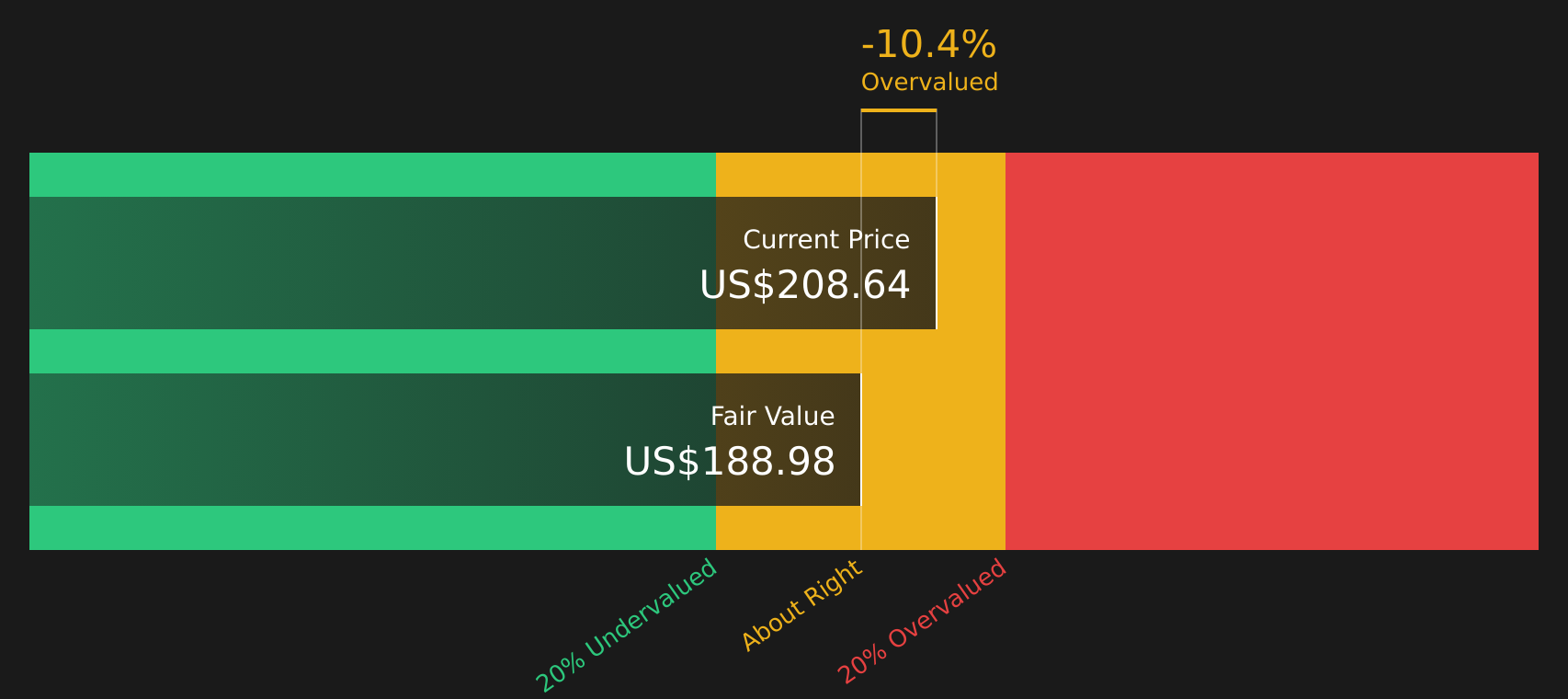

A Discounted Cash Flow model projects a company’s future cash flows and then discounts those back to today using a required rate of return, aiming to estimate what the business might be worth in total per share.

For NVIDIA, the model used here is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is around $119.4b. Analyst and extrapolated projections see free cash flow figures between $96.0b and $540.8b over the next decade, with one specific projection for 2031 at $434.9b. Simply Wall St only uses direct analyst inputs for the nearer years, and then extends the series using its own growth assumptions for later periods.

After discounting those projected cash flows back to today, the model produces an estimated intrinsic value of $188.98 per share. Compared with a recent share price of $205.10, this DCF output suggests the stock is around 8.5% above the model’s estimate of fair value. This represents a modest gap rather than an extreme one.

Result: ABOUT RIGHT

NVIDIA is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: NVIDIA Price vs Earnings

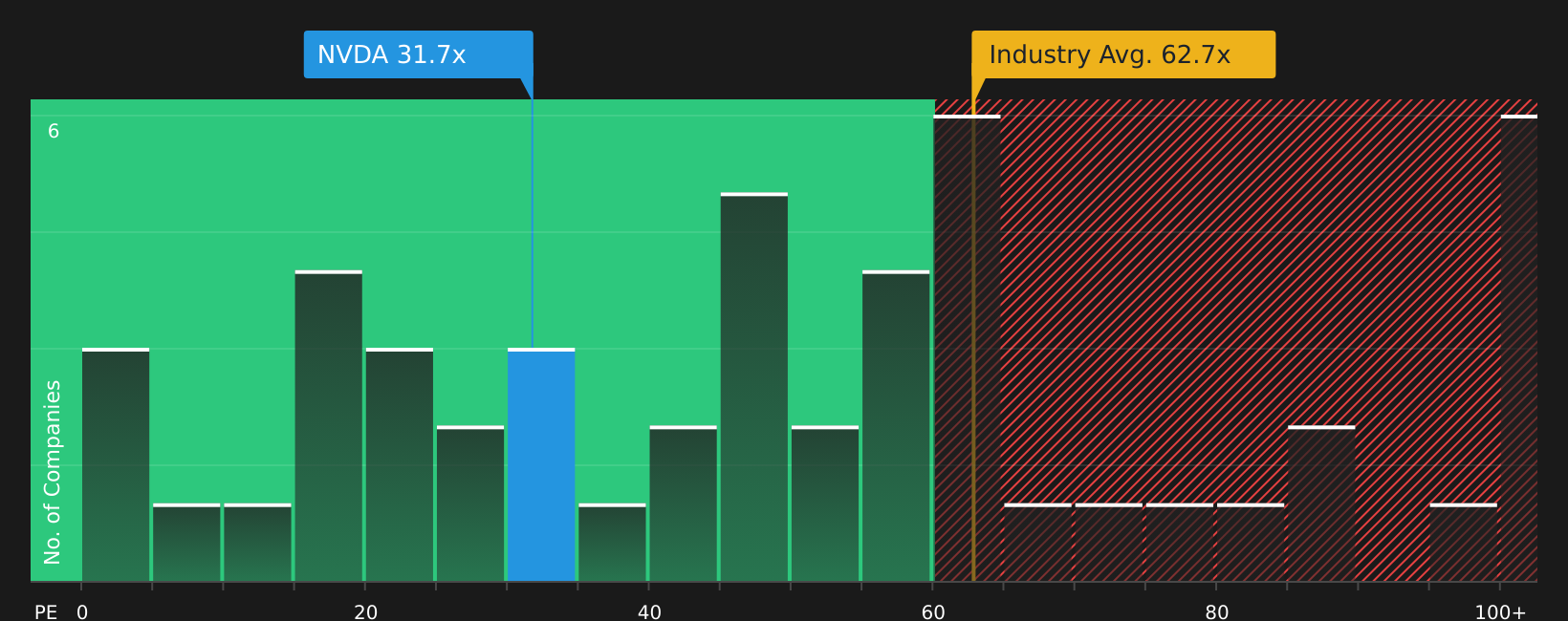

For profitable companies, the P/E ratio is often a useful shorthand because it links what you pay for the stock to the earnings the company is already generating. Higher growth potential and lower perceived risk usually justify a higher P/E, while slower growth or higher risk tend to pull a “normal” or “fair” P/E lower.

NVIDIA currently trades on a P/E of 31.1x. That sits well below the Semiconductor industry average of about 61.8x and also below the peer group average of 87.0x. On those simple comparisons, the stock looks cheaper than many other semiconductor stocks.

Simply Wall St’s “Fair Ratio” refines this by estimating what P/E might be appropriate once factors like earnings growth, profit margins, industry, market cap and risk profile are taken into account. For NVIDIA, this Fair Ratio is 63.5x, which is a proprietary view of what investors might reasonably pay based on those characteristics. Because it is tailored to the company rather than a broad group, it can be more informative than just lining NVIDIA up against peers or the industry average. With the current P/E of 31.1x sitting well below the Fair Ratio of 63.5x, the stock screens as undervalued on this metric.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your NVIDIA Narrative

Earlier it was mentioned that there is an even better way to understand valuation. This is where Narratives come in, letting you attach a clear story to your numbers by pairing your view of NVIDIA’s future revenue, earnings and margins with an explicit fair value, then tracking how that stacks up against the current share price.

On Simply Wall St’s Community page, Narratives are an easy tool you can use to set out your own forecast for the company, link it to a valuation and then see, in one place, whether your fair value suggests the stock looks expensive or cheap compared with today’s US$205.10 price. This can help you decide whether it feels like a time to be patient or to act.

Narratives update automatically as new data arrives. When fresh earnings, regulatory news or AI contract announcements appear, the fair values behind each NVIDIA story are refreshed, and you can instantly see whether your thesis still holds or needs a rethink.

For example, one NVIDIA Narrative on the Community page currently anchors around a fair value of US$167, another around US$270 and a third closer to US$305. This shows how different investors, all looking at the same stock, can reasonably land in very different places depending on how confident they are about AI infrastructure demand, competition and long term margins.

For NVIDIA however we will make it really easy for you with previews of two leading NVIDIA Narratives:

Fair value in this narrative: US$339.90 per share

At the recent price of US$205.10, this narrative views the stock as trading about 40% below its fair value estimate.

Implied long term revenue growth assumption: 30%

- Sees NVIDIA reaching US$400b in annual revenue in five years, with around 90% tied to data center customers and AI racks like Blackwell driving that outcome.

- Highlights execution risks around competition, potential disruption to the CUDA software stack and the need for NVIDIA and its partners to keep pushing new chip generations that justify large replacement cycles.

- Stresses how energy, regulation and geopolitics around AI, semiconductors and power supply could slow data center expansion or limit access to key markets, which would pressure this high growth path.

Fair value in this narrative: US$104.00 per share

At the recent price of US$205.10, this narrative views the stock as trading about 97% above its fair value estimate.

Implied long term revenue growth assumption: 13%

- Accepts that NVIDIA earned “legendary” status during the large language model boom, with CUDA and its GPUs becoming the default choice for AI training workloads.

- Argues that the initial surge in GPU demand was pulled forward, so training demand could cool while inference work shifts toward custom chips and other processors that reduce NVIDIA’s share.

- Frames current expectations as very high. The narrative suggests a trading range between US$70 and US$140 as more consistent with a strong but maturing hardware and AI infrastructure provider.

Do you think there's more to the story for NVIDIA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.