Is Vulcan’s CEO Transition and Reaffirmed 2026 EBITDA Outlook Reshaping the Case for VMC?

Vulcan Materials Company VMC | 0.00 |

- On May 11, 2026, Vulcan Materials Company announced that President Thompson S. Baker II will retire from his role effective July 15, 2026, while also reaffirming its 2026 adjusted EBITDA outlook supported by a healthy project backlog and continued strength in public construction activity.

- This combination of leadership transition and reiterated earnings guidance highlights how Vulcan’s aggregates-heavy portfolio remains closely aligned with ongoing infrastructure demand and large public works projects.

- We’ll now examine how Vulcan’s reaffirmed 2026 adjusted EBITDA outlook, underpinned by a strong public-construction backlog, affects its investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you need to believe that sustained public infrastructure spending will keep its aggregates business humming, even while residential and weather-related headwinds linger. The latest news, combining the president’s planned retirement with reaffirmed 2026 adjusted EBITDA guidance, does not materially alter the near term catalyst, which still centers on the size and timing of publicly funded projects, or the key risk around potential interruptions or changes to government infrastructure funding.

Against that backdrop, Vulcan’s ongoing share repurchase activity, including the US$149.48 million buyback in Q1 2026, feels especially relevant. While the company is investing heavily in its aggregates footprint and efficiency, this capital return program amplifies the impact of any future earnings progress, but it also interacts with the risk of high capital needs and project delays if infrastructure momentum or permitting conditions were to soften.

Yet even with reaffirmed guidance, investors should be aware that heavy reliance on government-backed infrastructure funding could...

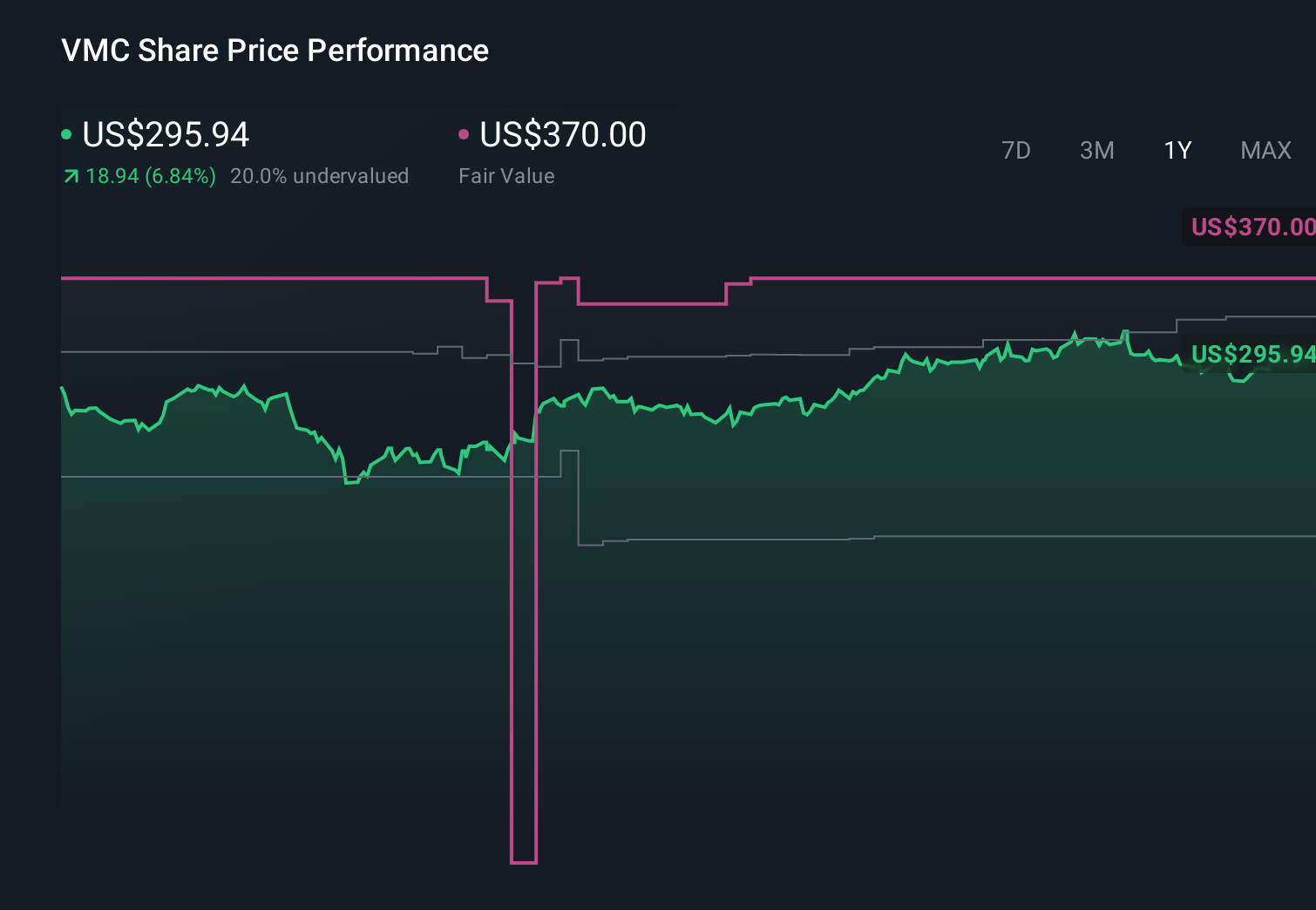

Vulcan Materials' narrative projects $9.6 billion revenue and $1.7 billion earnings by 2029. This requires 6.0% yearly revenue growth and roughly a $0.6 billion earnings increase from $1.1 billion today.

Uncover how Vulcan Materials' forecasts yield a $328.81 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were counting on revenue of about US$10.0 billion and earnings near US$1.9 billion by 2029, which is far more upbeat than the baseline view. When you compare that to concerns about stricter environmental rules potentially raising costs, it shows just how differently you can read the same company story, especially now that leadership and guidance reaffirmations may prompt both camps to revisit their assumptions.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth just $256.61!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.