Klarna Group (NYSE:KLAR) Valuation Check As Shares Rebound After A Weak Start To The Year

Klarna Group Plc KLAR | 0.00 |

Klarna Group stock: recent performance in focus

Klarna Group (KLAR) has drawn attention after a recent stretch of mixed returns, with the stock up over the past week and month, yet down about 42% so far this year.

The recent 1 month share price return of 11.96% and 3 month share price return of 26.68% contrast with the share price being down 42% year to date, suggesting momentum has picked up after a weak start to the year.

If Klarna’s rebound has caught your eye, it can be useful to compare it with other fast growing financial technology and payments players by scanning 20 top founder-led companies

With Klarna shares rebounding in recent months but still down sharply for the year, the key question now is whether the current price undervalues its growth potential or if the market is already pricing in future gains.

Most Popular Narrative: 61.5% Undervalued

Against the last close at $16.57, the most followed narrative on Klarna sets a fair value of $43.01, implying a large gap between market price and that narrative view.

Small, Purposeful Loans: Instead of the "revolving door" of high-interest credit card debt, Klarna offers surgical, small-scale loans.

Flexible Payment Plans: By breaking a $400 purchase into four $100 payments, Klarna allows consumers to manage cash flow without the "debt hangover" typical of 20% APR cards.

According to SiwyOgon, this fair value leans heavily on stronger revenue growth, sharply improving profitability and a richer future earnings multiple. Want to see which assumptions carry the most weight and how they connect to that $43.01 figure?

Result: Fair Value of $43.01 (UNDERVALUED)

However, this narrative could be challenged if Klarna struggles to move from losses to consistent profits or if regulators tighten rules on flexible payment products.

Another View: Cash Flows Paint A Different Picture

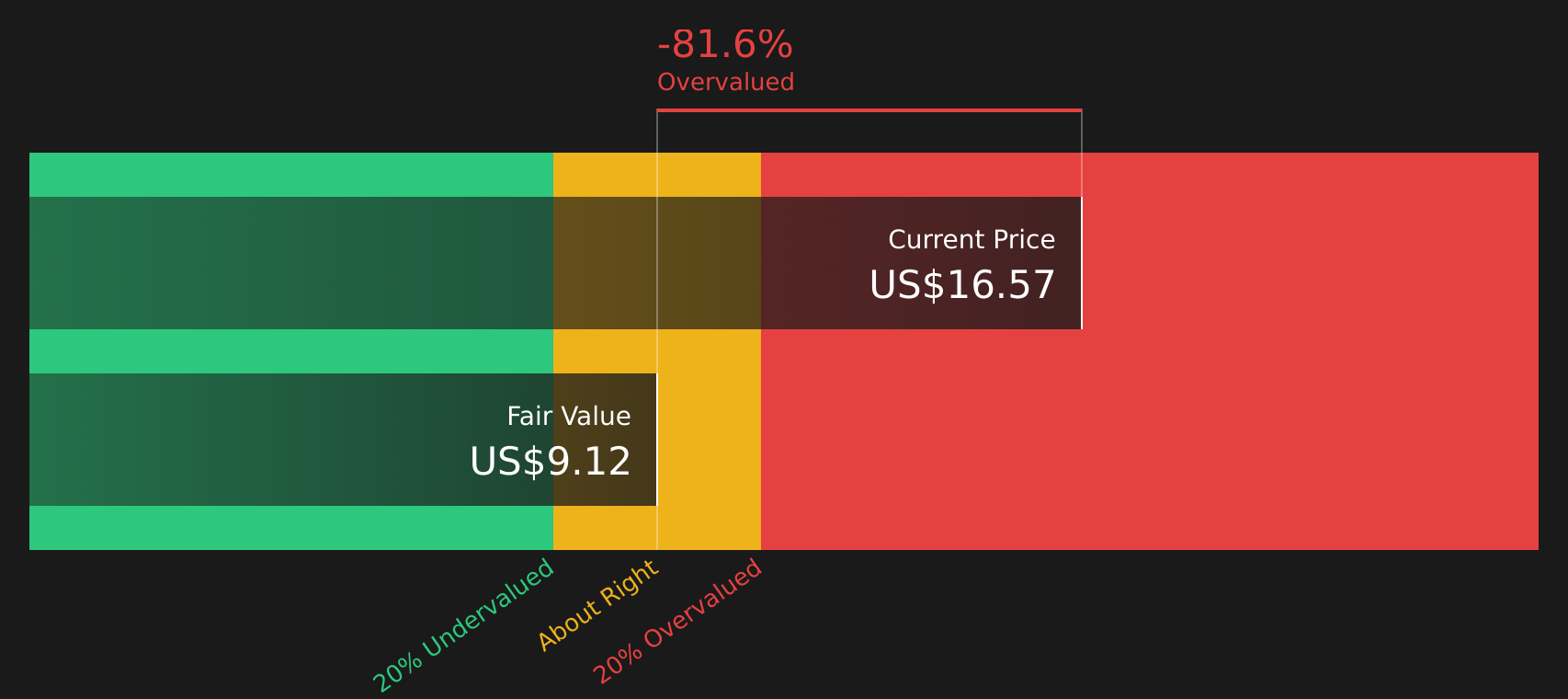

While the most popular narrative sees Klarna stock as undervalued at a fair value of $43.01, the SWS DCF model points in the opposite direction. At a share price of $16.57, the model estimates Klarna’s future cash flow value at $10.20, suggesting the stock is currently priced above that estimate.

For you as an investor, that split view can feel uncomfortable. One approach leans on growth, margins and future earnings multiples. The DCF framework, in contrast, focuses directly on projected cash generation and applies its own discount rate. When two lenses disagree this clearly, which assumptions earn your trust, and why?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between optimism and caution, this is a good moment to review the numbers for yourself and move quickly while views are still forming. A useful starting point is the 2 key rewards.

Looking for more investment ideas?

If Klarna has sharpened your focus, do not stop here. Use curated lists to quickly spot other opportunities that might fit your style and goals.

- Target dependable income by scanning companies we group as 10 dividend fortresses that offer higher yields with a focus on resilience.

- Hunt for potential mispriced opportunities through 49 high quality undervalued stocks that combine solid fundamentals with room for market sentiment to improve.

- Prioritise capital protection by reviewing 66 resilient stocks with low risk scores designed to highlight businesses with lower risk scores and steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.