Please use a PC Browser to access Register-Tadawul

Get It

Q.E.P (QEPC): Margin Expansion Challenges Skepticism, But Earnings Quality Draws Investor Scrutiny

Q.E.P. CO INC QEPC | 35.80 | 0.00% |

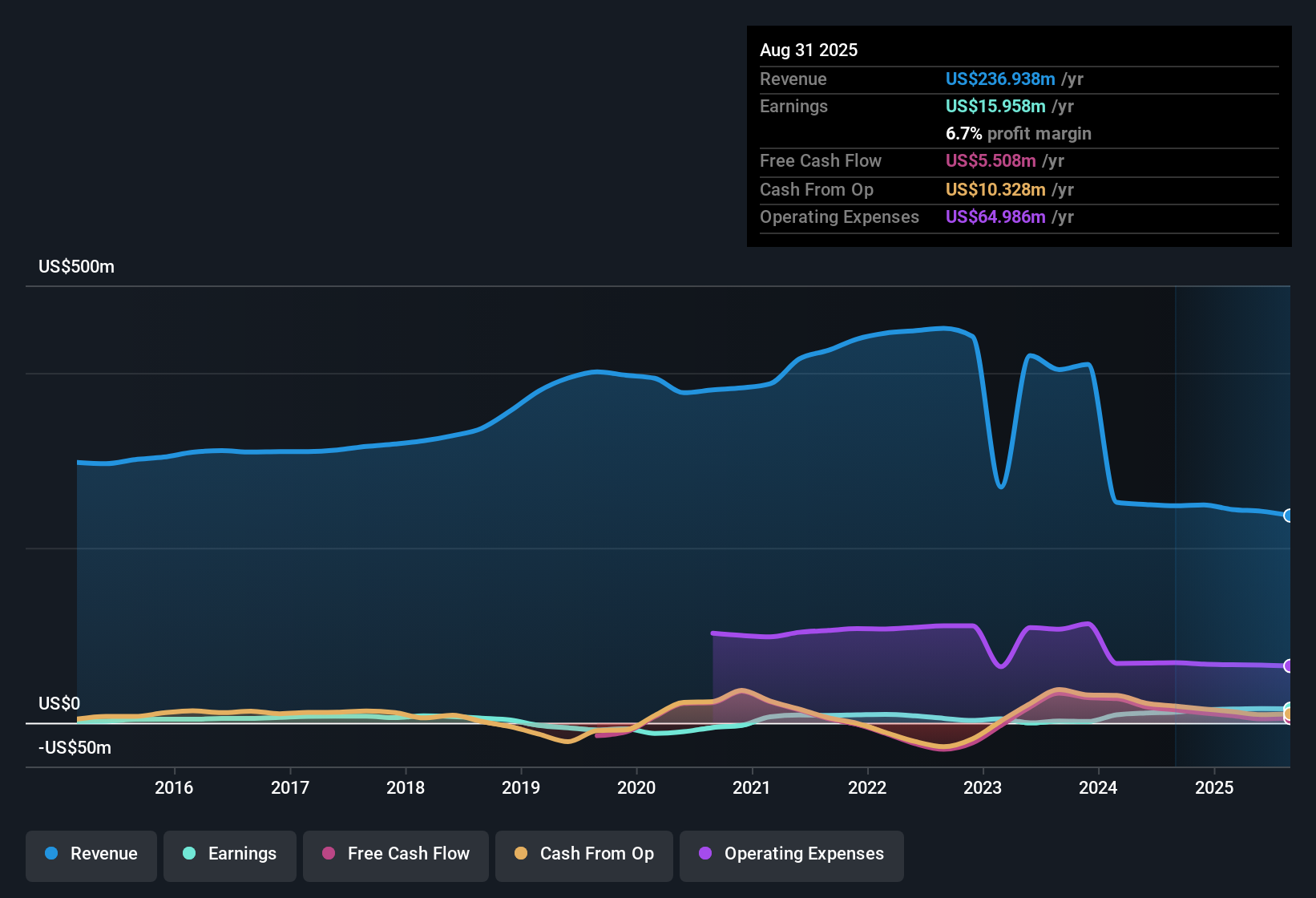

Q.E.P (QEPC) posted a net profit margin of 6.7%, up from 4.9% in the previous year. Earnings have grown at an impressive 32.1% annually over the past five years. The company’s Price-to-Earnings Ratio sits at 7.7x, noticeably lower than both the peer group average of 12.5x and the US Consumer Durables industry average of 10.7x. This frames Q.E.P as particularly attractive on a value basis right now. While these strong numbers point to greater operational efficiency and historically solid profitability, investors may want to keep an eye on the quality of recent earnings due to a notable presence of non-cash items.

See our full analysis for Q.E.P.Next up, we’ll see how these headline earnings figures measure up against the market’s current narratives and expectations. We will also consider whether the story supports or challenges the consensus view.

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Q.E.P's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Q.E.P’s rising non-cash earnings and questions about underlying profitability mean its recent growth may not fully reflect sustainable, cash-backed performance.

If you want clearer signals and stronger earnings quality, check out stable growth stocks screener (2096 results) to focus on businesses with consistently reliable financial progress year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.