Please use a PC Browser to access Register-Tadawul

Get It

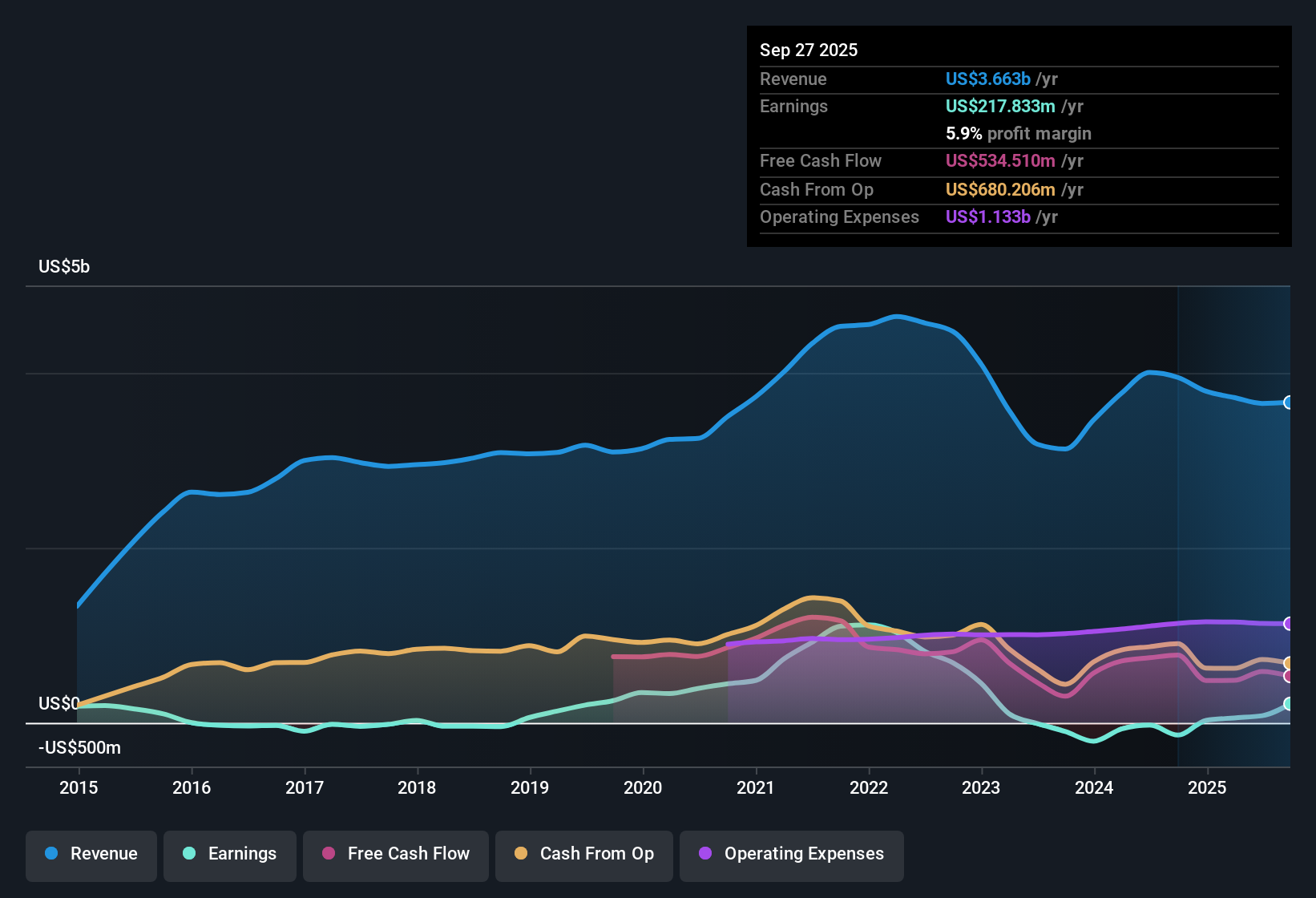

Qorvo (QRVO) Returns to Profitability, But One-Off Loss Challenges Reliability of Earnings Recovery

Qorvo, Inc. QRVO | 89.40 89.40 | -0.62% 0.00% Pre |

Qorvo (QRVO) just returned to profitability, but the company’s earnings have declined by 49.9% per year over the last five years. Looking ahead, analysts expect annual earnings growth of 20.2%, outpacing the projected 16% for the broader US market, while revenue is forecast to rise by a slower 3.8% per year compared to the market’s 10.5%. Despite improved margins as profits came back, a one-off $166.9 million loss still weighs on the quality of recent results. Investors are left to balance the potential for strong projected growth with ongoing concerns about earnings consistency.

See our full analysis for Qorvo.Next, we’ll see how these headline numbers measure up to the key narratives shaping market expectations. Some long-held views may be reinforced, while others could be in for a challenge.

What could nudge Qorvo’s margin expansion story off track or supercharge it? Analysts dig deeper in their full consensus narrative for Qorvo: 📊 Read the full Qorvo Consensus Narrative.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Qorvo on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Think you have a unique take on the figures? Share your perspective and shape a fresh narrative in just minutes: Do it your way

A great starting point for your Qorvo research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Qorvo’s high customer concentration and below-industry revenue growth make its results more volatile and less reliable compared to stable growth peers.

If you want more certainty and steadier fundamentals, use our stable growth stocks screener (2084 results) to pinpoint companies that keep delivering consistent growth year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.