Please use a PC Browser to access Register-Tadawul

Get It

Should Twilio's (TWLO) Vodafone Spain RCS Deal Signal a Turning Point for Its Global Expansion?

Twilio, Inc. Class A TWLO | 127.32 | +1.68% |

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

To be a Twilio shareholder today, you need conviction that enterprises will keep adopting richer communication channels, like RCS, to drive customer engagement, and that Twilio can balance global expansion with improving gross margins. While the Vodafone Spain announcement strengthens Twilio’s international footprint and brings advanced messaging features to a large new market, its impact on margin pressures, the most important short-term catalyst, and on the biggest risk, ongoing margin compression from messaging mix, seems incremental rather than transformational for now.

Among Twilio’s recent actions, the August 2025 launch of global RCS messaging is particularly relevant here, showcasing that Vodafone Spain is one of several international carriers integrating this new channel. These product and carrier partnerships directly support Twilio’s push to drive omnichannel customer engagement, reinforcing the narrative that incremental innovation and international expansion remain key near-term drivers for both growth and gross margin improvements.

However, as Twilio expands messaging options and enters lower-margin regions, investors should be aware that pressing margin headwinds could...

Twilio's narrative projects $5.9 billion revenue and $449.9 million earnings by 2028. This requires 7.9% yearly revenue growth and a $429.7 million earnings increase from $20.2 million today.

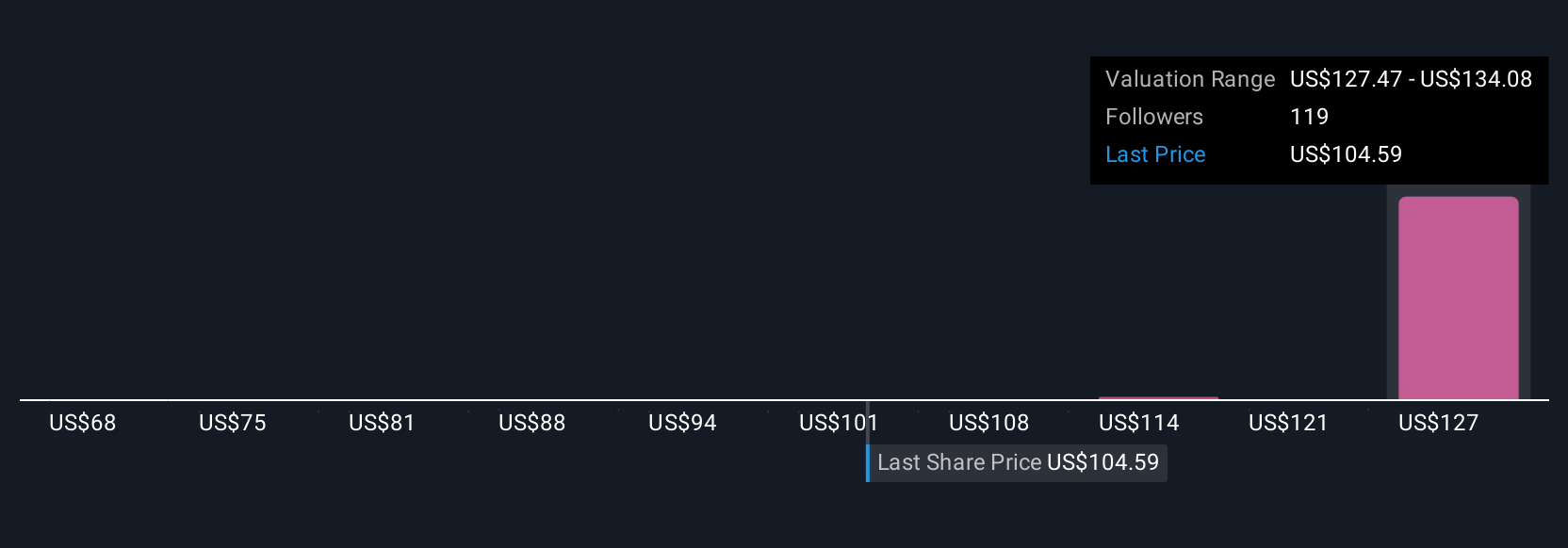

Uncover how Twilio's forecasts yield a $130.88 fair value, a 17% upside to its current price.

Six private investors in the Simply Wall St Community estimate Twilio’s fair value between US$68 and US$131.38 per share. With gross margin improvement still the main focus after international agreements, it’s clear opinions on future performance are diverse, explore the range of views and what could influence outcomes.

Explore 6 other fair value estimates on Twilio - why the stock might be worth 39% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.