Please use a PC Browser to access Register-Tadawul

Get It

Valero Energy (VLO): Evaluating Valuation After Strong 3-Month Share Price Performance

Valero Energy Corporation VLO | 174.14 | -0.46% |

While Valero Energy’s share price dipped fractionally in the past week, it has maintained strong momentum, reflecting renewed optimism about future earnings and sector demand. Over the past year, the company’s total shareholder return has outpaced many peers, underscoring both its resilience and growth potential in a shifting energy landscape.

If Valero’s run has inspired confidence, now is a smart time to broaden your search and discover fast growing stocks with high insider ownership

But with Valero trading near its all-time highs, investors are left to wonder if the recent surge leaves room for further upside or if the market has already accounted for all of the company’s growth prospects.

Valero Energy’s most widely followed narrative sees a fair value of $169 per share, which is slightly above its last close at $160.98. This view positions the stock as modestly undervalued, with valuation supported by upbeat future earnings forecasts and operating improvements just ahead.

The SEC unit optimization project at St. Charles, expected to start up in 2026, is projected to increase the yield of high-value products, potentially boosting future revenues and earnings. Anticipated tight product supply and demand balances, with low product inventories, are expected to support refining fundamentals during the driving season, possibly enhancing refining margins and revenues.

Want to know the backbone of this valuation? The story rests on projected profit margins and a future earnings multiple higher than today’s sector average. Bold calls are hiding in the numbers. But which metric truly drives the upside? Find out what’s fueling analyst conviction in the full narrative.

Result: Fair Value of $169 (UNDERVALUED)

However, unforeseen regulatory changes or operational setbacks in Valero’s renewable segment could quickly challenge the current optimism about its future growth trajectory.

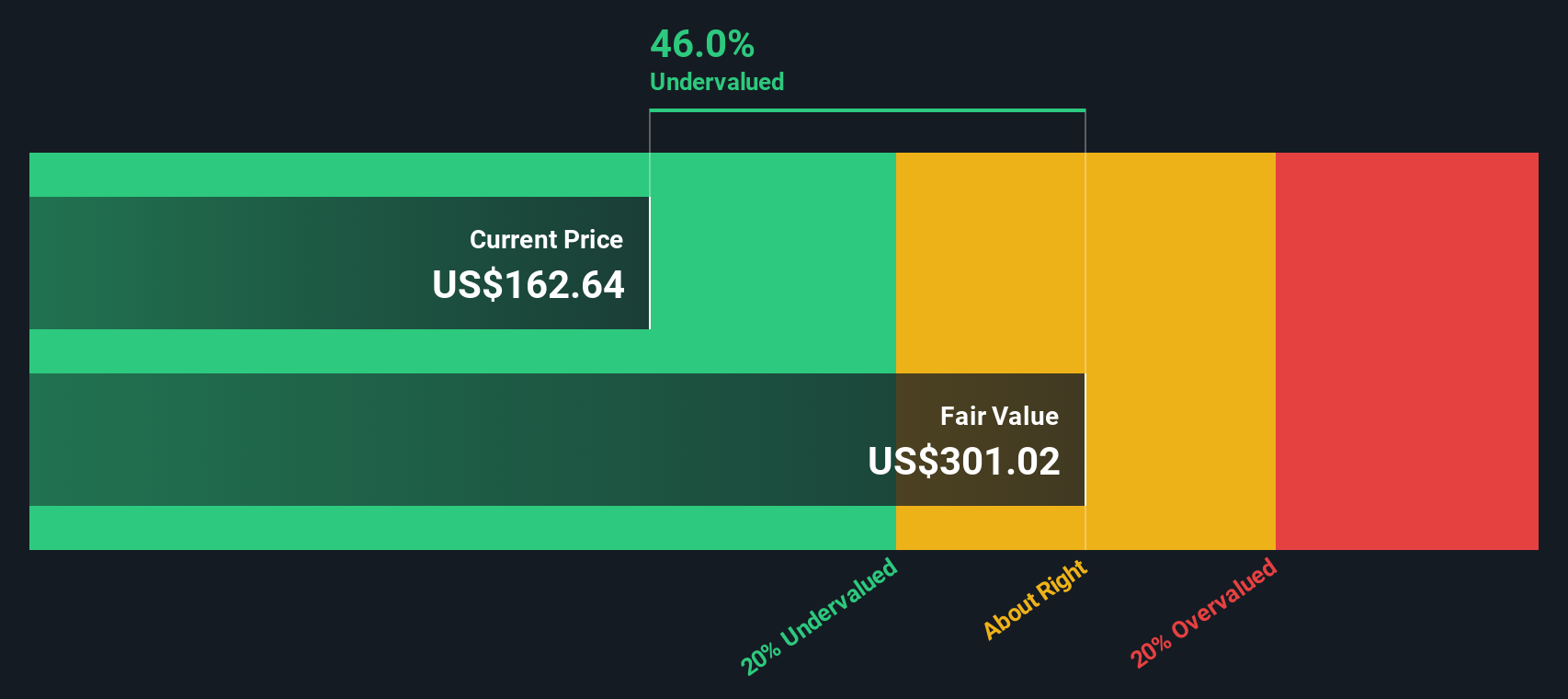

While analyst price targets suggest Valero is fairly valued, our DCF model presents a strikingly different picture. It values the company at $275.10 per share, meaning Valero could be trading at a steep discount of over 40%. Could the market be missing the true long-term potential here, or are the risks being underestimated?

If you see things differently or want to run your own numbers, it takes just a few minutes to craft your personal thesis and perspective. Do it your way

A great starting point for your Valero Energy research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Don’t let opportunities pass you by. There are standout stocks across the market waiting for the right investor. Use these handpicked ideas as your springboard to something bigger.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.