Please use a PC Browser to access Register-Tadawul

Get It

Vicor (VICR) Is Up 6.3% After Surge in IP Licensing Revenue and Share Buyback Completion

Vicor Corporation VICR | 96.83 | +2.42% |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To be a Vicor shareholder, you have to believe the company’s high-value patents and demand for advanced power delivery solutions can sustainably drive both licensing and product revenue, while navigating significant swings in quarterly results. The latest quarter’s surge in IP licensing brought substantial short-term earnings upside, but it also raises the importance of consistency in these infrequent income streams, so while this is a powerful catalyst right now, it amplifies Vicor’s biggest risk: earnings unpredictability tied to the timing and nature of licensing deals.

Of the recent developments, the completion of the US$33.82 million share buyback program stands out most this quarter, as it directly affects per-share earnings metrics amid Vicor’s exceptionally strong IP-driven results. While returning capital to shareholders may not address fundamental order volatility or long-term product revenue risks, buybacks can support near-term valuation during periods of inconsistent results linked to licensing swings.

But behind the upbeat headlines, investors should also be aware that results remain vulnerable to the timing of large, one-off IP deals and...

Vicor's narrative projects $523.8 million in revenue and $45.4 million in earnings by 2028. This requires 11.4% yearly revenue growth and a $20.1 million decrease in earnings from $65.5 million today.

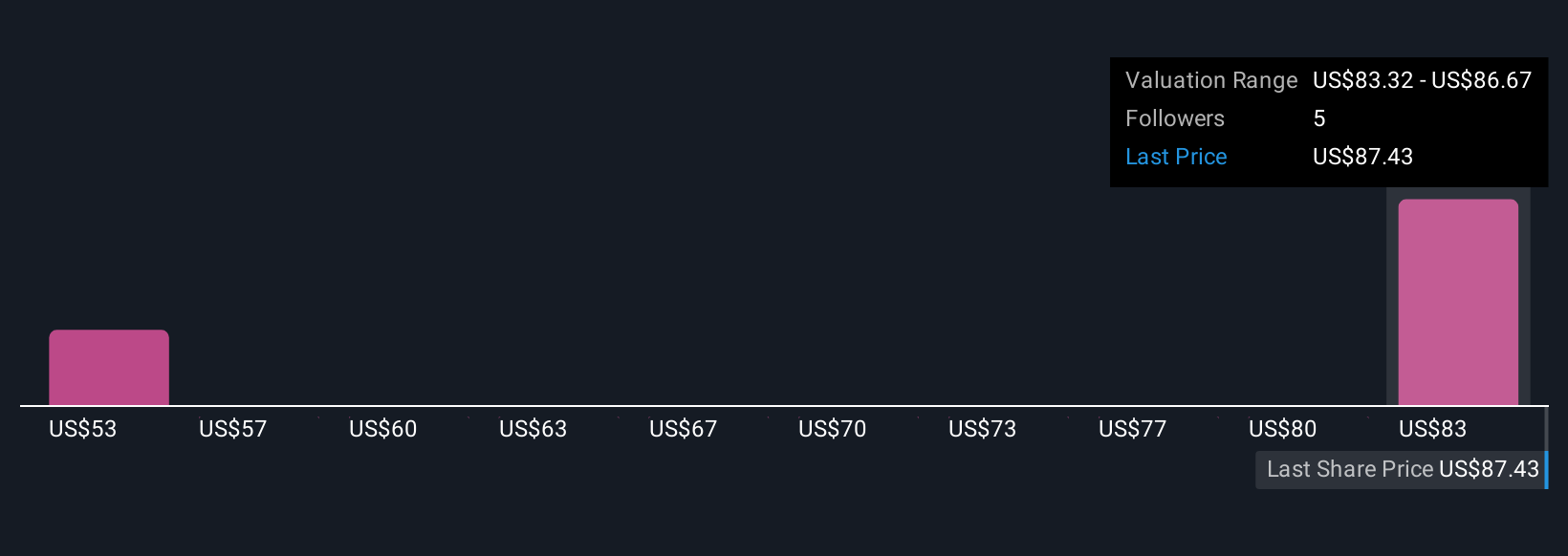

Uncover how Vicor's forecasts yield a $86.67 fair value, a 5% downside to its current price.

Two fair value estimates from the Simply Wall St Community range widely from US$42.89 to US$86.67 per share. While quarterly licensing gains have fueled recent results, this variability continues to shape the outlook, consider how differing views reflect the uncertainty around future earnings streams.

Explore 2 other fair value estimates on Vicor - why the stock might be worth less than half the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.