What Vestis (VSTS)'s Margin-Driven Return To Profitability Means For Shareholders

Vestis Corporation VSTS | 0.00 |

- In May 2026, Vestis Corporation reported second-quarter sales of US$659.44 million, a slight decline from US$665.25 million a year earlier, while swinging from a US$27.83 million net loss to a US$2.6 million net profit and maintaining full-year 2026 revenue guidance for a 2% decline to flat performance.

- Despite broadly flat sales over the past six months, Vestis sharply reduced its net loss from US$27 million to US$3.8 million, highlighting how cost controls and better operating leverage are beginning to reshape the company’s earnings profile.

- We’ll now examine how Vestis’s return to quarterly profitability, driven by margin gains rather than revenue growth, reshapes its investment narrative.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

Vestis Investment Narrative Recap

To own Vestis, you need to believe its margin-focused turnaround can offset flat or slightly declining revenue while it fixes past service and pricing issues. The latest quarter’s modest return to profit supports that thesis, but the main near term catalyst remains sustained margin improvement, and the biggest risk is still that customer churn and pricing pressure keep revenue drifting lower. This earnings print does not materially change that risk balance.

The most relevant update is management’s reaffirmed 2026 revenue outlook of a 2% decline to flat performance. That guidance anchors expectations that near term progress will come from cost controls and better operating leverage rather than new growth. For investors watching catalysts, it sharpens the focus on whether operational changes, not top line acceleration, can consistently lift earnings while Vestis works through its balance sheet and customer retention challenges.

Yet beneath Vestis’s improving margins, investors should be aware that elevated leverage and restrictions on dividends and buybacks until at least 2027 could...

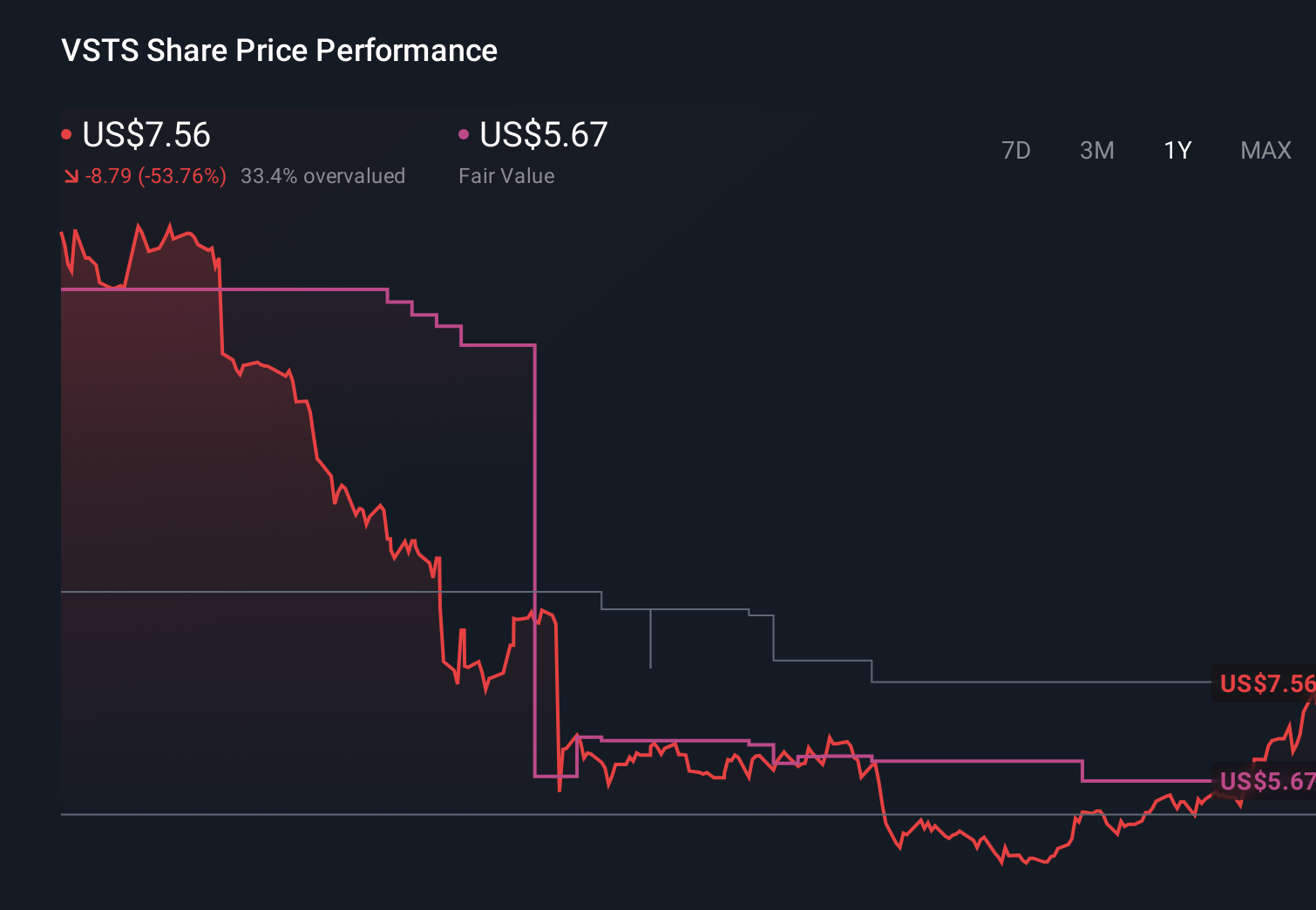

Vestis' narrative projects $2.7 billion revenue and $87.4 million earnings by 2029. This requires fairly flat yearly revenue and a $134.8 million earnings increase from -$47.4 million today.

Uncover how Vestis' forecasts yield a $7.81 fair value, a 33% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Vestis could grow revenue to about US$2.9 billion and earnings to roughly US$120 million, which is far more upbeat than the consensus view that focuses on flat revenue and gradual margin repair; this quarter’s small profit and unchanged guidance may either reinforce that bullish story of accelerating improvement or prompt a rethink, so it is worth comparing how differently you might weigh those upside and downside scenarios.

Explore another fair value estimate on Vestis - why the stock might be worth just $14.00!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vestis research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.