نظرة على تقييم شركة سينشري ألومنيوم (CENX) مع ازدياد التقلبات ونشاط خيارات المؤسسات

Century Aluminum Company CENX | 62.57 | -1.48% |

وقد أدى ارتفاع التقلبات في أسهم شركة Century Aluminum (CENX) إلى تقلبات حادة في أسواق المعادن العالمية ومجموعة من صفقات الخيارات الكبيرة من قبل المستثمرين المؤسسيين، مما أدى إلى انقسام الآراء حول اتجاه السهم على المدى القريب.

تأتي هذه التقلبات المفاجئة في أعقاب أداء قوي، حيث بلغ عائد سعر السهم 35.88% خلال شهر واحد، وعائد إجمالي للمساهمين 124.63% خلال عام واحد. يشير هذا إلى أن الزخم كان يتزايد حتى مع انعكاس تحركات الأسعار قصيرة الأجل لتغيرات في تصورات المخاطر.

إذا كانت التحركات الحادة في أسعار السلع الأساسية ضمن اهتماماتك، فقد تكون هذه لحظة جيدة لتوسيع قائمة مراقبتك والتحقق من الأسهم سريعة النمو ذات الملكية الداخلية العالية .

مع تداول أسهم شركة Century Aluminum بسعر 42.23 دولارًا مقابل سعر مستهدف للمحللين يبلغ 40.00 دولارًا، ومع ذلك تم الإشارة إلى خصم جوهري بنسبة 47.20٪، يجب أن نسأل: هل هذه فجوة قيمة حقيقية، أم أن السوق يسعر بالفعل النمو المستقبلي؟

الرواية الأكثر شيوعًا: 5.6% مبالغ في تقييمها

مع إغلاق سهم شركة Century Aluminum عند 42.23 دولارًا أمريكيًا مقابل قيمة عادلة سردية تبلغ 40 دولارًا أمريكيًا، فإن السعر الحالي أعلى بقليل من التقدير النموذجي، مما يضع مزيدًا من التركيز على افتراضات الأرباح والهوامش الكامنة وراء الفجوة.

يُمكّن توسيع وإعادة تشغيل مصنع ماونت هولي، إلى جانب التقدم المُحرز في إنشاء مصهر جديد في الولايات المتحدة، شركة سينشري ألومنيوم من زيادة إنتاجها من الألومنيوم الأولي في الولايات المتحدة بشكل ملحوظ، مُستفيدةً من الطلب المحلي المتزايد الناتج عن إعادة توطين سلاسل التوريد، والمُحفّز بالتعريفات الجمركية الحكومية وإجراءات الحماية التجارية. ومن المتوقع أن يدعم ذلك نمو الإيرادات في المستقبل، ويُحسّن استيعاب التكاليف الثابتة، وبالتالي يُعزز هوامش الربح الصافية.

من المثير للاهتمام كيف تتضافر عوامل نمو الإيرادات برقمين، وهامش الربح الأوسع، وانخفاض نسبة السعر إلى الأرباح المستقبلية، في هذه الحالة. إن المدخلات الأساسية تبدو أكثر جرأة مما هي عليه في الواقع.

النتيجة: القيمة العادلة 40 دولارًا (مبالغ في تقييمها)

ومع ذلك، قد تتغير القصة بسرعة إذا تم تخفيض الرسوم الجمركية الأمريكية على الألومنيوم أو علاوات الغرب الأوسط، أو إذا تحركت تكاليف الطاقة والمواد الخام ضد شركة سينشري ألومنيوم.

وجهة نظر أخرى: وزارة شؤون الأطفال والأسر تشير إلى الاتجاه الآخر

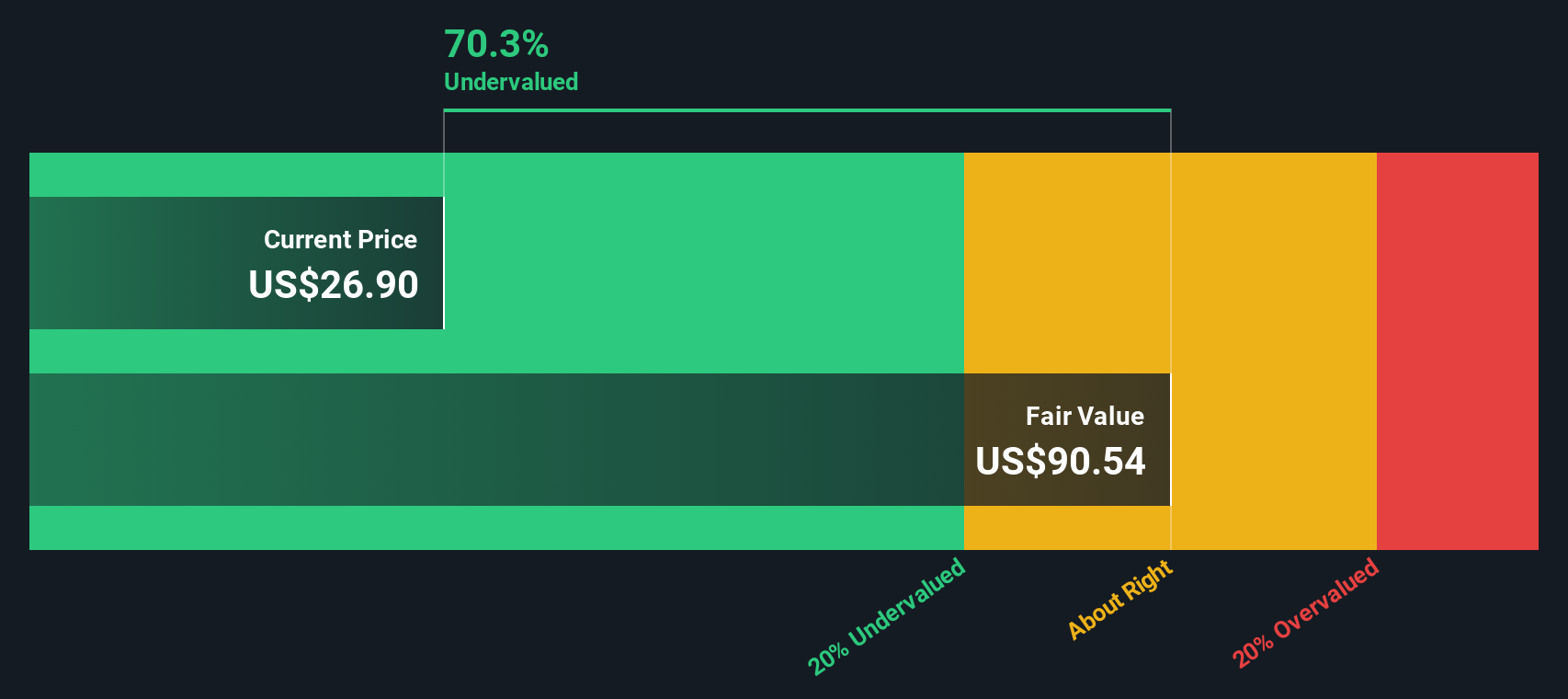

بينما يشير النموذج السردي إلى أن أسهم شركة سينشري ألومنيوم تبدو مبالغًا في قيمتها بنحو 5.6% عند 42.23 دولارًا أمريكيًا مقابل قيمة عادلة تبلغ 40 دولارًا أمريكيًا، فإن نموذج التدفقات النقدية المخصومة لدينا يشير إلى شيء مختلف تمامًا، حيث يتم تداول الأسهم بنحو 47.2% أقل من القيمة العادلة المقدرة البالغة 79.98 دولارًا أمريكيًا. أي من الروايتين تجدها أكثر إقناعًا؟

يقوم موقع Simply Wall St بتحليل التدفقات النقدية المخصومة (DCF) لجميع الأسهم في العالم يوميًا ( راجع أسهم شركة Century Aluminum على سبيل المثال ). نعرض لك كامل عملية الحساب. يمكنك متابعة النتائج في قائمة مراقبتك أو محفظتك الاستثمارية ، وتلقي تنبيهات عند حدوث أي تغيير، أو استخدام أداة فحص الأسهم لدينا لاكتشاف 875 سهمًا مقومًا بأقل من قيمته الحقيقية بناءً على تدفقاتها النقدية . عند حفظ أداة الفحص، نرسل إليك تنبيهات عند إضافة شركات جديدة مطابقة، حتى لا تفوتك أي فرصة استثمارية.

اصنع روايتك الخاصة عن الألمنيوم في القرن الحادي والعشرين

إذا لم تكن موافقًا على هذه الافتراضات، أو كنت تفضل اختبار الأرقام بنفسك، فيمكنك إنشاء عرض مخصص في غضون دقائق قليلة من خلال البدء بـ "افعلها بطريقتك" .

تُعد تحليلاتنا التي تسلط الضوء على مكافأتين رئيسيتين وعلامتين تحذيريتين مهمتين قد تؤثران على قرارك الاستثماري نقطة انطلاق رائعة لأبحاثك حول شركة Century Aluminum.

هل تبحث عن المزيد من أفكار الاستثمار؟

إذا كانت شركة سينشري ألومنيوم ضمن اهتماماتك، فلا تتوقف عند هذا الحد. استغل هذا الزخم للبحث عن فرص أخرى قد تناسب أسلوبك وقدرتك على تحمل المخاطر.

- اكتشف الشركات المرشحة للتحول من خلال الاطلاع على هذه الأسهم الصغيرة البالغ عددها 3555 سهماً والتي تتمتع ببيانات مالية قوية ، حيث تجمع بين أسعار أسهم منخفضة وميزانيات عمومية وتدفقات نقدية يمكنك تقييمها فعلياً.

- استهدف نقطة التقاء الرعاية الصحية والتعلم الآلي من خلال مراجعة هذه الأسهم الـ 29 في مجال الذكاء الاصطناعي للرعاية الصحية والتي تركز على محركات الإيرادات الحقيقية، وليس مجرد الكلمات الرنانة.

- ركز على الفرص التي تركز على التدفق النقدي باستخدام هذه الأسهم الـ 875 المقومة بأقل من قيمتها الحقيقية بناءً على التدفقات النقدية للعثور على الشركات التي تشير فيها أسعار السوق والقيمة النموذجية إلى اتجاهات مختلفة.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.