مراجعة تقييم شركة Artisan Partners (APAM) بعد النتائج القوية وزيادة توزيعات الأرباح

Artisan Partners Asset Management, Inc. Class A APAM | 35.80 | -1.06% |

حظيت شركة Artisan Partners Asset Management (APAM) باهتمام جديد بعد إعلانها عن نتائج الربع الرابع والسنة المالية 2025، بالإضافة إلى إعلانها عن توزيع أرباح مجمعة بقيمة 1.58 دولار أمريكي للسهم الواحد تتضمن دفعة خاصة.

في ظل هذه الظروف، أغلق سعر سهم شركة Artisan Partners لإدارة الأصول عند 44.27 دولارًا أمريكيًا، مسجلاً انخفاضًا بنسبة 2.51% خلال يوم واحد، وعائدًا بنسبة 6.91% منذ بداية العام، وعائدًا إجماليًا للمساهمين بنسبة 50.49% على مدى ثلاث سنوات. يشير هذا إلى أن الزخم قد ازداد على المدى الطويل مقارنةً بالأسابيع الأخيرة، حيث يوازن المستثمرون بين ارتفاع الأرباح، وزيادة توزيعات الأرباح، والتغييرات الإدارية الأخيرة.

إذا كانت آخر أخبار توزيعات الأرباح قد دفعتك للتفكير في الدخل والنمو في أماكن أخرى، فقد يكون الوقت مناسبًا لفحص قائمتنا لأفضل 22 شركة يقودها مؤسسوها بحثًا عن أفكار جديدة تتجاوز شركات إدارة الأصول.

مع تداول أسهم شركة APAM عند 44.27 دولارًا أمريكيًا، وهو سعر أعلى من أحدث هدف سعري للمحللين ولكنه أقل من قيمتها الجوهرية المقدرة، هل يجب أن تنظر إلى المستوى الحالي على أنه نقطة دخول مقومة بأقل من قيمتها الحقيقية أم كعلامة على أن الأسواق تتوقع بالفعل نموًا مستقبليًا؟

الرواية الأكثر شيوعًا: 2.4% مبالغ في تقييمها

تشير الرواية التي تحظى بمتابعة واسعة من قبل شركة Artisan Partners Asset Management إلى قيمة عادلة تبلغ 43.25 دولارًا، أي أقل بقليل من سعر الإغلاق الأخير البالغ 44.27 دولارًا. وهذا يُشير إلى علاوة تقييم متواضعة.

يُجمع المحللون على سعر مستهدف يبلغ 46.125 دولارًا أمريكيًا لسهم شركة Artisan Partners Asset Management، استنادًا إلى توقعاتهم لنمو أرباحها المستقبلية وهوامش ربحها وعوامل المخاطرة الأخرى. مع ذلك، يوجد تباين في توقعات المحللين، حيث يُشير أكثرهم تفاؤلًا إلى سعر مستهدف يبلغ 51.0 دولارًا أمريكيًا، بينما يُشير أكثرهم تشاؤمًا إلى سعر مستهدف يبلغ 41.5 دولارًا أمريكيًا فقط.

هل تتساءل عما يكمن وراء هذا الفارق الضئيل بين السعر الحالي والقيمة العادلة؟ إن افتراضات الإيرادات، وتعديلات هامش الربح، وانخفاض مضاعف الأرباح المستقبلية، كلها عوامل مؤثرة هنا. ويربط السرد الكامل بين هذه العناصر المتغيرة.

النتيجة: القيمة العادلة 43.25 دولارًا (مبالغ في تقييمها)

ومع ذلك، قد يتغير هذا الرأي إذا أثرت فرق الاستثمار الموسعة على هوامش الربح أو إذا فشلت الاستراتيجيات الجديدة في قنوات الثروة الوسيطة في جذب تدفقات الأصول المتوقعة.

وجهة نظر أخرى: تشير المضاعفات إلى خصم

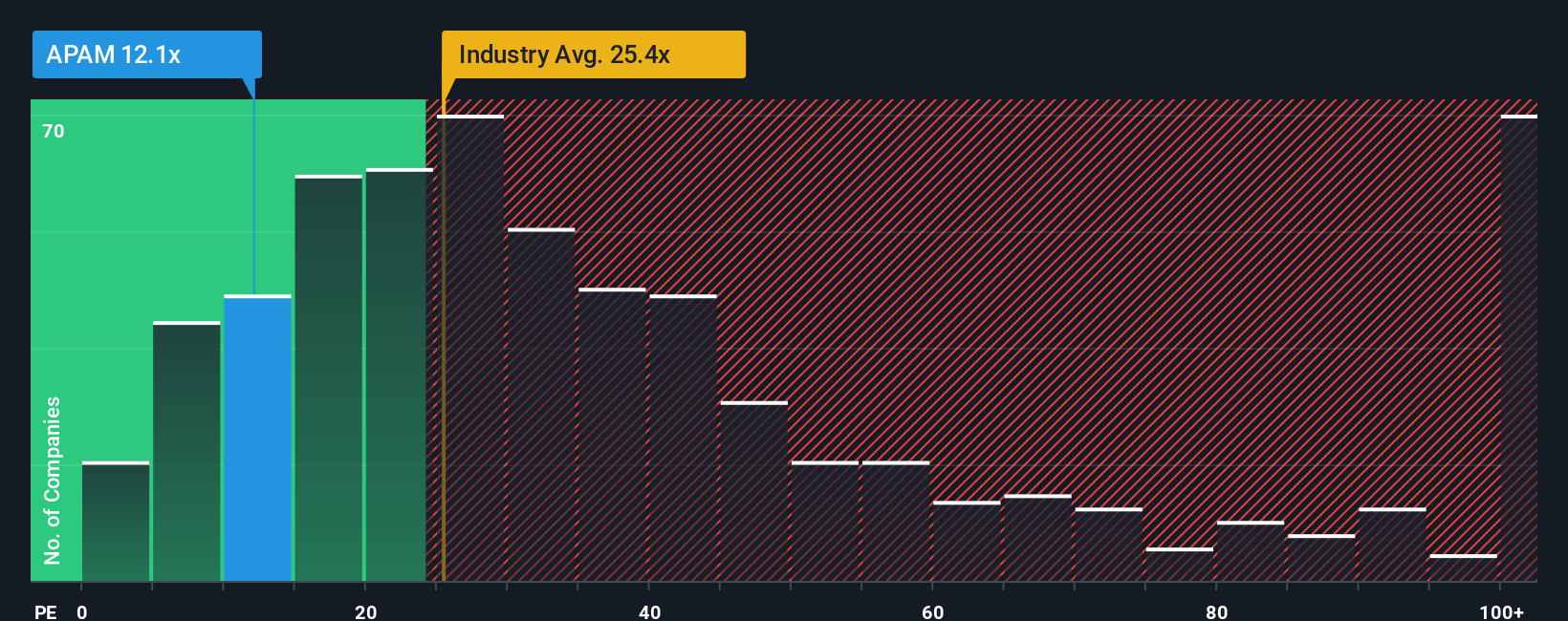

بينما يشير النموذج التحليلي إلى أن سهم APAM مُبالغ في تقييمه بنسبة 2.4%، فإن نسبة السعر إلى الأرباح الحالية البالغة 10.7 ضعف، مقارنةً بنسبة عادلة تبلغ 13.9 ضعف، ومتوسط النسبة لدى الشركات المماثلة البالغ 15 ضعف، تُظهر صورةً مختلفة. ويُشير هذا الفارق إلى أن السوق قد يُبالغ في تقدير المخاطر، أو أنه قد يتجاهل بعض نقاط القوة.

بناء سرد إدارة الأصول الخاص بك لشركاء الحرفيين

إذا نظرت إلى الأرقام وتوصلت إلى استنتاج مختلف، أو كنت تفضل ببساطة مسار بحثك الخاص، فيمكنك بناء سرد مخصص في غضون دقائق قليلة والقيام بذلك على طريقتك الخاصة .

تُعد تحليلاتنا التي تسلط الضوء على 4 مكافآت رئيسية وعلامتين تحذيريتين مهمتين قد تؤثران على قرارك الاستثماري نقطة انطلاق رائعة لأبحاثك حول إدارة الأصول لدى Artisan Partners.

هل تبحث عن المزيد من أفكار الاستثمار؟

إذا ساهمت منصة APAM في تحديد أولوياتك الاستثمارية، فلا تتوقف هنا. الخطوة التالية هي توسيع نطاق فرصك الاستثمارية من خلال أفكار أسهم مختارة بعناية تتناسب مع أسلوبك الاستثماري.

- استهدف الجودة بأسعار مخفضة من خلال الاطلاع على قائمتنا التي تضم 52 سهماً عالي الجودة مقوم بأقل من قيمته الحقيقية ، والتي تجمع بين أساسيات قوية وأسعار قد تكون أقل من قيمتها المقدرة.

- عزز نهجك في تحقيق الدخل من خلال مراجعة 13 شركة رائدة في توزيع الأرباح ، وهي مجموعة من الشركات التي تقدم عوائد أعلى والتي قد تكون جذابة إذا كانت العوائد النقدية المنتظمة مهمة بالنسبة لك.

- أعط الأولوية للمرونة من خلال التحقق من 84 سهمًا مرنًا ذات درجات مخاطر منخفضة ، حيث قد تساعدك الشركات ذات درجات المخاطر المنخفضة في الحفاظ على استقرار محفظتك الاستثمارية خلال تقلبات المزاج العام.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.