تقييم مجموعة إمكور (EME) بعد رفع مستوى التوجيهات وتعزيز أساسيات التعاقد

مجموعة إمكور EME | 803.64 | -1.29% |

تركز التعليقات الأخيرة من شركة ستيفل بشأن مجموعة إمكور (EME) على تعزيز الأساسيات في أعمال المقاولات الميكانيكية والكهربائية، حيث تساعد مستويات النشاط واتجاهات الطلب في تشكيل توقعات المستثمرين للسهم.

يشير العائد الأخير لسعر السهم بنسبة 21.20% خلال شهر واحد ليصل إلى 800.82 دولار أمريكي، إلى جانب عائد سعر السهم بنسبة 29.19% خلال 3 أشهر وعائد إجمالي كبير جدًا للمساهمين على مدى 5 سنوات، إلى أن الزخم يتزايد مع رد فعل المستثمرين على التوجيهات المرتفعة ونشاط الاستحواذ.

إذا دفعك أداء شركة EMCOR إلى التفكير في مواضيع أخرى متعلقة بالبنية التحتية، فقد يعجبك عرضنا لشبكة الطاقة والبنية التحتية الذي يسلط الضوء على 25 سهمًا في مجال تكنولوجيا شبكة الطاقة والبنية التحتية كمرشحين محتملين لمزيد من البحث.

مع تداول أسهم شركة EMCOR عند 800.82 دولار أمريكي، وهو أعلى من السعر المستهدف الأخير للمحللين ولكن مع وجود خصم جوهري واضح وعائد إجمالي كبير للغاية على مدى عدة سنوات، يجب أن تسأل: هل لا تزال هناك فرصة للشراء هنا، أم أن السوق قد بدأ بالفعل في تسعير النمو المستقبلي؟

الرواية الأكثر شيوعًا: 70.8% مبالغ في تقييمها

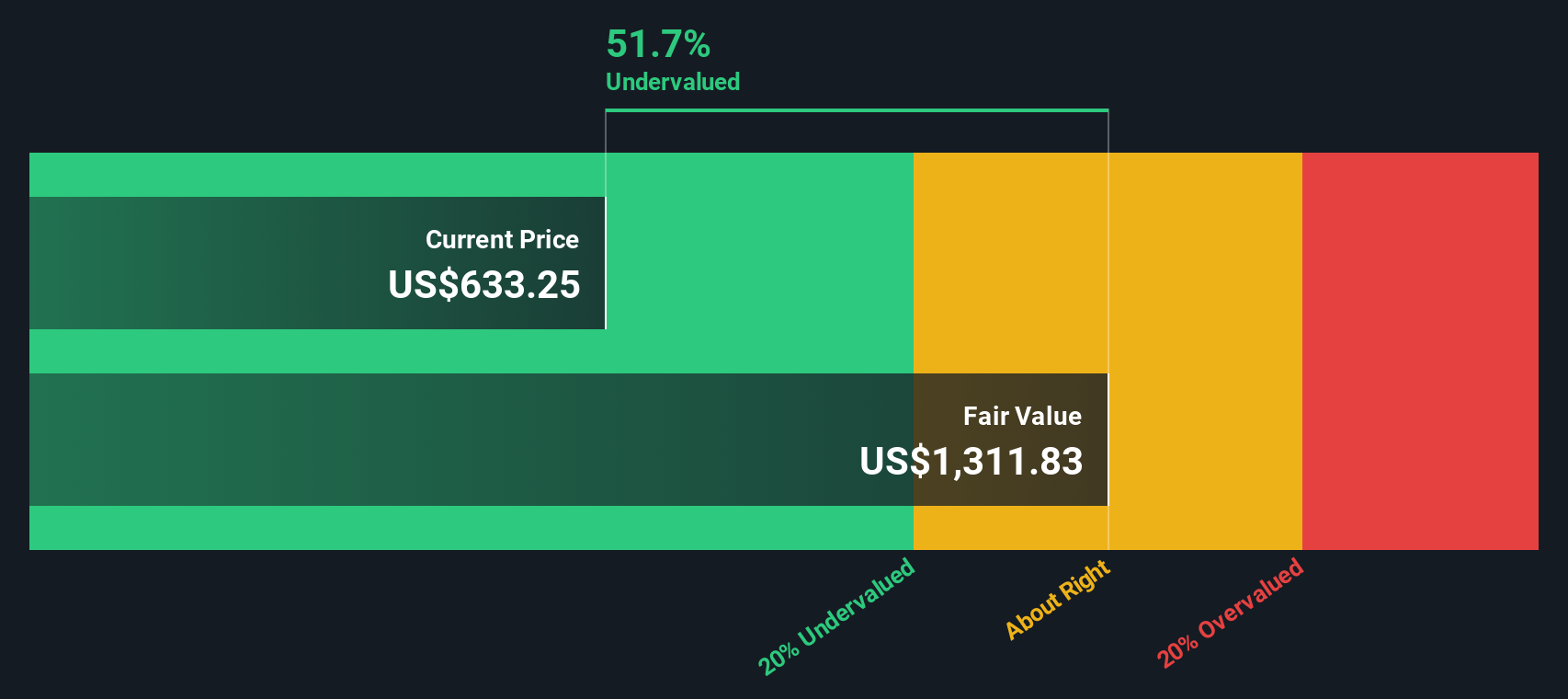

بحسب التحليلات المتداولة على نطاق واسع حول مجموعة إمكور، فإن القيمة العادلة المقدرة للسهم والبالغة 468.79 دولارًا أمريكيًا أقل بكثير من سعر السهم الحالي البالغ 800.82 دولارًا أمريكيًا. وهذا يخلق فجوة تقييم واضحة يتناقش حولها المستثمرون.

بفضل تعرضها القوي لتوسع مراكز البيانات، والكهرباء، والإنفاق على البنية التحتية، وإعادة توطين الصناعات، أظهرت الشركة نموًا ثابتًا في الإيرادات وتحسنًا في الربحية.

اقرأ القصة كاملة. اقرأ القصة كاملة.

هل تتساءل عن شكل القدرة على تحقيق الأرباح وهوامش الربح اللازمة لسد فجوة بهذا الحجم؟ يعتمد التحليل على نمو قوي في الإيرادات، وهوامش ربح أعلى، ومضاعف أرباح مستقبلية يرتبط عادةً بالشركات ذات النمو المرتفع. إذا كنت ترغب في معرفة كيف تتوافق هذه الافتراضات مع القيمة العادلة البالغة 468.79 دولارًا، فإن التحليل الكامل يشرح كل خطوة بالتفصيل.

النتيجة: القيمة العادلة 468.79 دولارًا (مبالغ في تقييمها)

ومع ذلك، قد تنهار هذه القصة إذا تباطأ الإنفاق الحكومي على البنية التحتية، أو إذا بدأت أسواق العمل الضيقة وارتفاع تكاليف الأجور في الضغط على هوامش مشاريع شركة EMCOR.

زاوية أخرى للقيمة

تتناقض القيمة العادلة البالغة 468.79 دولارًا، وفقًا لرواية المستخدم، تناقضًا حادًا مع رأينا بأن سهم EMCOR يُتداول بسعر جيد، سواءً بالمقارنة مع الشركات المنافسة أو مع تقديرنا لقيمة تدفقاته النقدية المستقبلية البالغة 924.20 دولارًا. عندما يُشير أحد النماذج إلى مبالغة في التقييم بنسبة 70.8%، بينما يُشير نموذج آخر إلى خصم، فأي الرأيين تميل إليه؟

قم ببناء سردك الخاص بمجموعة EMCOR

إذا لم تكن مقتنعًا تمامًا بهذه الروايات أو كنت تفضل الاعتماد على عملك الخاص، فيمكنك اختبار الافتراضات، وإعادة صياغة القصة، وبناء وجهة نظر شخصية في غضون دقائق معدودة. افعل ذلك على طريقتك.

تُعد نقطة البداية الجيدة تحليلنا الذي يسلط الضوء على 4 مكافآت رئيسية يتفاءل بها المستثمرون فيما يتعلق بمجموعة EMCOR.

هل تبحث عن المزيد من أفكار الاستثمار؟

إذا ساهمت شركة EMCOR في صقل تفكيرك، فلا تتوقف هنا. وسّع نطاق اهتماماتك الاستثمارية بإضافة بعض الأفكار المركزة التي قد تُعيد تشكيل طريقة تخصيص رأس مالك.

- حدد القيمة المستهدفة أولاً من خلال مسح قائمتنا التي تضم 53 سهماً عالي الجودة مقوم بأقل من قيمته الحقيقية ، حتى لا تكتفي بالتفاعل مع العناوين الرئيسية فحسب، بل تقارن الأسعار بالأساسيات.

- أعط الأولوية للمرونة من خلال 85 سهماً مرناً بدرجات مخاطر منخفضة ، خاصة إذا كنت تريد شركات تشير فحوصات المخاطر فيها بالفعل إلى ملفات أعمال أكثر صلابة.

- اكتشف الفرص غير المعروفة باستخدام أداة الفرز الخاصة بنا التي تحتوي على 23 جوهرة غير مكتشفة عالية الجودة ، قبل أن تصبح هذه الأسماء معروفة للجميع.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.