يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Assessing NBT Bancorp (NBTB) Valuation After Mixed Shareholder Returns And Earnings Expectations

NBT Bancorp Inc. NBTB | 41.53 | +0.29% |

NBT Bancorp (NBTB) has attracted fresh attention after recent share performance data highlighted mixed returns, with modest gains month to date and over the past 3 months alongside a negative 1 year total return.

At a share price of US$42.59, NBT Bancorp’s recent 7 day share price return of 2.58% contrasts with a 1 year total shareholder return decline of 5.13%. However, the 5 year total shareholder return of 44.46% points to a stronger longer term record, suggesting recent momentum is rebuilding after a softer period.

If this kind of mixed performance has you reassessing your watchlist, it could be a good moment to widen your search with fast growing stocks with high insider ownership.

With revenue of US$629.728m, net income of US$149.731m and a model-based intrinsic value suggesting a 51% discount, the key question is whether NBT Bancorp is genuinely undervalued or if the market is already pricing in future growth.

Compared with the last close at US$42.59, the most followed narrative points to a fair value of US$47.80, framing NBT Bancorp as modestly undervalued on its own numbers and assumptions.

Enhanced focus on expanding wealth management and insurance services, especially with access to Evans' customer base, supports a growing share of non-interest, fee-based revenues, leading to a more resilient earnings profile.

Want to see what is powering that valuation gap? The narrative leans on faster earnings growth, rising margins and a future earnings multiple that assumes real staying power. Curious how those ingredients come together into a single fair value number?

Result: Fair Value of $47.8 (UNDERVALUED)

However, the narrative could be tested if loan growth in slower regional markets falls short, or if higher commercial credit costs start to pressure margins.

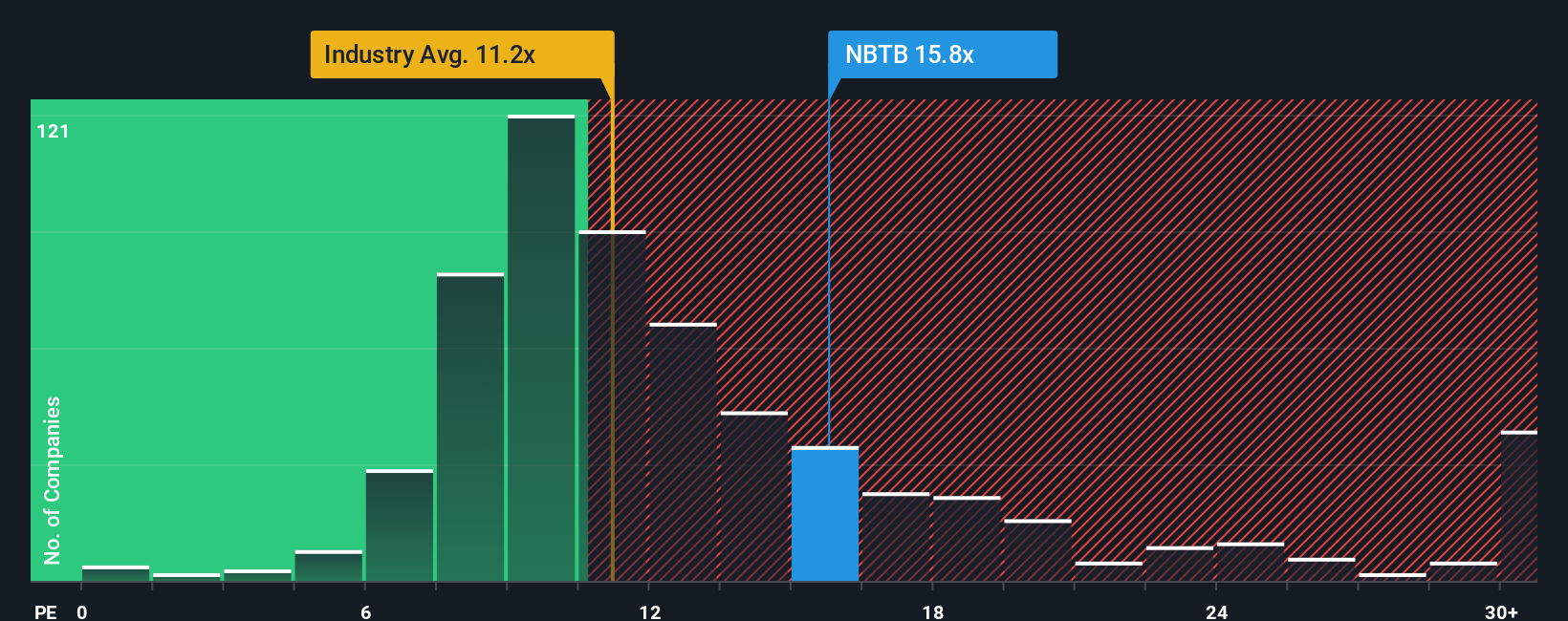

That 10.9% discount to the narrative fair value sits beside a very different message from earnings based pricing. NBT Bancorp trades on a P/E of 14.9x, above both the US Banks industry at 11.9x and peers at 14x, and slightly richer than its own fair ratio of 14.6x.

In plain terms, the market is already paying a bit extra for each dollar of NBT Bancorp’s earnings, which can limit upside if growth or profitability do not line up with expectations. The question for you is whether those earnings forecasts feel strong enough to justify paying that premium.

If you look at the numbers and come to a different conclusion, or simply prefer to test your own view, you can build a full narrative in minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding NBT Bancorp.

If NBT Bancorp has sharpened your thinking, do not stop here, the next move could be finding other opportunities that fit your style even better.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.