يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Assessing Nicolet Bankshares (NIC) Valuation After Robust Earnings And Revenue Beat

Nicolet Bankshares, Inc. NIC | 143.39 | +1.29% |

Nicolet Bankshares (NIC) is back in focus after reporting fourth quarter and full year 2025 results, with higher net income and earnings per share and revenue that topped forecasts, drawing fresh attention from investors.

The latest earnings release and dividend affirmation arrived after a strong run in the shares, with a 30 day share price return of 13.42% and year to date gain of 17.25%. The 1 year total shareholder return of 30.31% and 3 year total shareholder return of just over 2x suggest momentum has been building over time.

If Nicolet’s results have you reassessing regional banks, it could be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

With earnings rising, a dividend affirmed and the stock still trading below some estimated value measures, is Nicolet quietly offering investors a reasonable entry point, or is the market already banking on more growth ahead?

On the numbers, Nicolet Bankshares is priced at a P/E of 13.8x, while our estimates point to a higher fair P/E of 17.9x and the wider peer group sits closer to 19.2x.

P/E is a simple way to compare what investors are currently paying for each dollar of earnings. For a bank like Nicolet, it often reflects expectations around the stability of profits, the quality of the loan book and how earnings might trend over time.

Here, the current 13.8x P/E sits below the estimated fair level of 17.9x, which suggests the market is not fully pricing in the earnings profile implied by our model. At the same time, it is above the broader US Banks industry average of 12.1x. This signals investors are already applying a premium to Nicolet compared with many banking peers.

Compared with the peer average of 19.2x, the gap between the current P/E and where similar companies trade could be a level the market moves toward if earnings trends stay supportive.

Result: Price-to-Earnings of 13.8x (UNDERVALUED)

However, risks around regional credit conditions and any shift in investor sentiment toward bank valuations could quickly change how that 13.8x P/E is viewed.

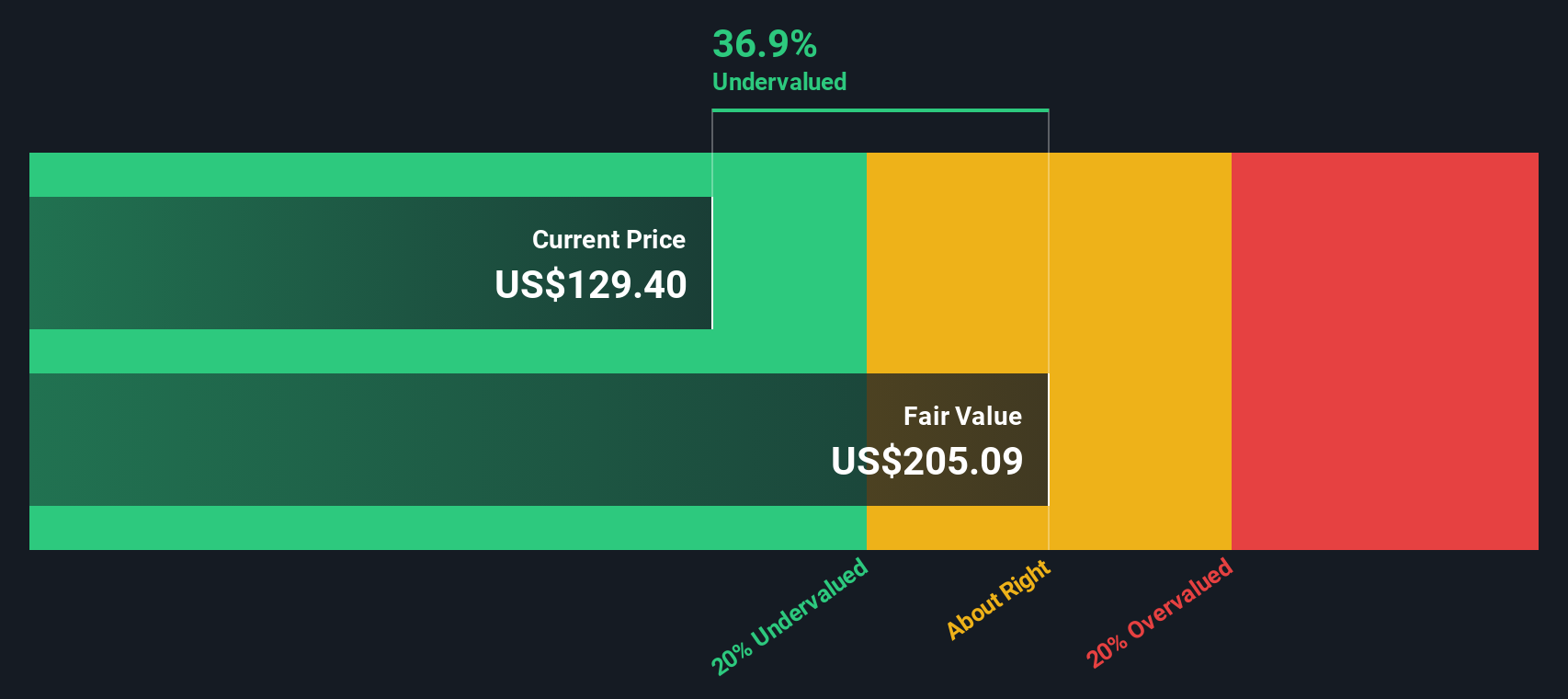

While the 13.8x P/E hints at some value support, our DCF model points to a different anchor. With the shares at $141.28 and our estimate of future cash flow value at $192.19, Nicolet screens as undervalued. The question is whether those cash flow assumptions prove realistic.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nicolet Bankshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 864 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you see the numbers differently or want to put your own stamp on the story, you can build a custom view in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nicolet Bankshares.

If Nicolet has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to line up your next round of ideas before the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.