يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Assessing Veracyte (VCYT) Valuation As Recent Momentum Meets An Expensive P/E Ratio

Veracyte, Inc. VCYT | 35.63 | -1.79% |

Veracyte (VCYT) has drawn attention after recent trading, with the share price most recently closing at $43.30. With mixed short term returns and a stronger past 3 months, investors are reassessing the story.

The 3.86% 1 day share price return and 21.49% 90 day share price return suggest momentum has been building recently, while the 0.58% 1 year total shareholder return and 68.16% 3 year total shareholder return point to a mixed longer term journey.

If Veracyte has you rethinking opportunities in diagnostics, it could be a good moment to broaden your watchlist across other healthcare names using healthcare stocks.

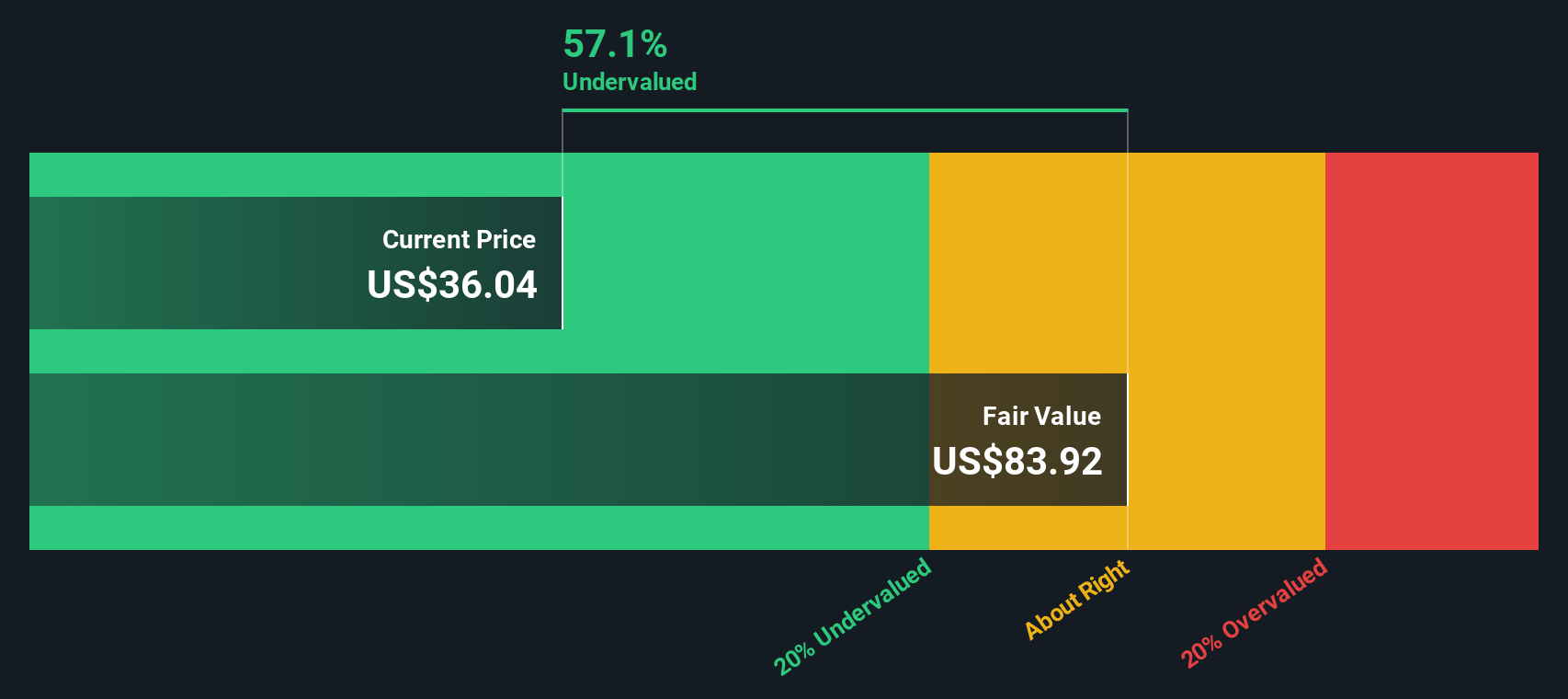

With Veracyte posting revenue of $495.141m, net income of $30.317m, and trading at $43.30 with an estimated intrinsic discount of 28.685%, you have to ask: is there real upside here, or is the market already pricing in future growth?

On current numbers, Veracyte trades on a P/E of 112.9x at a last close of $43.30, which sits well above several key comparison points.

The P/E ratio compares the share price to the company’s earnings per share and is a common way investors frame what they are paying for each dollar of profit, especially in sectors like biotech where profit visibility matters.

For Veracyte, this 112.9x P/E is described as expensive when lined up against the US Biotechs industry average of 19.8x and a peer average of 66.3x. It is also high compared to an estimated fair P/E of 23.8x that our model suggests the market could eventually lean toward based on broader sector relationships.

Result: Price-to-Earnings of 112.9x (OVERVALUED)

However, you also have to weigh a 112.9x P/E and a 5 year total return of 16% against the risk of any stumble in diagnostic adoption or reimbursement pressure.

The high 112.9x P/E makes Veracyte look expensive, but our DCF model offers a different perspective. On that view, the shares at $43.30 are trading below an estimated future cash flow value of $60.72, which points to a potential valuation gap.

That contrast, expensive on earnings yet below our DCF estimate, raises a simple question for you as an investor: is the market overpaying for today’s profits or underestimating the cash the business could generate over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Veracyte for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you look at this and come to a different conclusion, or simply want to test your own assumptions against the data, you can build a personalized view of Veracyte in just a few minutes using Do it your way.

A great starting point for your Veracyte research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

If Veracyte has sharpened your focus, do not stop here. The next step is lining up a few more targeted ideas that could sharpen your overall portfolio thinking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.