يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Could Peer Bank Disclosures Reshape Investor Trust in PFBC’s Loan Quality Expectations?

Preferred Bank PFBC | 100.42 | +0.33% |

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Owning Preferred Bank stock requires conviction in its ability to maintain solid asset quality and disciplined deposit pricing, despite lending concentration in California and commercial sectors that may be exposed to localized shocks. While recent peer disclosures reignited concerns about regional bank loan quality, they are not expected to materially alter the immediate outlook for Preferred Bank’s most significant catalyst, continued expansion into high-growth markets, nor do they directly amplify its biggest current risk of local loan book exposure.

Preferred Bank’s recent dividend declaration, with a 3.3% yield and payout scheduled for October 21, stands out as a relevant signal of management’s confidence in the bank’s capital strength. This dividend action, paired with steady earnings per share, helps anchor the near-term shareholder narrative even as short-term volatility picks up on sector headlines.

By contrast, investors should be aware that reliance on commercial and C&I lending in specific markets also means ...

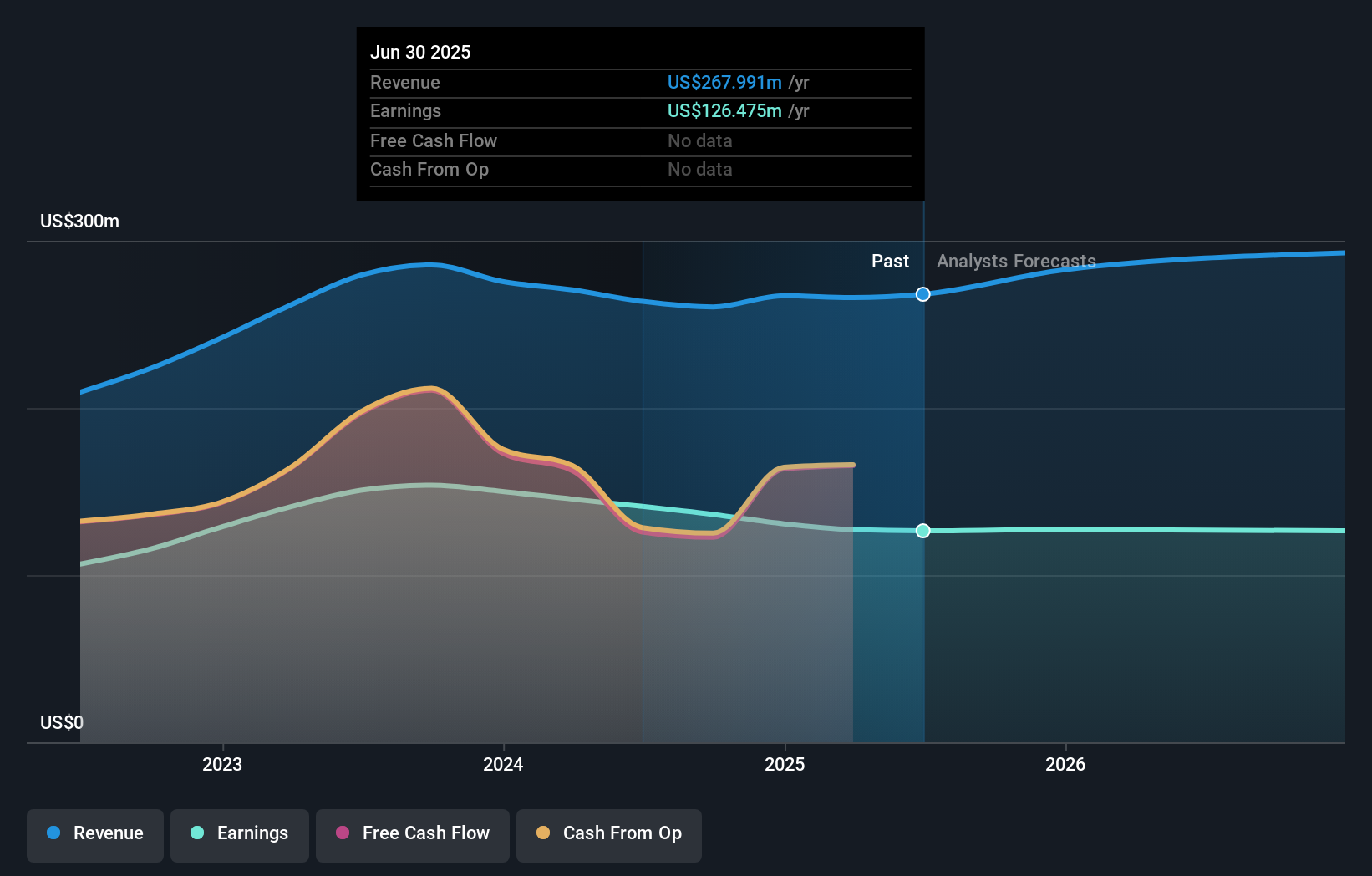

Preferred Bank's outlook projects $320.4 million in revenue and $126.6 million in earnings by 2028. This requires a 6.1% annual revenue growth rate and a negligible earnings increase of $0.1 million from current earnings of $126.5 million.

Uncover how Preferred Bank's forecasts yield a $107.00 fair value, a 25% upside to its current price.

Two fair value estimates from the Simply Wall St Community span a wide range, from US$107 to US$226.69. Opinions remain split as the potential for loan quality risks continues to shape expectations about future stability and recovery, explore more perspectives to sharpen your own outlook.

Explore 2 other fair value estimates on Preferred Bank - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.