يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Does the Recent Insider Sale Reveal Shifting Priorities for NXP Semiconductors' (NXPI) Management Team?

NXP Semiconductors NV NXPI | 203.03 | -1.08% |

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

For investors in NXP Semiconductors, the central belief is in the company’s ability to capitalize on long-term growth in automotive, industrial, and IoT semiconductor demand, balanced against near-term pressures on margins and inventory. The CFO’s share sale and recent comments about margin and inventory headwinds do not appear to meaningfully affect the most important short-term catalyst, which remains the normalization of Automotive Tier 1 customer inventories, but they do highlight uncertainty around operating leverage as costs rise.

The company’s recent announcement of an advanced Electrochemical Impedance Spectroscopy (EIS) chipset for EV battery management is highly relevant in this context, underscoring NXP’s commitment to driving automotive content growth, a key catalyst for revenue and margin expansion as vehicle electrification accelerates. Such innovation is central for supporting end-demand recovery, even as margin challenges persist.

Yet, in contrast to these product-driven tailwinds, rising internal inventories and the associated risk of weaker-than-expected end-market demand remain critical points investors should be aware of...

NXP Semiconductors is projected to achieve $15.5 billion in revenue and $3.5 billion in earnings by 2028. This outlook is based on analysts forecasting an annual revenue growth rate of 8.7% and an earnings increase of $1.4 billion from the current $2.1 billion.

Uncover how NXP Semiconductors' forecasts yield a $258.19 fair value, a 31% upside to its current price.

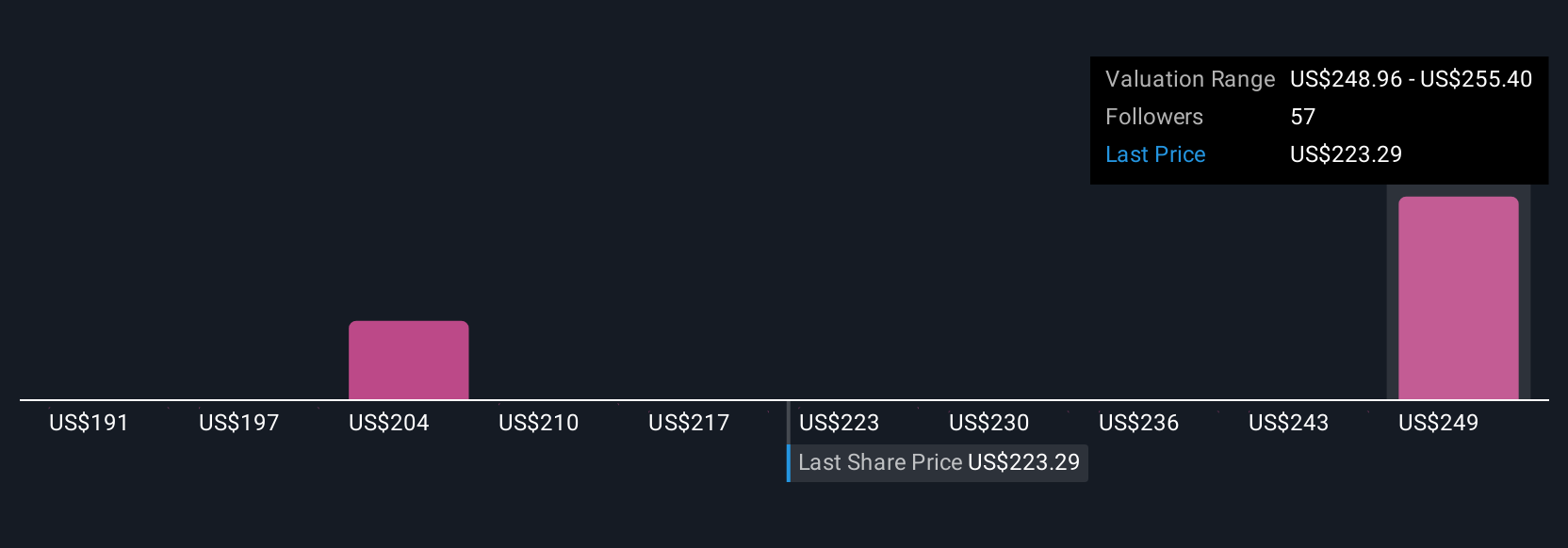

Simply Wall St Community members provided 10 fair value estimates for NXP Semiconductors, ranging widely from US$187.08 to US$294.09 per share. Many highlight margin pressure and inventory volatility as crucial to understanding the company’s earnings potential, so explore these contrasting viewpoints for deeper insight.

Explore 10 other fair value estimates on NXP Semiconductors - why the stock might be worth 5% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.