يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Essent Group (ESNT) Margin Compression Challenges Bullish Narrative Of High Profitability

Essent Group Ltd. ESNT | 60.36 | +0.23% |

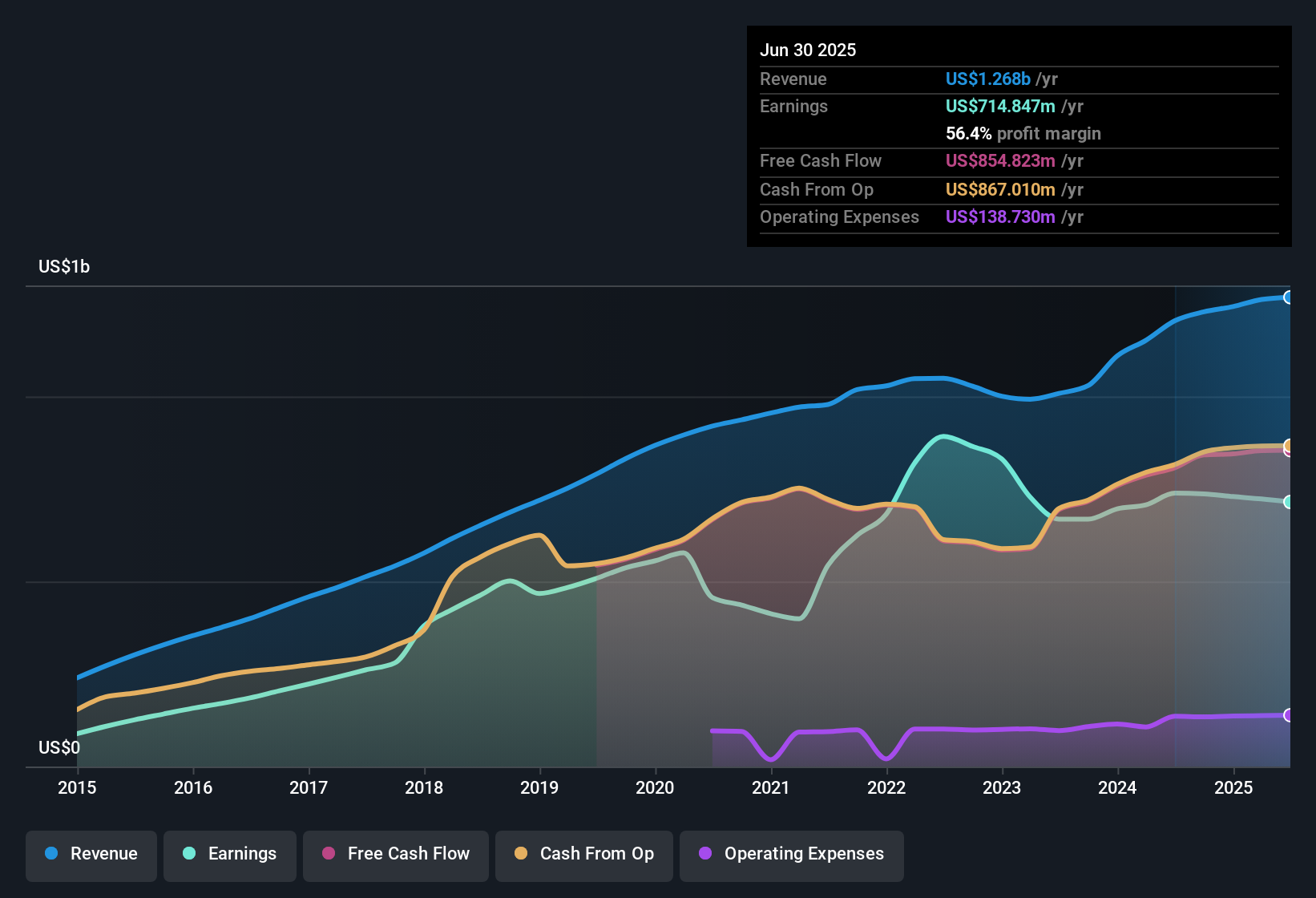

Essent Group (ESNT) has posted its latest FY 2025 numbers, with Q3 total revenue at US$311.8 million and basic EPS of US$1.69, backed by net income of US$164.2 million. The company has seen quarterly revenue range between US$312.9 million and US$344.4 million over the last six reported periods, while basic EPS has moved between US$1.60 and US$1.95 over the same stretch, giving investors a clear view of how the top line and EPS have tracked together through recent quarters. Set against a trailing 12 month net profit margin of 55.6%, the fresh results keep the focus squarely on how efficiently Essent is converting revenue into profit.

See our full analysis for Essent Group.With the headline numbers on the table, the next step is to see how this earnings run rate lines up against the big narratives around Essent, from its profit margins to the way investors talk about its long term earnings power.

Bulls and skeptics are clearly reading the same valuation gap in very different ways, so if you want to see how those arguments are laid out in full, it is worth going through the current community view on the company: 📊 Read the full Essent Group Consensus Narrative.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Essent Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this data sparks a different angle for you, shape that view into a full story in just a few minutes, Do it your way

A great starting point for your Essent Group research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Essent's recent margin compression from 59.5% to 55.6% and trailing earnings lagging its 5.2% annual trend highlight pressure on both profitability and growth consistency.

If that mix of softer margins and slowing earnings makes you want more upside for every dollar you commit, check out 53 high quality undervalued stocks that already screen for quality at cautious prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.