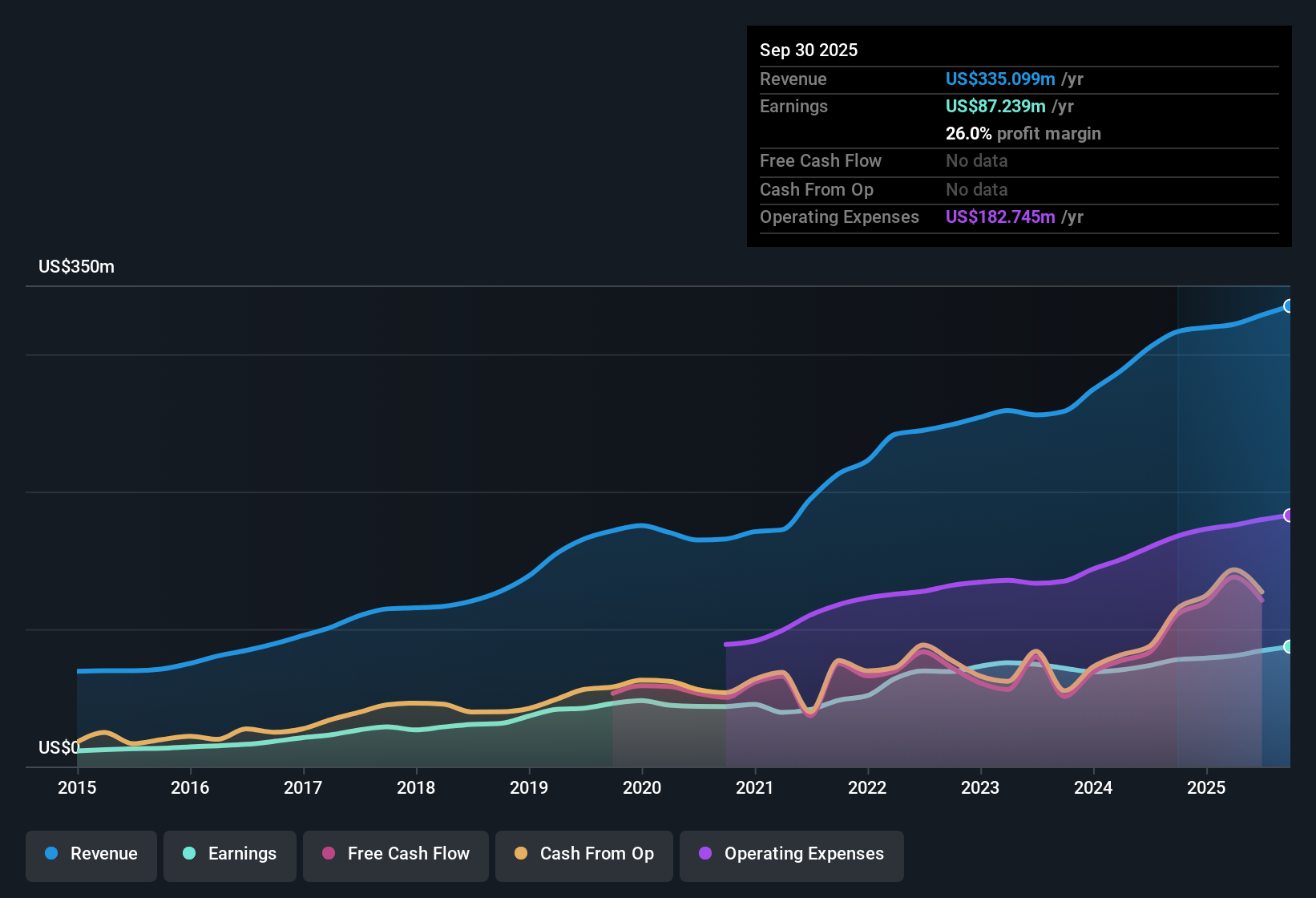

First Mid Bancshares (FMBH) has wrapped up FY 2025 with fourth quarter revenue of US$85.9 million and basic EPS of US$0.99, supported by quarterly net income of US$23.7 million. The trailing twelve month figures show revenue of US$339.3 million and EPS of US$3.84. Over recent periods the company has reported revenue of US$79.3 million in Q3 2024 and US$85.9 million in Q4 2025, with EPS over the same timeframe moving from US$0.81 to US$0.99 as trailing twelve month net income reached US$91.7 million. Alongside a net profit margin that has risen to 27% over the last year, these results highlight profitability as a central focus for investors reviewing the latest numbers.

See our full analysis for First Mid Bancshares.

With the headline results now available, the next step is to see how these earnings and margin trends compare with the most widely discussed narratives around First Mid Bancshares and to consider where those narratives may need updating.

NasdaqGM:FMBH Earnings & Revenue History as at Jan 2026

Margins and EPS show steady support

Across FY 2025, Basic EPS ranged between US$0.93 and US$0.99 per quarter, with trailing twelve month EPS at US$3.84 alongside a 27% net profit margin, so earnings stayed relatively tight even as revenue moved between US$79.3 million and US$85.9 million across the reported periods.

What really backs a bullish angle is how earnings and margins line up, because trailing twelve month net income reached US$91.7 million with 16.3% one year earnings growth and a 27% margin, while five year earnings growth averaged 12.9% per year, which gives bulls a data point that earnings efficiency rather than big revenue swings has been doing most of the work.

Supporters can point to quarterly net income between US$19.2 million and US$23.7 million during FY 2025, which sits comfortably above the US$19.2 million level seen in Q4 2024, as evidence that profitability held up using the reported figures.

At the same time, the move from a 24.7% margin a year earlier to 27% now fits the bullish argument that the bank is getting more out of each dollar of the US$339.3 million in trailing twelve month revenue.

To see how that profitability story compares with different long term growth views and risk angles, you can weigh it against the full narrative range in one place.

📊 Read the full First Mid Bancshares Consensus Narrative.

Loan book and credit quality stay contained

Total loans sat between US$5,655.8 million and US$5,852.6 million across the reported quarters, while non performing loans stayed in a band of US$18.2 million to US$29.8 million, so credit issues were present but limited relative to the multi billion loan base given in the data.

Bears often worry about credit risk at regional banks, and this data gives them and bulls something to argue over, because non performing loans moved from US$29.8 million in Q4 2024 to US$26.6 million in Q1 2025 and US$22.2 million by Q3 2025, while total loans stayed around the mid US$5,000 million level, so critics might still focus on absolute troubled loan dollars even as the figures remain small versus the full book.

Those cautious on the stock may highlight that non performing loans were US$26.6 million in Q1 2025 compared with US$18.2 million in Q3 2024, using that swing as a reminder that credit costs can move around even when earnings look strong.

Supporters can counter that non performing loans of US$22.2 million in Q3 2025 versus total loans of US$5,852.6 million still represent a relatively small slice of the balance sheet using the numbers provided.

Valuation gap and revenue outlook pull in opposite directions

The current share price of US$41.45 sits well below the DCF fair value of US$87.75 and the single analyst price target of US$46.29, while the trailing P/E of 10.8x is lower than both the US Banks industry at 11.7x and peers at 11.4x, and revenue is forecast to see about a 1.5% decline per year over the next three years according to the figures provided.

What creates tension for a more bearish stance is this mix of apparent valuation support and softer top line expectations, because critics can point to the revenue decline forecast of around 1.5% per year and the description of an unstable dividend history, while others may focus on the 16.3% one year earnings growth and margin improvement to 27% as signs that profitability per share has been resilient even if headline revenue growth is not in focus.

Skeptics might argue that a forecast revenue decline over several years can pressure fee growth and loan demand, which matters even if EPS tracked at US$3.84 on a trailing twelve month basis in the latest data.

Supporters can reply that a P/E of 10.8x on that EPS level plus a DCF fair value more than double the share price still point to room between

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on First Mid Bancshares's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

For all the margin strength, the key weak spot is the forecast 1.5% annual revenue decline over the next three years, which keeps top line momentum under pressure.

If that revenue drag makes you cautious, shift your attention to stable growth stocks screener (2171 results) to focus on companies with steadier sales and earnings profiles that can support more consistent performance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.