يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

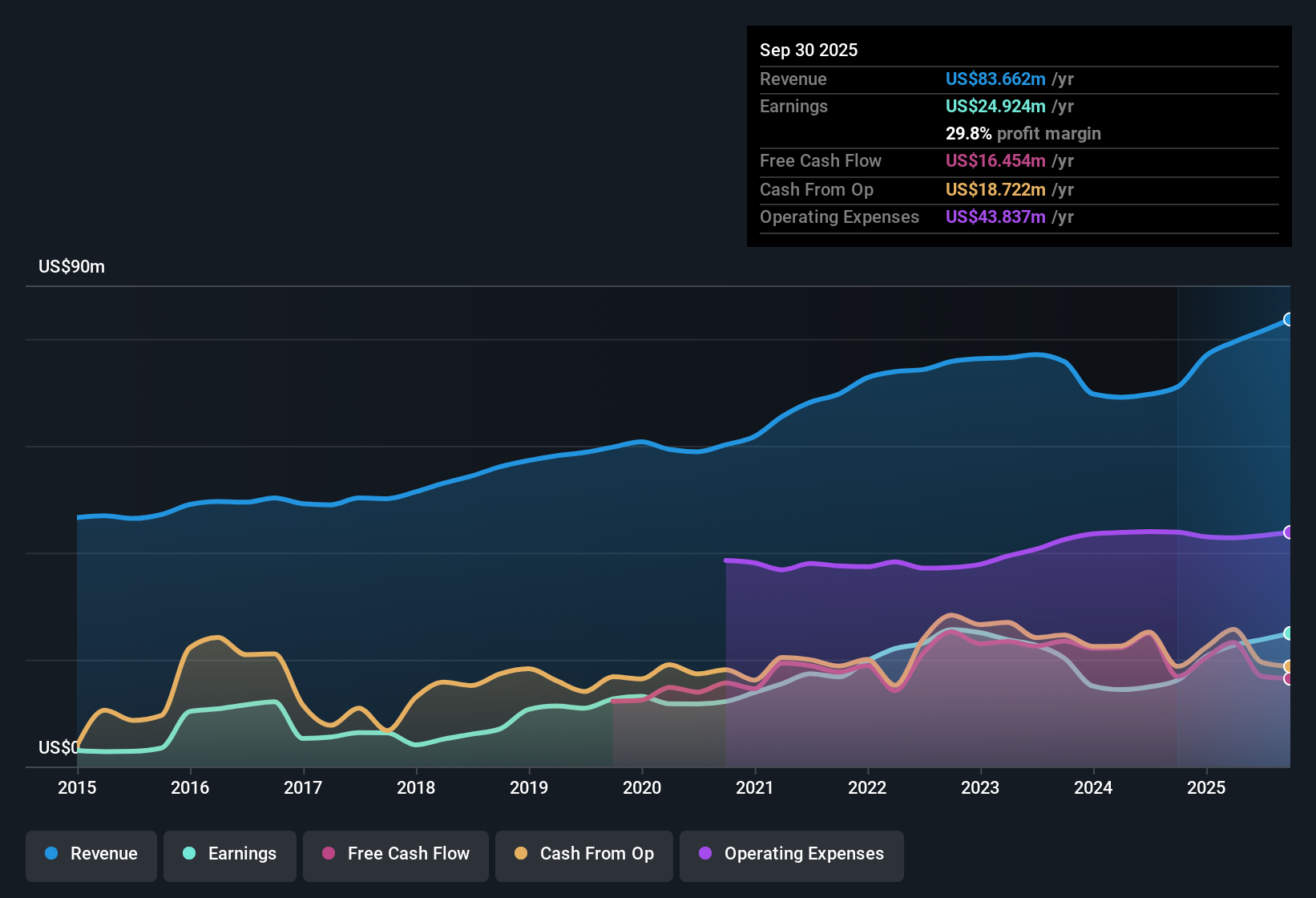

First United (FUNC) Net Margins Surge to 29.8%, Reinforcing Bullish Value Narrative

First United Corporation FUNC | 38.60 38.60 | -0.41% 0.00% Pre |

First United (FUNC) reported standout earnings growth of 54.4% over the past year, far outpacing its 5-year average of 5.3% per year. Net profit margins reached 29.8%, rising from 22.7% in the prior year, while shares are currently trading at $36.98, well below an estimated fair value of $68.47. With only one minor risk flagged and multiple rewards highlighted, including high-quality past earnings, expanding profit and revenue, and a strong value profile, the latest results point to improved profitability and constructive investor sentiment.

See our full analysis for First United.The next step is seeing how these headline numbers stack up against the main narratives: where the results echo street views, and where they might challenge them.

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on First United's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Despite standout profit growth, First United still lags sector leaders in forecasted long-term revenue and earnings expansion. This poses questions about its future pace compared to peers.

If you're seeking smoother performers, target steady results and fewer surprises by focusing on stable growth stocks screener (2087 results) that deliver growth with greater consistency year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.