يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Here's Why Huntington Ingalls Industries (NYSE:HII) Has A Meaningful Debt Burden

Huntington Ingalls Industries, Inc. HII | 321.63 | -1.58% |

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Huntington Ingalls Industries, Inc. (NYSE:HII) does carry debt. But should shareholders be worried about its use of debt?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

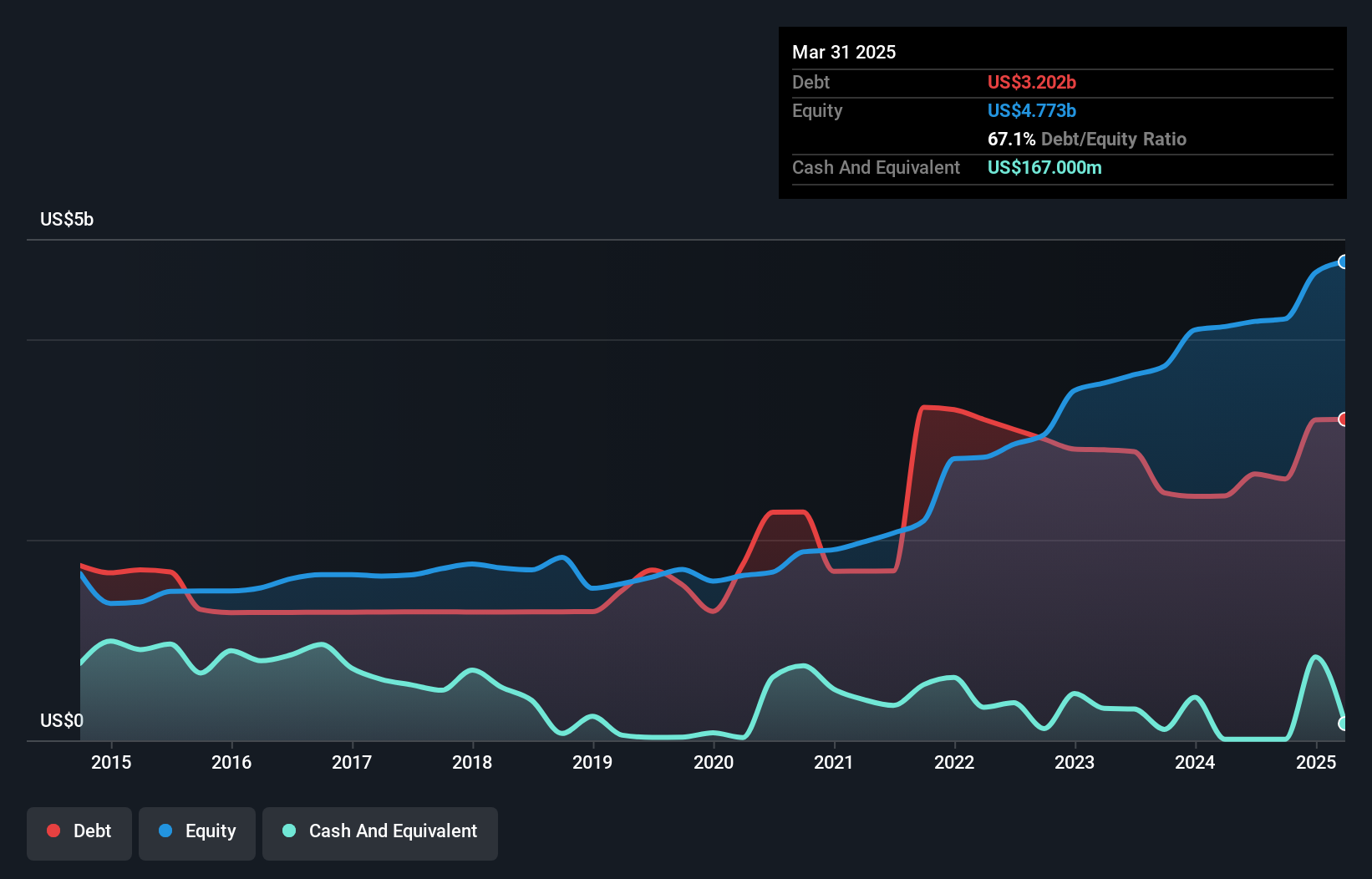

The image below, which you can click on for greater detail, shows that at March 2025 Huntington Ingalls Industries had debt of US$3.20b, up from US$2.44b in one year. However, it does have US$167.0m in cash offsetting this, leading to net debt of about US$3.04b.

Zooming in on the latest balance sheet data, we can see that Huntington Ingalls Industries had liabilities of US$2.86b due within 12 months and liabilities of US$4.47b due beyond that. Offsetting this, it had US$167.0m in cash and US$2.56b in receivables that were due within 12 months. So it has liabilities totalling US$4.61b more than its cash and near-term receivables, combined.

Huntington Ingalls Industries has a market capitalization of US$9.77b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Huntington Ingalls Industries has a debt to EBITDA ratio of 3.0, which signals significant debt, but is still pretty reasonable for most types of business. However, its interest coverage of 13.0 is very high, suggesting that the interest expense on the debt is currently quite low. The bad news is that Huntington Ingalls Industries saw its EBIT decline by 15% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Huntington Ingalls Industries can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Huntington Ingalls Industries recorded free cash flow of 38% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Neither Huntington Ingalls Industries's ability to grow its EBIT nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Taking the abovementioned factors together we do think Huntington Ingalls Industries's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Huntington Ingalls Industries (at least 1 which is concerning) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.