يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Informatica (INFA): Evaluating Fair Value as Growth Moderates and Market Waits for Next Move

Informatica Inc. INFA | 24.79 | Delist |

Informatica (INFA) shares have seen some movement as investors weigh the company’s recent performance and market positioning. While the past month showed a slight dip, year-over-year returns remain positive, which may indicate underlying stability.

After riding out some ups and downs, Informatica’s 1-year total shareholder return of 3.8% points to steady progress, even as momentum has slowed recently. With the share price now at $24.88, it seems investors are pausing to reassess growth prospects versus potential risks, following a period of stronger, longer-term gains.

If you’re interested in spotting what else the market might be rewarding, this is a great moment to broaden your search and discover fast growing stocks with high insider ownership

With shares trading close to analyst targets and recent growth moderating, the big question is whether Informatica now represents an undervalued opportunity or if the market has already accounted for its future potential.

The narrative consensus suggests Informatica’s fair value is in line with the current share price, with only a marginal gap separating analyst targets and market price. This equilibrium reflects subdued expectations for wild valuation swings in the near term, making the following key narrative driver stand out even more.

Informatica's innovations, such as its AI-powered IDMC platform with CLAIRE AI and GenAI capabilities, are expected to capture a significant portion of the $62 billion addressable cloud market. This could potentially increase future revenue and earnings. Informatica's expansion in AI capabilities, with an increase in AI-driven use cases and AI blueprints with major tech partners, is expected to enhance revenue growth by driving the adoption of data management platforms.

Curious what bold assumptions power this fair value? The real story lies in growth upgrades, rapidly rising margins, and ambitious profit forecasts that most would not expect. How do analysts justify their price target with high growth multiples and future earnings leaps? Click to see what numbers drive the narrative’s fair value and what could surprise the market next.

Result: Fair Value of $24.40 (ABOUT RIGHT)

However, lower-than-expected renewals and foreign exchange headwinds could quickly undermine these fair value assumptions. This signals possible setbacks for Informatica's growth story.

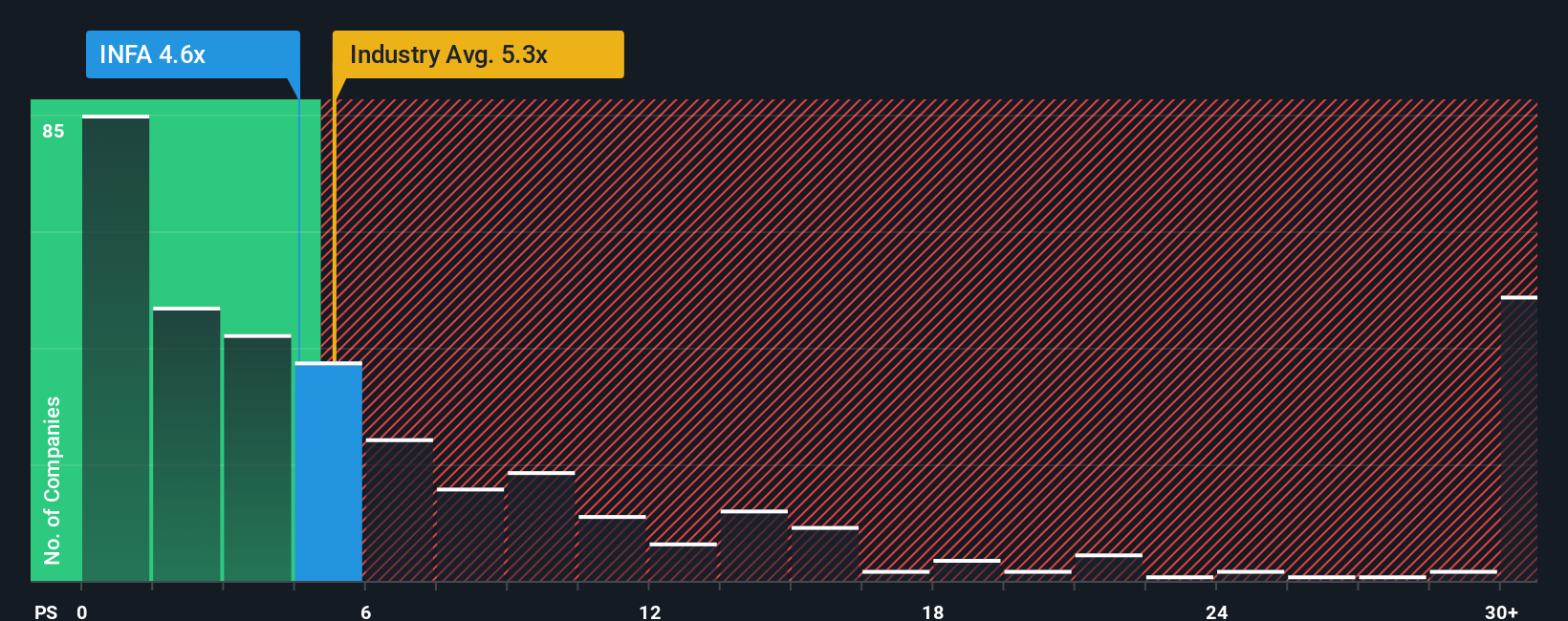

Looking through a different lens, Informatica’s price-to-sales ratio stands at 4.6x. This is noticeably lower than both its peer average of 6.9x and the US software industry’s 5.3x. The fair ratio, calculated at 5.5x, suggests the stock could move higher if sentiment shifts. Are investors overlooking a potential value or pricing in more risk than meets the eye?

If you see the story unfolding differently or want a hands-on look at the numbers, you can craft your own narrative in just a few minutes, your way. Do it your way

A great starting point for your Informatica research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Don’t let your next big win slip away. Expand your watchlist now with bold opportunities you can spot instantly using Simply Wall Street’s powerful tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.