هل حان الوقت لإعادة تقييم شركة DXP Enterprises (DXPE) بعد قوة سعر السهم الأخيرة؟

DXP Enterprises, Inc. DXPE | 159.37 | +5.44% |

- إذا كنت تتساءل عما إذا كان سعر سهم شركة DXP Enterprises الحالي يعكس قيمتها الحقيقية، فأنت لست وحدك. تشرح هذه المقالة ما تشير إليه الأرقام فعلياً.

- مع وصول سعر السهم إلى 132.09 دولارًا أمريكيًا وعوائد حديثة بلغت 9.4% على مدى 7 أيام، و14.4% على مدى 30 يومًا، و22.6% منذ بداية العام، و23.4% على مدى عام واحد، يعيد العديد من المستثمرين تقييم كل من إمكانات النمو ومستوى المخاطر التي يشعرون بالراحة تجاهها.

- حظيت شركة DXP Enterprises باهتمام إعلامي واسع لدورها كموزع ومزود خدمات في مختلف الأسواق الصناعية. وقد ساهم ذلك في إبقاء سهم الشركة محط أنظار المستثمرين مع تغير الظروف التي تواجه شركات السلع الرأسمالية. وتوفر التغطية المستمرة لاتجاهات الطلب في القطاع والتحديثات الخاصة بالشركة سياقًا هامًا عند التفكير في مدى استدامة أداء سعر السهم الأخير.

- في تقييماتنا، حصلت شركة DXP Enterprises على 3 من 6 نقاط في مؤشر احتمال انخفاض قيمتها، ويمكنكم الاطلاع على تفاصيل هذه النتيجة هنا . سنقارن لاحقًا بين مناهج تقييم مختلفة للسهم، ثم نختتم بنظرة على القيمة تتجاوز النسب المعتادة.

النهج الأول: تحليل التدفقات النقدية المخصومة لشركة DXP

يأخذ نموذج التدفقات النقدية المخصومة التدفقات النقدية المستقبلية المتوقعة ثم يخصمها إلى اليوم باستخدام معدل العائد المطلوب لتقدير قيمة الشركة في الوقت الحالي.

بالنسبة لشركة DXP Enterprises، يستخدم النموذج منهجية التدفق النقدي الحر إلى حقوق الملكية على مرحلتين. يبلغ التدفق النقدي الحر خلال الاثني عشر شهرًا الماضية حوالي 61 مليون دولار. وتشير توقعات المحللين والتوقعات المستنبطة إلى أن التدفق النقدي الحر سيصل إلى حوالي 206.8 مليون دولار في عام 2035، مع تقديرات محددة مثل 106.6 مليون دولار في عام 2026 و159.6 مليون دولار في عام 2029، وكلها بالدولار الأمريكي. وتقوم منصة Simply Wall St باستنباط البيانات لما بعد أفق المحللين لإكمال مسار العشر سنوات.

عند خصم جميع التدفقات النقدية المستقبلية وجمعها، يصل النموذج إلى قيمة جوهرية تبلغ حوالي 171.38 دولارًا أمريكيًا للسهم الواحد. وبالمقارنة مع سعر السهم الحالي البالغ حوالي 132.09 دولارًا أمريكيًا، فإن هذا يشير إلى خصم بنسبة 22.9%، مما يدل على أن الأسهم تُتداول بأقل من تقدير التدفقات النقدية المخصومة.

النتيجة: مُقَيَّم بأقل من قيمته الحقيقية

تشير تحليلاتنا للتدفقات النقدية المخصومة (DCF) إلى أن أسهم شركة DXP Enterprises مقومة بأقل من قيمتها الحقيقية بنسبة 22.9%. تابع هذا السهم في قائمة مراقبتك أو محفظتك الاستثمارية ، أو اكتشف 878 سهماً آخر مقوماً بأقل من قيمته الحقيقية بناءً على التدفقات النقدية .

النهج الثاني: مقارنة سعر سهم شركة DXP Enterprises مع أرباحها

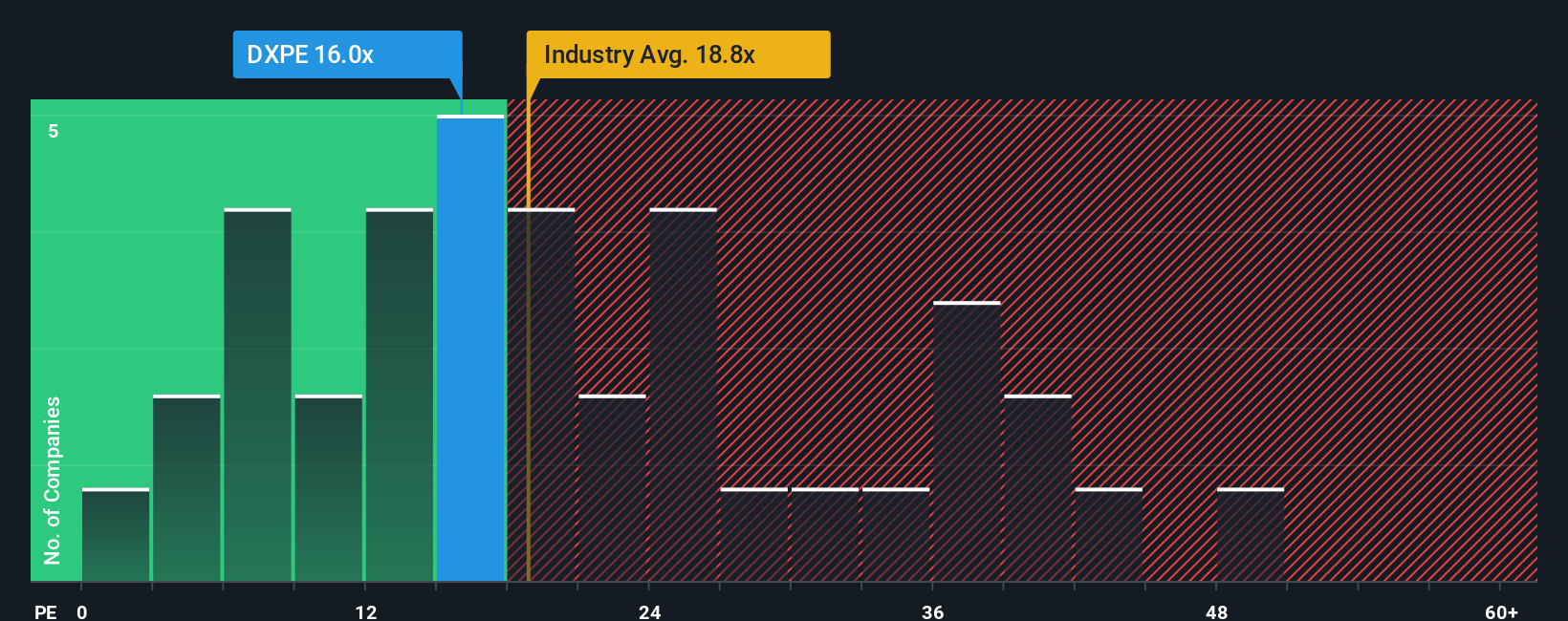

بالنسبة للشركات المربحة، يُعدّ مُضاعف الربحية (P/E) أداةً مفيدةً لفهم العائد على الاستثمار لكل دولار من الأرباح. عادةً ما تدعم توقعات النمو المرتفعة وانخفاض المخاطر المُتصوَّرة مُضاعف ربحية أعلى، بينما يُبرر النمو الأبطأ أو المخاطر الأعلى مُضاعف ربحية أقل.

تتداول أسهم شركة DXP Enterprises حاليًا بنسبة سعر إلى ربحية تبلغ 23.8 ضعفًا. وهذا قريب من متوسط قطاع موزعي التجارة البالغ حوالي 23.9 ضعفًا، وأعلى من متوسط المجموعة النظيرة البالغ 19.5 ضعفًا، لذا فإن السهم ليس رخيصًا جدًا ولا باهظ الثمن جدًا عند المقارنة البسيطة.

كما تُحسب منصة Simply Wall St نسبة "القيمة العادلة" الخاصة بشركة DXP Enterprises، والتي تبلغ 26.0 ضعفًا. وهي تقدير لما قد تكون عليه نسبة السعر إلى الأرباح إذا عكس السوق بشكل كامل عوامل مثل معدل نمو أرباح الشركة، وهوامش الربح، والقطاع، والقيمة السوقية، والمخاطر الرئيسية. ونظرًا لأنها تتضمن هذه العوامل الخاصة بالشركة، فإن نسبة القيمة العادلة تُقدم معيارًا أكثر دقة من المتوسطات العامة للقطاع أو الشركات المنافسة.

تشير مقارنة نسبة السعر إلى الأرباح الحالية البالغة 23.8 مرة مع النسبة العادلة البالغة 26.0 مرة إلى أن الأسهم يتم تداولها بأقل من هذا المعيار المخصص.

النتيجة: مُقَيَّم بأقل من قيمته الحقيقية

نسبة السعر إلى الأرباح لا تُعطي صورة كاملة، ولكن ماذا لو كانت الفرصة الحقيقية تكمن في مكان آخر؟ اكتشف 1427 شركة يراهن فيها المطلعون بقوة على نمو هائل .

حسّن عملية اتخاذ القرارات لديك: اختر سردية مؤسستك الخاصة بمنصة تجربة العملاء الرقمية

ذكرنا سابقاً أن هناك طريقة أفضل لفهم التقييم، لذا دعونا نقدم لكم "الروايات"، وهي طريقة بسيطة لربط وجهة نظرك حول DXP Enterprises بالأرقام التي تراها على الشاشة.

السرد هو قصتك عن الشركة، معبراً عنها من خلال افتراضات القيمة العادلة والإيرادات المستقبلية والأرباح وهوامش الربح، وبالتالي فهو يحول الأفكار غير المنظمة إلى رؤية منظمة.

في موقع Simply Wall St، تربط الروايات تلك القصة بتوقعات مالية ثم بالقيمة العادلة، ويمكنك الوصول إليها مباشرة على صفحة المجتمع حيث يشارك ملايين المستثمرين وجهات نظرهم.

بمجرد حصولك على سرد، يمكنك مقارنة قيمته العادلة بالسعر الحالي للمساعدة في تحديد ما إذا كانت شركة DXP Enterprises تبدو جذابة أم مبالغ فيها بناءً على افتراضاتك الخاصة، ويستمر السرد في التحديث عند إضافة أرباح أو أخبار أو بيانات أخرى جديدة.

على سبيل المثال، قد يعكس أحد سرديات DXP Enterprises على صفحة المجتمع قيمة عادلة متفائلة للغاية مع نمو أعلى في الإيرادات وهوامش ربح أعلى، بينما قد يستخدم سرد آخر افتراضات أكثر تحفظًا، مما يؤدي إلى قيمة عادلة أقل.

هل تعتقد أن هناك المزيد من التفاصيل حول شركة DXP Enterprises؟ تفضل بزيارة مجتمعنا للاطلاع على آراء الآخرين!

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.