يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Olin’s (OLN) Braskem Partnership and EDC Realignment Could Be a Game Changer

Olin Corporation OLN | 23.80 | +1.84% |

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

To be a shareholder in Olin today, you need to believe in the long-term earnings power of its integrated chemical platform and the ability to reposition supply into more profitable and sustainable partnerships, despite severe pricing pressure in global EDC markets and persistent overcapacity. The recent Braskem alliance is a positive step for Olin’s vinyls strategy, but its impact on the most important near-term catalyst, industry-wide cost rationalization, remains modest, and it does not meaningfully address the biggest risk of prolonged low EDC prices.

Among recent announcements, the winding down of the Blue Water Alliance joint venture stands out. This move freed up EDC volumes, allowing Olin to pursue the higher-value Braskem partnership and focus more intently on long-term, growth-oriented contracts rather than short-term commodity exposures, which speaks directly to the catalysts discussed above. Contrast this more optimistic setup with...

Olin's outlook projects $7.4 billion in revenue and $375.3 million in earnings by 2028. This requires a 3.6% annual revenue growth rate and an earnings increase of $389.4 million from the current earnings of -$14.1 million.

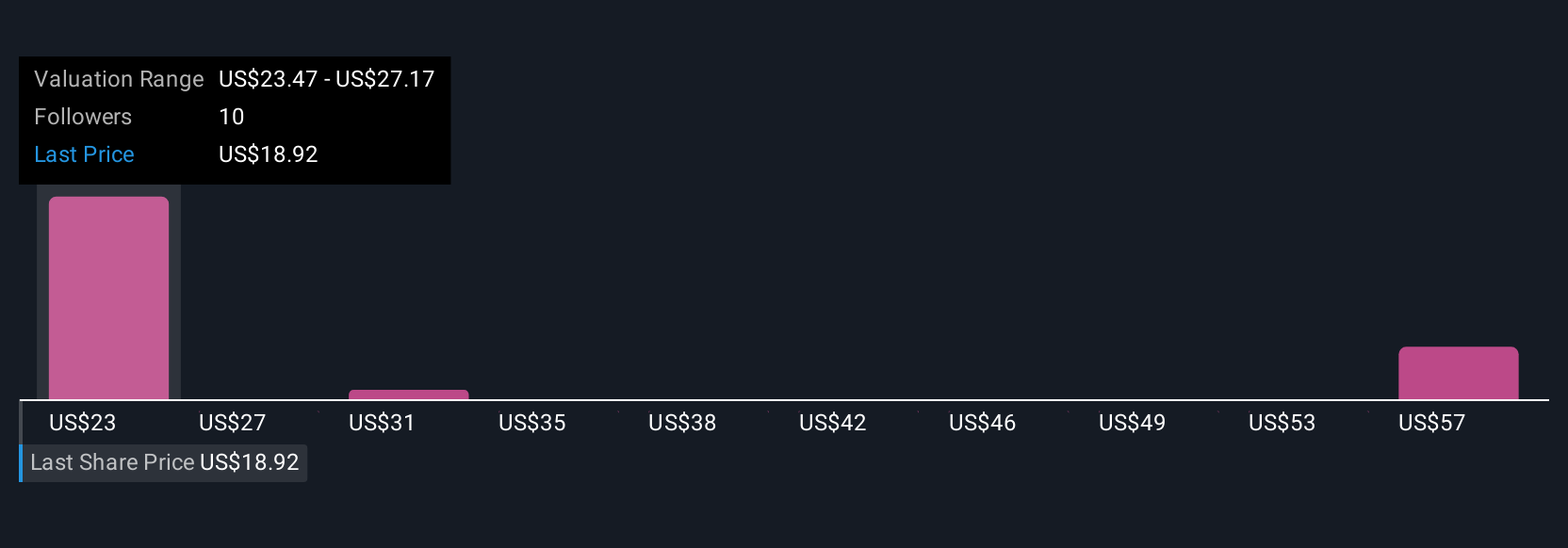

Uncover how Olin's forecasts yield a $24.73 fair value, a 23% upside to its current price.

Five community fair value estimates on Simply Wall St for Olin range from US$24.73 to US$105.17, revealing a broad spectrum of opinions on the stock. While some expect upside if cost-cutting succeeds, others flag the risk that prolonged low EDC prices could limit recovery, making it worthwhile to explore several different viewpoints.

Explore 5 other fair value estimates on Olin - why the stock might be worth over 5x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.