يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Sonic Automotive (NYSE:SAH) Has No Shortage Of Debt

Sonic Automotive, Inc. Class A SAH | 66.63 | +3.25% |

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Sonic Automotive, Inc. (NYSE:SAH) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

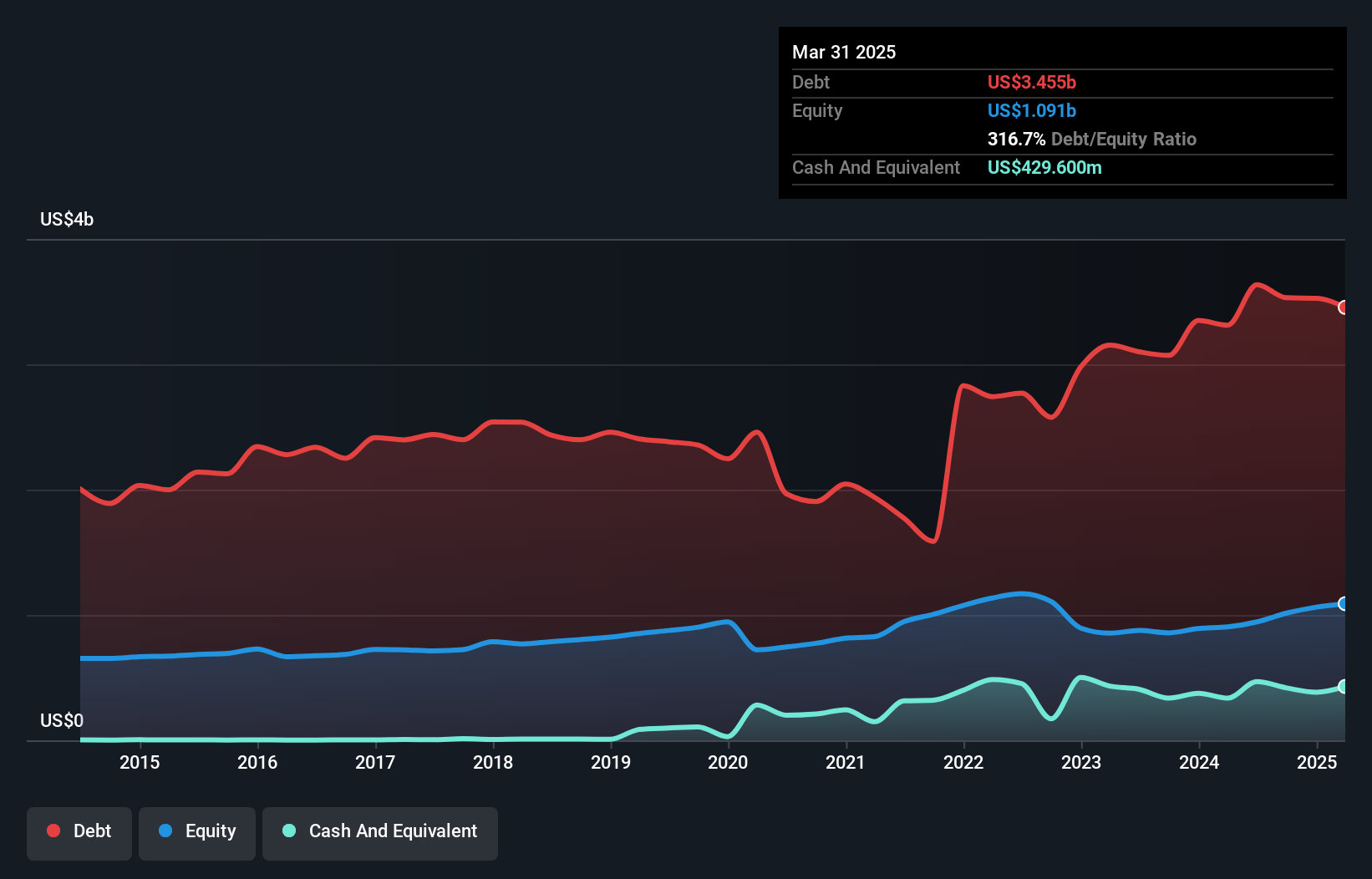

The image below, which you can click on for greater detail, shows that at March 2025 Sonic Automotive had debt of US$3.45b, up from US$3.31b in one year. However, it does have US$429.6m in cash offsetting this, leading to net debt of about US$3.03b.

According to the last reported balance sheet, Sonic Automotive had liabilities of US$2.63b due within 12 months, and liabilities of US$2.16b due beyond 12 months. Offsetting this, it had US$429.6m in cash and US$514.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.84b.

This deficit casts a shadow over the US$2.38b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Sonic Automotive would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Sonic Automotive's debt to EBITDA ratio (4.9) suggests that it uses some debt, its interest cover is very weak, at 2.4, suggesting high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Even more troubling is the fact that Sonic Automotive actually let its EBIT decrease by 3.8% over the last year. If it keeps going like that paying off its debt will be like running on a treadmill -- a lot of effort for not much advancement. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Sonic Automotive can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Sonic Automotive created free cash flow amounting to 9.7% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Mulling over Sonic Automotive's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. But at least its EBIT growth rate is not so bad. Taking into account all the aforementioned factors, it looks like Sonic Automotive has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.