لماذا انخفض سهم شركة دبليو دبليو غرينجر (GWW) بنسبة 5.5% بعد نتائج متباينة لعام 2025، وتوقعات لعام 2026، ودعوى قضائية جديدة؟

غرينجر دبليو دبليو إنك GWW | 1133.52 1133.52 | -0.86% 0.00% Post |

- أعلنت شركة WW Grainger, Inc. مؤخرًا عن نتائج الربع الرابع من عام 2025 والتي أظهرت مبيعات بقيمة 4,425 مليون دولار أمريكي ومبيعات كاملة لعام 2025 بقيمة 17.94 مليار دولار أمريكي، إلى جانب إصدار توجيهات صافي المبيعات لعام 2026 تتراوح بين 18.70 مليار دولار أمريكي و19.10 مليار دولار أمريكي، في حين تواجه أيضًا دعوى قضائية جماعية جديدة من كاليفورنيا تتعلق بالعمالة تزعم انتهاكات الأجور وساعات العمل.

- على الرغم من ارتفاع المبيعات، انخفض صافي دخل الشركة وأرباح السهم الواحد من العمليات المستمرة في عام 2025، مما يسلط الضوء على الضغط على الربحية مع استثمارها في التكنولوجيا وتوسيع تشكيلة المنتجات والمبادرات التشغيلية.

- في ظل هذه الخلفية المتمثلة في ارتفاع المبيعات وانخفاض الأرباح، سنقوم بدراسة كيف تعيد توجيهات مبيعات شركة Grainger لعام 2026 تشكيل سردها الاستثماري الحالي.

اكتشف الفرصة الكبيرة القادمة مع 28 سهمًا من أسهم البنسات المميزة التي توازن بين المخاطرة والعائد.

ملخص سردية استثمار دبليو دبليو غرينجر

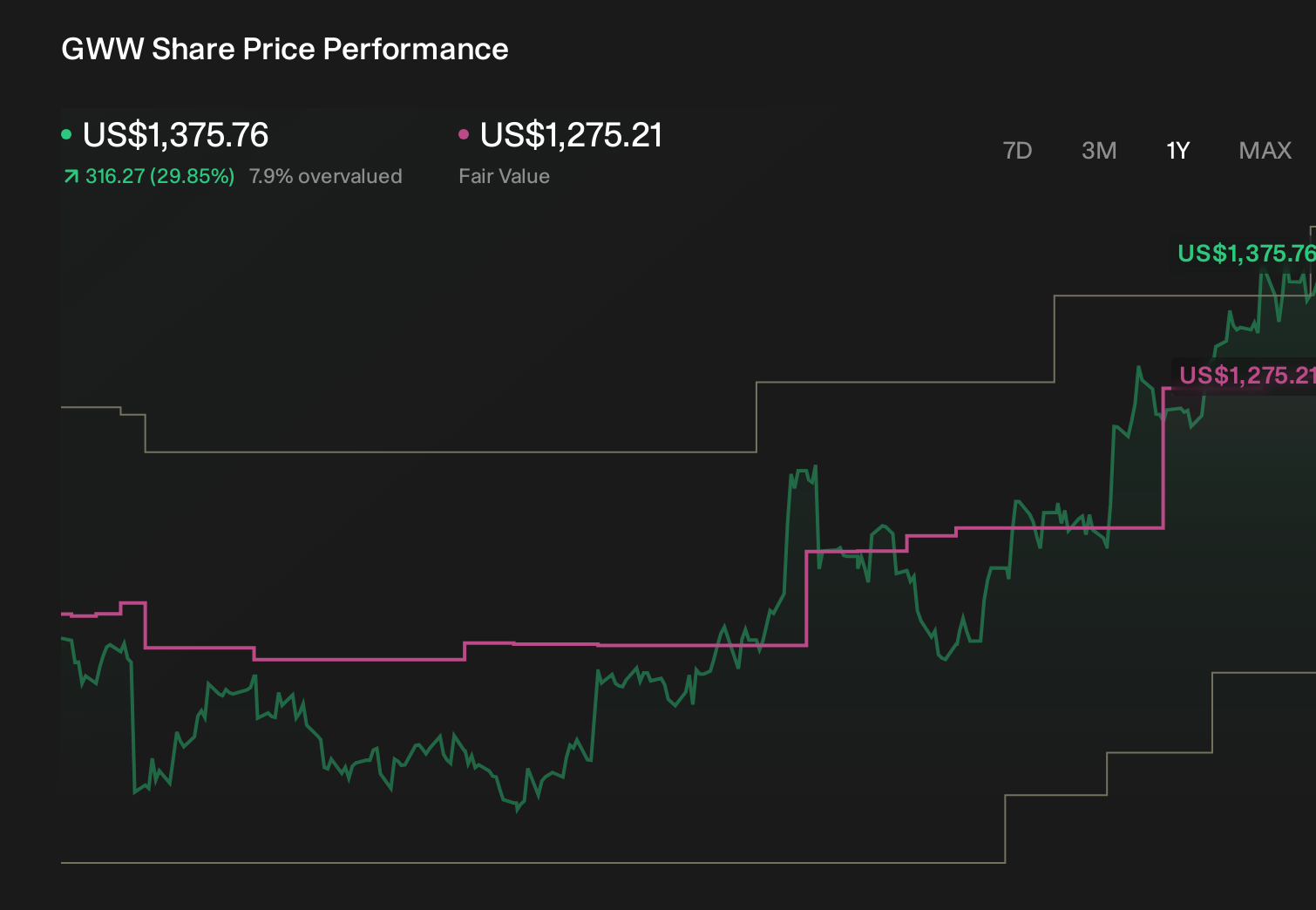

لامتلاك أسهم شركة Grainger، يجب أن تؤمن بقدرة حجمها وأدواتها الرقمية وتشكيلتها الواسعة على تعويض ضغوط هوامش الربح الناتجة عن انخفاض الأرباح وارتفاع التكاليف المستمر. تؤكد أحدث نتائج عام 2025 وتوقعات مبيعات عام 2026 نمو الإيرادات، ولكن مع انخفاض الربحية، لذا يبقى العامل المحفز الرئيسي على المدى القريب هو ما إذا كانت الاستثمارات في التكنولوجيا وتشكيلة المنتجات ستُحسّن هوامش الربح. تُضيف الدعوى الجماعية العمالية الجديدة في كاليفورنيا حالة من عدم اليقين القانوني والمالي، ولكن في هذه المرحلة، لا يبدو أنها تُغيّر الفرضية الأساسية.

أهم ما تم الإعلان عنه مؤخرًا هو توقعات شركة غراينجر لمبيعاتها الصافية لعام 2026، والتي تتراوح بين 18.70 مليار دولار أمريكي و19.10 مليار دولار أمريكي، ما يُرسي دعائم التوقعات بعد عام شهد ارتفاعًا في المبيعات وانخفاضًا في الأرباح. بالنسبة للمستثمرين، يُحدد هذا النطاق مدى سرعة نمو الشركة، وفقًا لتوقعات الإدارة، بالإضافة إلى مبيعات عام 2025 البالغة 17.94 مليار دولار أمريكي، وذلك في ظل ضغوط على هوامش الربح، واستمرار النفقات الرأسمالية، فضلًا عن التحديات القانونية الناشئة التي قد تؤثر على التكاليف والمخاطر الإعلامية.

ومع ذلك، فإنه بالرغم من التوقعات المرتفعة للمبيعات لعام 2026، فإن قضية الأجور وساعات العمل غير المحسومة في كاليفورنيا تشكل خطراً يجب على المستثمرين أن يكونوا على دراية به...

تتوقع شركة WW Grainger تحقيق إيرادات بقيمة 21.3 مليار دولار وأرباح بقيمة 2.3 مليار دولار بحلول عام 2028. ويتطلب ذلك نموًا سنويًا في الإيرادات بنسبة 6.7٪ وزيادة في الأرباح بنحو 0.4 مليار دولار من 1.9 مليار دولار اليوم.

اكتشف كيف أن توقعات شركة WW Grainger تُنتج قيمة عادلة قدرها 1131 دولارًا ، بما يتماشى مع سعرها الحالي.

استكشاف وجهات نظر أخرى

بينما يركز الإجماع على ضغط الهامش والمخاطر القانونية، كان المحللون الأكثر تفاؤلاً يتوقعون سابقًا إيرادات تبلغ حوالي 21.5 مليار دولار أمريكي وأرباحًا تبلغ 2.4 مليار دولار أمريكي، لذلك إذا كنت توازن بين هذه التوقعات المتفائلة والتوجيهات الجديدة ومخاوف تكلفة العمالة، فمن الجدير بالذكر مدى اختلاف الآراء وكيف قد تحتاج كلتا الروايتين إلى إعادة النظر بعد هذه الأخبار.

استكشف 3 تقديرات أخرى للقيمة العادلة لشركة WW Grainger - لماذا قد تكون قيمة السهم أقل بنسبة 16٪ من السعر الحالي!

ابتكر قصتك الخاصة مع دبليو دبليو غرينجر

هل تخالف الروايات السائدة؟ أنشئ روايتك الخاصة في أقل من 3 دقائق - نادراً ما تأتي عوائد الاستثمار الاستثنائية من اتباع القطيع.

- تُعد نقطة انطلاق رائعة لبحثك في شركة WW Grainger هي تحليلنا الذي يسلط الضوء على مكافأة رئيسية واحدة وعلامة تحذيرية مهمة واحدة يمكن أن تؤثر على قرارك الاستثماري.

- يقدم تقريرنا البحثي المجاني عن شركة WW Grainger تحليلاً أساسياً شاملاً مُلخصاً في شكل مرئي واحد - شكل ندفة الثلج - مما يسهل تقييم الوضع المالي العام لشركة WW Grainger بنظرة سريعة.

هل ترغب بمعرفة المزيد من الخيارات؟

بدأ المستثمرون الأوائل يلاحظون ذلك بالفعل. تعرف على الأسهم التي يستهدفونها قبل أن تغادر السوق:

- ابحث عن 53 شركة ذات إمكانات تدفق نقدي واعدة ولكنها تتداول بأقل من قيمتها العادلة .

- استغل دورة البنية التحتية للذكاء الاصطناعي الفائقة من خلال اختيارنا لأفضل 34 "خيارًا وأداة" في طفرة الذكاء الاصطناعي التي تحول الطلب القياسي إلى تدفق نقدي هائل.

- مستقبل العمل هنا. اكتشف أفضل 30 سهماً في مجال الروبوتات والأتمتة التي تقود مسيرة الأتمتة المدعومة بالذكاء الاصطناعي والتحول الصناعي.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.