يرجى استخدام متصفح الكمبيوتر الشخصي للوصول إلى التسجيل - تداول السعودية

حسنًا

Zillow Group (ZG): Evaluating Valuation Following Latest Earnings and Share Price Pullback

Zillow Group, Inc. Class A ZG | 42.15 | +3.28% |

Zillow Group (ZG) shares have dropped about 2% today after the company reported annual net income figures that showed a loss of $32 million, even though revenue climbed over the past year. Investors are considering what this means for Zillow’s ongoing shift in the real estate technology space.

While today’s dip follows weaker-than-expected profitability, it’s the broader trend that stands out: Zillow’s share price is now down 4.1% for the year-to-date and 4.98% on a total return basis over the past year, suggesting momentum has faded after a strong multiyear rebound. Recall that the three-year total shareholder return still sits at an impressive 93% despite current challenges.

If you’re weighing up what else the market has to offer, now’s a good moment to explore and discover fast growing stocks with high insider ownership

The question now is whether Zillow’s recent pullback, combined with a sizable analyst price target discount and ongoing revenue growth, leaves the stock undervalued. Alternatively, investors may need to be cautious that the market has already accounted for future gains.

With Zillow Group’s fair value pegged at $88.46 compared to the last close of $67.21, the prevailing narrative points to significant upside potential if management can meet ambitious targets in a rapidly evolving digital real estate market.

The accelerated digital transformation of real estate, combined with Zillow’s leading traffic, engagement, and product innovation (including AI-powered tools, integrated communication platforms such as Follow Up Boss, and immersive experiences like SkyTour), positions the company to expand market share and drive higher user conversion rates. This is likely to result in above-industry revenue growth and higher monetization per transaction.

Want to know the surprising growth levers justifying such a premium? Discover how cutting-edge product launches and aggressive margin expansion shape this high-conviction valuation. The real story is in the ramp-up assumptions driving revenue and profits in the years ahead. Are you ready to see what Wall Street is betting on?

Result: Fair Value of $88.46 (UNDERVALUED)

However, persistent high interest rates and regulatory pressures could still limit real estate transaction volumes. This could potentially challenge Zillow’s optimistic growth trajectory.

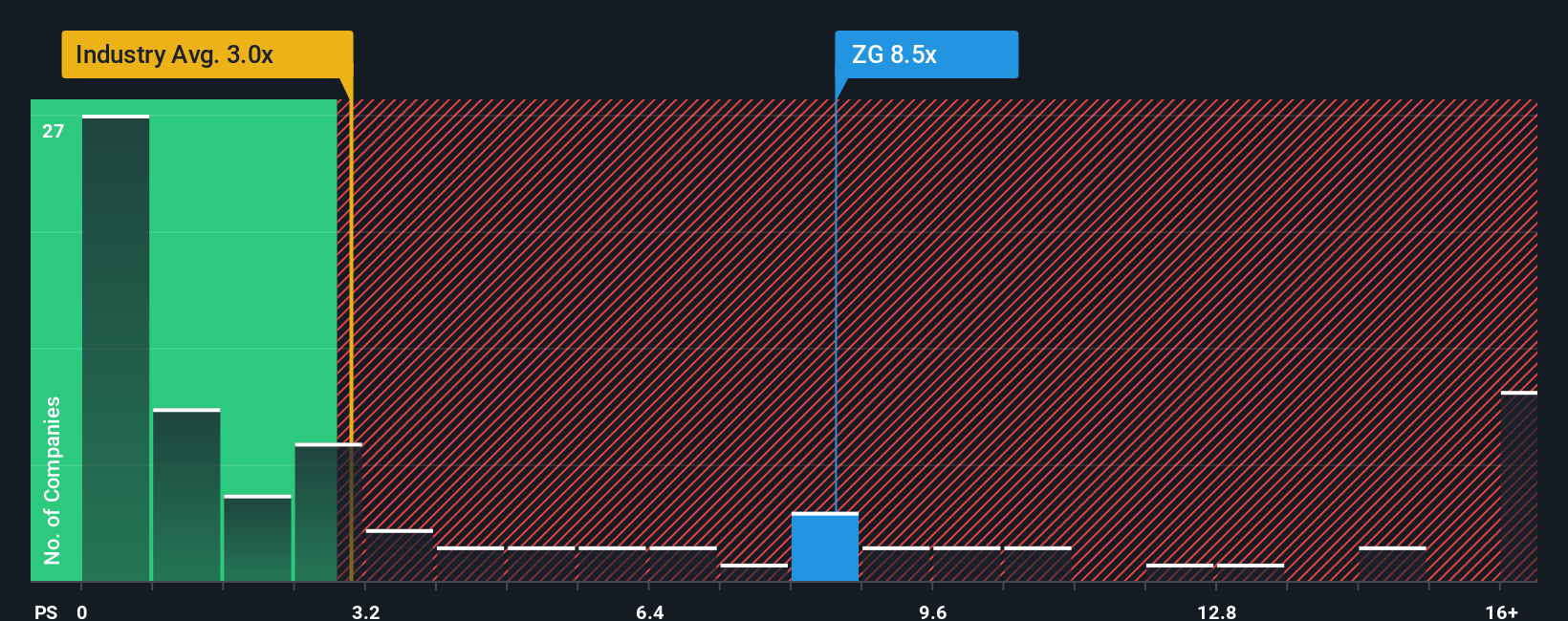

While the fair value model points to sizable upside, Zillow’s price-to-sales ratio is sitting at 6.6x. This is much higher than both the industry average of 2.6x and its peer group at 3.1x. The market’s willingness to pay such a premium may hint at elevated expectations, but it also raises valuation risk. Could sentiment shift if growth slows?

If you see things differently or want to dig into the numbers yourself, it’s easy to develop your own point of view in just minutes, and Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Zillow Group.

Level up your investing strategy and uncover opportunities you might be missing. Search the market for unique angles and hidden gems using these powerful screeners:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.