3 Defensive Stocks For Investors Worried About A 5% S&P 500 Pullback

U.S. Physical Therapy, Inc. USPH | 0.00 |

With Bank of America flagging rich valuations, stretched AI spending, and the prospect of more Fed rate hikes, many investors are starting to question how much risk sits inside broad market indices. Defensive stocks, particularly larger companies with steady dividends and healthier balance sheets, can sometimes feel less exposed when momentum trades unwind or volatility spikes. This article looks at how those macro catalysts could affect a handful of resilient businesses and why their profiles might appeal if a 5% S&P 500 snapback materialises. Ahead, three stocks from a Defensive Stocks screener are put under the microscope.

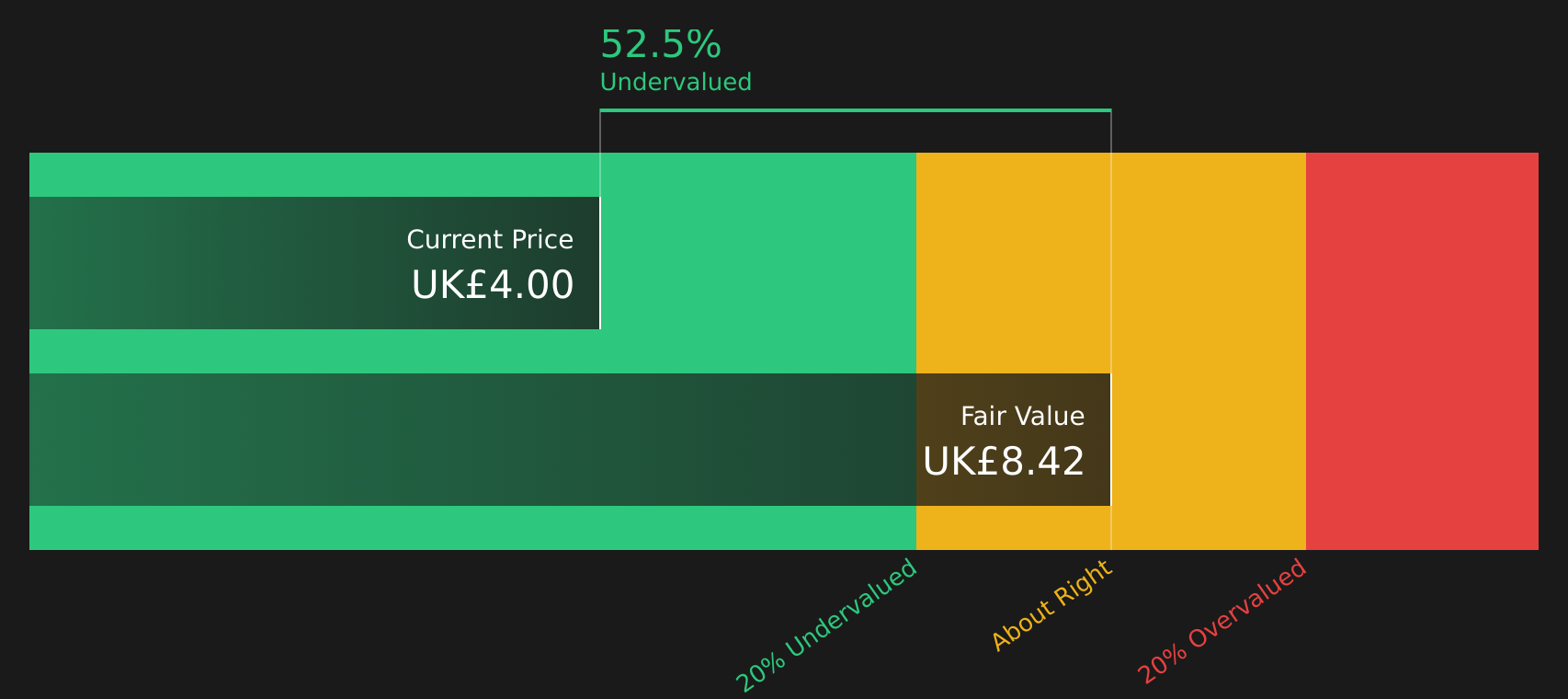

Tristel (AIM:TSTL)

Overview: Tristel is a UK based infection prevention specialist that makes and sells high level disinfectants for hospital medical devices, clinical surfaces and laboratories, with a product range that covers areas such as endoscopy, ultrasound, ophthalmology and women’s health.

Operations: Tristel generates most of its £49.5m revenue from Hospital Medical Device Decontamination (£43.4m), with smaller contributions from Hospital Environmental Surface Disinfection (£4.3m) and Other Revenue (£1.9m) across the UK, Western Europe, Germany, Australia and other regions.

Market Cap: £192.0m

Tristel operates in a market where investors are increasingly wary of stretched valuations and rate sensitive growth stories, because demand for hospital disinfection products often reflects healthcare needs rather than market cycles. The stock is priced below one valuation estimate of fair value and carries a P/E below sector peers. This may appeal to investors who prefer steadier cash generative businesses. Earnings growth forecasts are described as solid, return on equity is high and the company has regulatory progress that could support further international expansion. Set against this are pressure points, including an unstable dividend record, a higher reliance on external funding and leadership change at the top that could reshape execution in unpredictable ways.

Tristel’s mix of healthcare linked demand, a below sector P/E and a single valuation estimate above the share price raises an obvious question about what the market might be missing, and the DCF valuation analysis for Tristel could reveal the twist behind that gap

U.S. Physical Therapy (USPH)

Overview: U.S. Physical Therapy operates and manages outpatient physical therapy clinics across the U.S., treating orthopedic and sports injuries, supporting patients before and after surgery, and helping injured workers and people with neurological conditions return to function. It also provides onsite injury prevention, testing, and ergonomics services for large employers, insurers, and their contractors.

Operations: U.S. Physical Therapy generates the bulk of its US$787.7m revenue from Physical Therapy Operations at US$670.2m, with Industrial Injury Prevention Services contributing US$117.5m, all in the United States.

Market Cap: US$1.1b

U.S. Physical Therapy stands out in a market where investors are focused on stretched AI valuations and higher rates because its clinics and employer services are tied more directly to essential healthcare demand rather than speculative tech spending. The company is using acquisitions, such as a recent twelve clinic deal that expands its presence into 45 states, and a larger US$450m credit facility to build scale, even as profit margins sit at 1% and earnings have recently fallen. That mix of growth plans, a 2.54% dividend and high analyst expectations for future earnings creates an interesting tension between potential upside and risks related to reimbursement pressure, labor costs and a high current P/E. The analysis report for U.S. Physical Therapy examines how those factors fit together.

U.S. Physical Therapy is leaning into acquisitions and a bigger credit facility while profits stay thin and expectations stay high, and the full story sits inside the analysis report for U.S. Physical Therapy

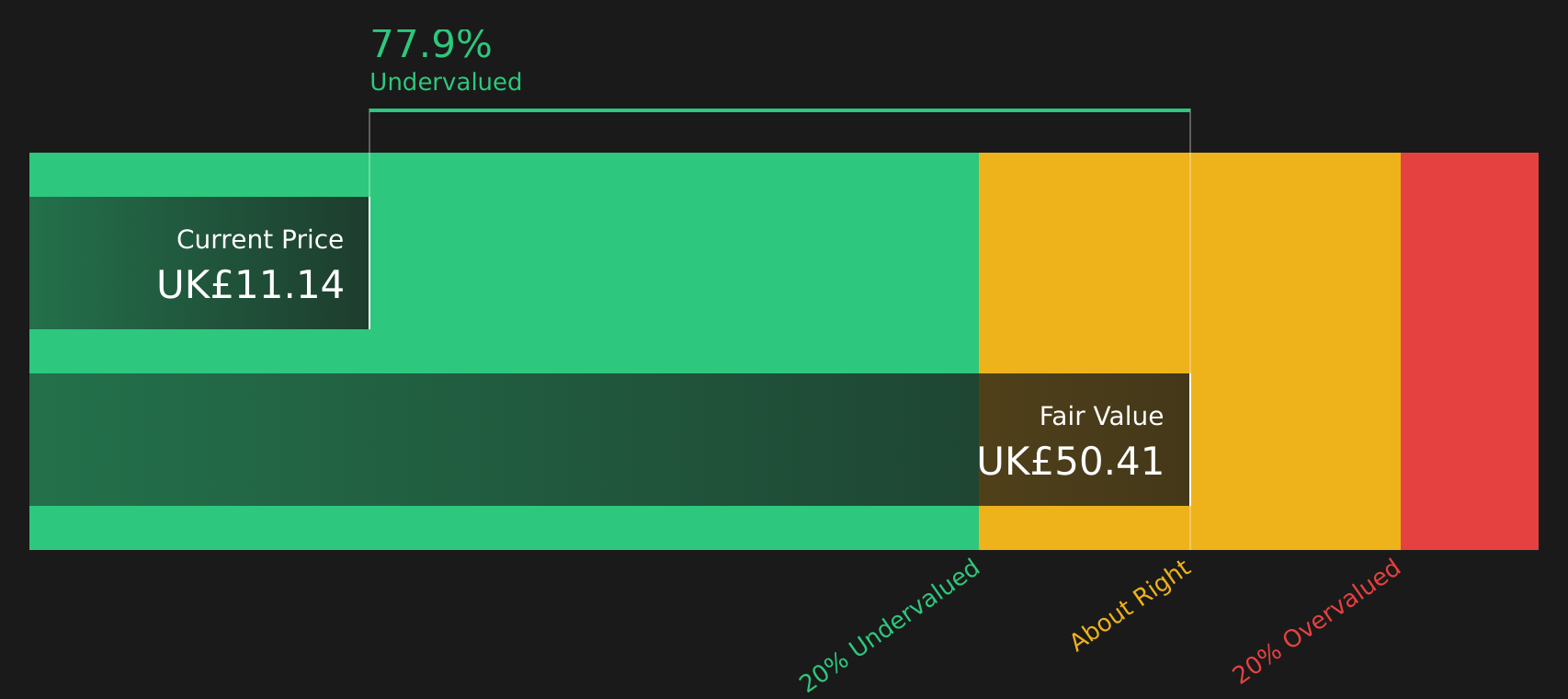

Craneware (AIM:CRW)

Overview: Craneware is a UK based software company that sells data driven SaaS tools to U.S. hospitals, helping them manage pricing, billing, pharmacy operations and workforce productivity so they can improve revenue integrity and control administrative costs.

Operations: Craneware generates its entire US$211.3m of revenue from healthcare software sold into the United States.

Market Cap: £366.5m

Craneware sits at the intersection of hospital cost pressure and the need for reliable, cloud based data tools. Its Trisus platform, multi decade customer relationships and AI assisted features are attracting attention in a market that is nervous about speculative growth stories. Earnings recently grew faster than revenue, margins improved to 10.6% and the stock is described as trading well below one estimate of fair value. However, guidance for broadly flat FY26 revenue and a dividend that is not covered by free cash flow highlight that execution and funding choices still matter. For investors considering defensive healthcare software with recurring revenue, U.S. exposure and valuation support as AI hype cools, Craneware may warrant a closer look.

Craneware’s earnings and margin lift, together with a share price described as well below one fair value estimate, suggest something in the story is still underappreciated. The DCF valuation analysis for Craneware hints at what might be hiding in plain sight

The three defensive stocks in this article are just a starting point. The full Defensive Stocks screener surfaces 12 more companies that pair solid financial health with dividend histories and lower risk profiles that could suit choppy markets. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you, so you can focus on the highest conviction defensive opportunities rather than sorting through the entire index yourself.

Take Control of Your Investment Journey

If U.S. Physical Therapy or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

New ideas move fast, and the best breakout setups rarely stay under the radar for long. Before the crowd catches on and momentum is gone, consider positioning earlier.

- Target high-yield income plays that aim to keep paying even when sentiment cools by scanning our curated 3 dividend fortresses before yield hunters crowd in.

- Spot early movers tied to copper demand trends as infrastructure spending shifts by reviewing a hand picked 8 top copper producer stocks while the story is still developing.

- Track companies building the backbone of tomorrow’s AI hardware and networking by tapping into a focused 52 AI infrastructure stocks before attention really accelerates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.