3 Defensive Value Stocks With Dividends And Fair Value Gaps

Global markets have been shaken by a sharp tech-led selloff, with double-digit falls in South Korea’s Kospi and steep drops across European chip stocks and U.S. semiconductor giants. When fast-growing sectors are under pressure, investors often look more closely at companies with steadier cash flows, stronger balance sheets, and consistent dividends. This is where a Defensive Value Stocks screener can help by focusing attention on stocks that may offer some resilience during volatility. Below, the article will walk through 3 stocks from this list that appear more exposed to the current news-driven moves in markets.

Village Super Market (VLGE.A)

Overview: Village Super Market operates ShopRite, Fairway and Gourmet Garage supermarkets and specialty food stores in the U.S., selling a full range of groceries, prepared foods and household products, both in-store and through its branded websites and apps.

Operations: Village Super Market generates about US$2.4b in annual revenue from the retail sale of food and nonfood products in the United States.

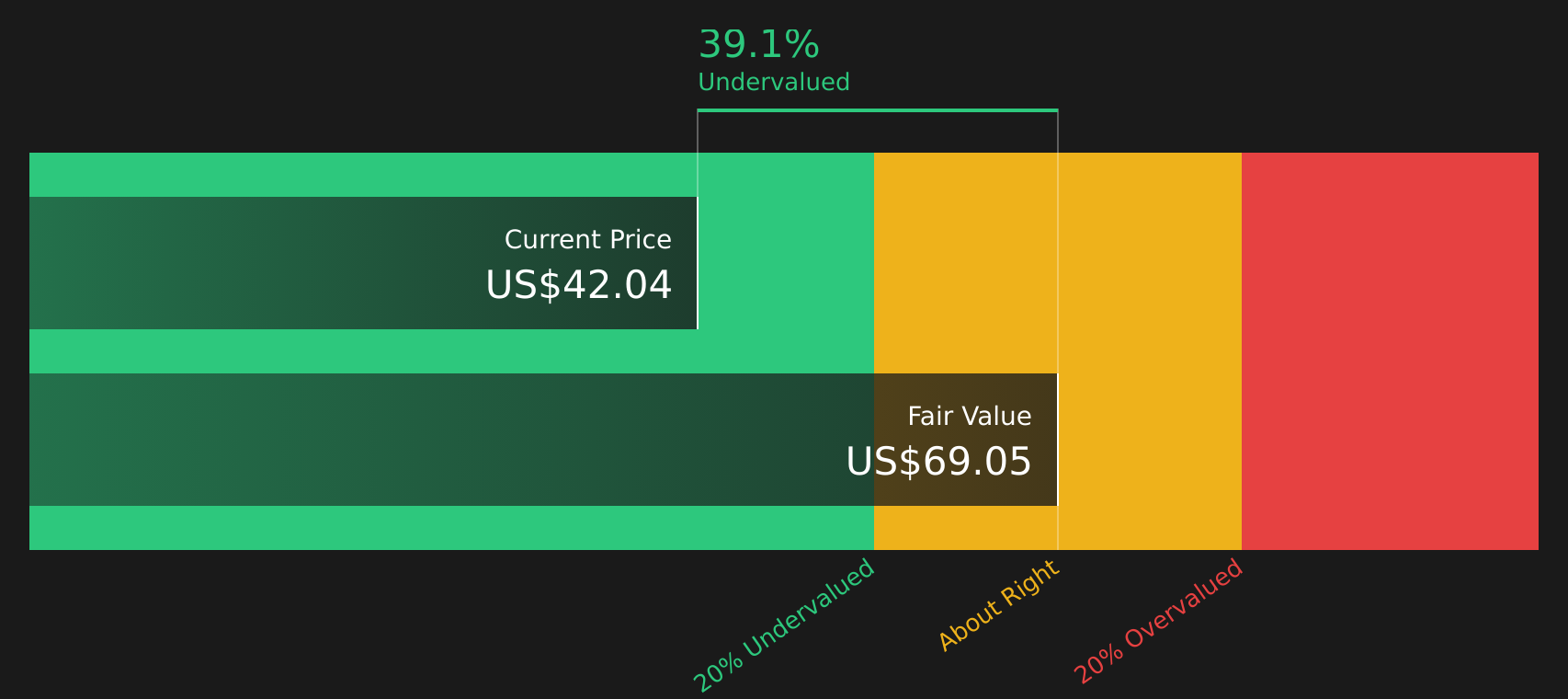

Market Cap: US$603m

Village Super Market attracts attention in a tech-led selloff because it sits firmly in consumer staples, with supermarket spending often holding up when growth stocks are under pressure, and it also offers a 2.45% dividend yield. The stock screens as undervalued, trading well below one estimate of fair value and at a P/E of 11.5x versus an industry average of 14x. However, earnings recently declined 3% and margins slipped to 2.2%. Long-tenured leadership and what appear to be high quality earnings are positives, but underperformance versus the wider U.S. market, insider selling and reliance on external borrowing highlight why investors may want to examine both the income potential and the risks in this defensive story.

Village Super Market’s low P/E, supermarket cash flows and 2.45% yield raise a clear question: is the market mispricing this stock’s resilience or correctly flagging its softer margins and earnings dip? Check the DCF valuation analysis for Village Super Market

Cochlear (ASX:COH)

Overview: Cochlear develops and sells implantable hearing solutions for children and adults, including cochlear implants, sound processors, bone conduction systems and accessories that help people with severe hearing loss better access sound in everyday life.

Operations: Cochlear generates about A$2.3b in annual revenue from implantable hearing devices, with sales spread across the Americas, EMEA and Asia Pacific.

Market Cap: A$7.4b

Cochlear stands out in a tech-led selloff because demand for its hearing implants and upgrades is tied to medical need rather than consumer sentiment, so its earnings profile can be less sensitive to market swings. The company holds a strong position in a growing ear health market, supports that with ongoing R&D and product improvements such as MRI friendly implants, and currently sits below one independent fair value estimate while analysts still see some upside. At the same time, slower revenue growth than the wider market, softer margins versus last year and reliance on higher risk external funding keep the risk profile real. That mix of essential product, premium pricing power and genuine execution challenges is what makes Cochlear worth a closer look for defensive investors.

Cochlear’s earnings tied to medical need, global footprint and premium pricing create a story that many investors only half see, while softer margins and funding choices raise questions that the 2 key rewards and 1 important warning sign

G. Willi-Food International (WILC)

Overview: G. Willi-Food International is an Israel based food company that imports, markets and distributes a wide range of packaged groceries worldwide, from canned vegetables, fruits and fish to dairy, edible oils, snacks, cereals and frozen products, sold mainly through supermarket chains and wholesalers.

Operations: G. Willi-Food International generates approximately ₪622.7m in annual revenue from import, export, marketing and distribution of food products.

Market Cap: US$449.8m

G. Willi-Food International catches the eye in a tech selloff because it sits in the classic defensive space of everyday food products. It still trades at a P/E below both its peer group and the broader US Consumer Retailing industry, while earnings and net margins have strengthened in recent periods. The company reported higher revenue and profit in its latest annual and quarterly results, alongside a cash dividend. However, funding the business entirely with higher risk external borrowing and a one off gain of ₪35.9m mean the current profitability picture is not as straightforward as it looks at first glance. When adding in a 13.9% ROE and an experienced board and management, investors have a more nuanced defensive food stock story to assess.

Strengthening earnings, richer margins and that cash dividend make G. Willi-Food International look like a quietly accelerating defensive play, yet its one off gain and borrowing raise sharper questions for the analysis report for G. Willi-Food International

The three Defensive Value Stocks highlighted here are only a starting point, with the full screener surfacing 16 more companies that pair value, dividends and balance sheet strength with equally compelling narratives through the Defensive Value Stocks screener. Use Simply Wall St to identify and analyze the specific catalysts, risk flags and income profiles that matter most to you, so you can focus on the highest conviction ideas within this defensive value theme.

Take Control of Your Investment Journey

If G. Willi-Food International or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Defensive Value

Tech stocks can move quickly and sentiment can change just as fast. Use this moment to scan fresh stock ideas before the crowd, while the data may still be relevant.

- Spot under-the-radar quality by reviewing companies in the 19 high quality undiscovered gems that currently combine strong fundamentals with overlooked stories before momentum becomes more widely recognized.

- Track cash-rich balance sheets by scanning the list of solid balance sheet and fundamentals (48 results) so you can focus on businesses that may be better positioned to withstand sharp drops in sentiment.

- Position ahead of potential infrastructure shifts by checking the 34 power grid technology and infrastructure stocks and see which stocks could benefit if grid upgrades receive increased attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.