3 Dividend Stocks With High Yield And Borrowing Risk

With Kevin Warsh’s Federal Reserve signaling that rate cuts are off the table and inflation risks tied to energy and housing pressures staying in focus, income investors are again weighing how reliable their dividend streams might be if borrowing costs stay higher for longer. This article looks at three high dividend yield stocks from a screener that emphasizes projected payouts, balance sheet strength, and payout discipline, and considers how exposed they are to the Fed’s more hawkish tone. By the end, you will have a clearer sense of which dividend stocks could still deserve a closer look for income and which might warrant more caution.

Kunlun Energy (KLYC.Y)

Overview: Kunlun Energy is a Hong Kong based subsidiary of PetroChina that focuses on exploring, producing, processing, and selling natural gas, LNG, LPG, and crude oil across several Asian markets, with a major role in midstream and downstream gas infrastructure.

Operations: Kunlun Energy generates most of its revenue from Natural Gas Sales at CN¥161.2b, with additional contributions from Sales of LPG at CN¥25.3b and LNG Processing and Terminal operations at CN¥10.6b, while Exploration and Production remains a small segment at CN¥0.1b.

Market Cap: US$7.35b

Kunlun Energy stands out in a higher for longer rate world as a high yield gas utility stock, combining a 5.49% dividend and a large CN¥193,979m revenue base with what Simply Wall St models as a sizeable discount to estimated fair value. The business sits in a mature energy infrastructure space that often appeals to income investors looking for steadier cash flows. Management has reaffirmed a dividend policy targeting at least a 50% payout of profit and maintaining total dividends at or above 2025 levels through 2028. At the same time, slowing earnings, modest 2.8% net margins, reliance on external borrowing, board turnover, and highly illiquid trading mean investors should look closely at whether the income and valuation story still outweigh these risks.

Kunlun Energy’s 5.49% yield and large CN¥193,979m revenue base look appealing, but the real story sits in how those cash flows stack up against its estimated fair value, debt needs, and capital discipline, and the DCF valuation analysis for Kunlun Energy hints at one factor investors often overlook

Électricite de Strasbourg Société Anonyme (LSE:0J74)

Overview: Électricite de Strasbourg Société Anonyme is a French utility that supplies electricity and natural gas to households, businesses, and local authorities, and also designs, builds, and operates energy infrastructure such as lighting networks, heating systems, and energy efficiency projects.

Operations: Électricite de Strasbourg Société Anonyme generates most of its revenue from production and marketing of electricity and gas at €936.33m and distribution of electricity and gas at €336.47m, with all reported revenue coming from France.

Market Cap: €1.39b

Income focused investors may find Électricite de Strasbourg Société Anonyme interesting as a higher yield utility that is trading at what Simply Wall St models as a deep discount to estimated fair value. The company reports a 12.6% net margin and a 23.2% return on equity, which suggests solid underlying profitability. Earnings grew 5% in the last year and the stock outperformed both the UK electric utilities group and the wider UK market. Despite this, its P/E of 8.7x sits well below sector averages. However, the mix of an unstable dividend track record, reliance on higher risk external borrowing, and limited board independence are important trade offs investors need to weigh before treating this as a core income holding.

Électricite de Strasbourg Société Anonyme’s low 8.7x P/E, 23.2% return on equity, and reported discount to estimated fair value suggest the market may be missing a key piece, and the analysis report for Électricite de Strasbourg Société Anonyme could show whether the unstable dividend and borrowing risk change that story

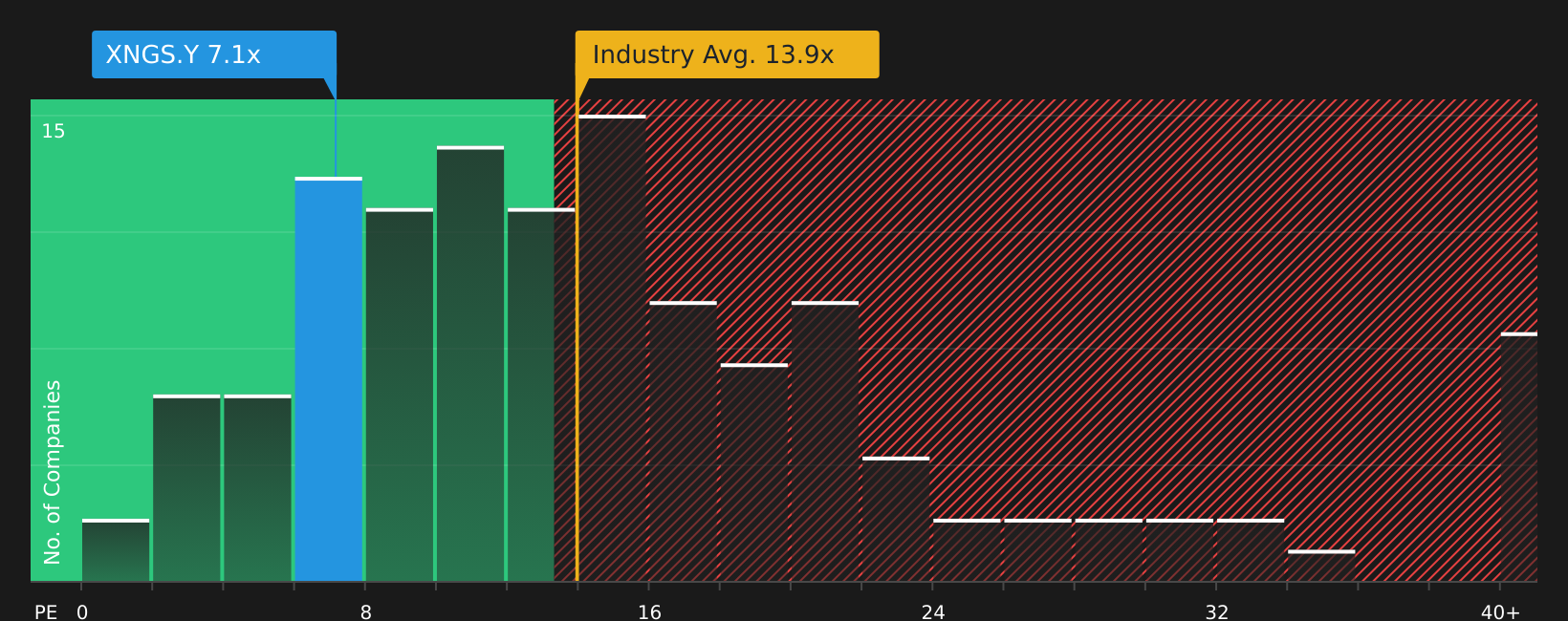

ENN Energy Holdings (XNGS.Y)

Overview: ENN Energy Holdings is a China based gas utility that builds and operates gas pipelines, supplies piped gas and LNG, runs vehicle refueling stations, and provides multi energy and low carbon solutions for residential, commercial, and industrial customers.

Operations: ENN Energy Holdings generates most of its revenue from Retail Gas Sales at CN¥67.7b and Wholesale of Gas at CN¥45.6b, alongside contributions from Integrated Energy at CN¥13.4b and Smart Home at CN¥8.3b, with smaller input from Construction and Installation at CN¥4.8b and CN¥27.9b of inter segment eliminations.

Market Cap: US$6.29b

ENN Energy Holdings offers a mix of income and value that may appeal if higher rates persist, with a 6.76% dividend yield backed by a payout ratio around 45.5% of core profits and revenue of roughly CN¥111.9b against a modest 5.3% margin. The stock trades on a P/E of about 7.2x, which is reported to be well below some global gas utility averages and certain estimates of fair value. At the same time, available forecasts indicate only mid single digit revenue and earnings growth and a projected ROE near 11.5%. That tension between cash generation, a relatively high yield, slower expected growth, and reliance on external borrowing is where the key opportunities and risks may sit for investors who focus on income and relative stability in a more hawkish Fed backdrop.

ENN Energy Holdings looks like a yield stock that trades on a modest 7.2x P/E, but that may not be the full story. See how the analyst forecasts for ENN Energy Holdings fit with its income profile and what that could be signaling.

The three dividend stocks covered here are just a starting point, as the full High Dividend Yield Stocks screen on Simply Wall St surfaced 5 more companies with equally compelling income and balance sheet narratives that could be easy to overlook. To identify the highest conviction opportunities for your own portfolio, use Simply Wall St to filter the High Dividend Yield Stocks screener by the specific catalysts and narratives that matter to you, so you can analyze which income ideas best fit your risk and return goals.

Take Control of Your Investment Journey

If ENN Energy Holdings or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Window Closes

Fresh stock ideas can move from quiet to flying once the crowd catches on, and the best entry points often drop away fast, so getting in early can be important.

- Target rock solid cash generators using the list of solid balance sheet and fundamentals (48 results) and focus your research on companies with financial strength while that information edge still matters.

- Spot early breakout potential in infrastructure by scanning the 34 power grid technology and infrastructure stocks and concentrating on businesses involved in long term grid upgrade activity before they become fully priced.

- Explore opportunities in the AI build out using the 49 AI infrastructure stocks and narrow in on companies supplying key elements of data center development while they are still attracting less attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.